A case of mistaken identity

Some investments are labelled passive, some achieve passiveness and some have passiveness thrust upon them...

Some investments are labelled passive, some achieve passiveness and some have passiveness thrust upon them.

William Shakespeare’s Twelfth Night is a comedy about mistaken identities and misunderstandings. The play centres on twins Viola and Sebastian who are separated by a shipwreck. Viola assumes the identity of a young man. Through a series of comic misinterpretations, mostly involving the pompous Molvolio, by the end of the play Viola ends up married to the Duke and all misunderstandings are resolved.

For years the question of ‘active’ versus ‘passive’ investment funds has been debated by participants in financial services. Like Viola, these classifications are often misidentified and misunderstood as ultimately they could both be defined as active. This is because many so called ‘passive’ investments, while not engaging in ‘active’ stock picking can have the same performance and risk characteristics of active investments. This is due to the active nature of the underlying index that the passive investment seeks to track.

The Oxford English Dictionary defines ‘active’ as “moving or tending to move about often or energetically”. The same lexicon defines ‘passive’ as “accepting or allowing what happens or what others do, without reacting or resisting.”

Most equity funds that are classified as ‘passive’ track a market capitalisation weighted index. Traditional market capitalisation weighted indices are constructed using an approach that assigns greater weight to larger companies and less to smaller companies. They regularly adjust their constituents’ weights to reflect changes in market capitalisation.

A purely passive portfolio, by definition, would not react to such changes, but would be accepting of any changes to a company. A purely passive portfolio would therefore be one that weights all of its stocks equally, irrespective of their size, or any changes in it.

In Australia, one example of a market capitalisation index that a ‘passive’ fund might seek to track is the S&P/ASX 200 Accumulation Index. As we all know, events such as corporate actions, management failures, the impact of government policies and macro global issues, mean that market capitalisations within this index, and therefore stock weights in any ‘passive’ fund that tracks it, change often. There are also unintended risks of investing in these type of ‘passive’ market capitalisation funds.

In Australia, investors are exposed to stock and sector concentration risk when they invest in funds that track market capitalisation indices such as the S&P/ASX 200 Accumulation Index. The top 10 companies represent more than 50% of the index; four of the top five companies are banks. Financials make up over nearly 40% of the index. Sector and stock concentration of this magnitude may make sense for active investors who are ‘bullish’ these stocks or the financials sector, but for passive investors seeking diversification, this is problematic if asset bubbles form. An investment in a fund tracking a market capitalisation index has all the hallmarks of an ‘active’ investment.

The impact of equal weighting is that while still retaining an investment in large companies, it allocates more to mid and small cap stocks than a market capitalisation weighted approach as all companies are weighted equally. The result is a portfolio that is around three times more diversified than the S&P/ASX 200 Accumulation Index as measured by the Herfindahl index.

There is only one purely passive and truly diversified equal weight portfolio available for Australian investors: the Market Vectors Australian Equal Weight ETF (ASX code: MVW). It tracks the Market Vectors Australia Equal Weight Index (MVW Index) which:

- has outperformed the S&P/ASX 200 Accumulation Index over the long term; and

- has a better risk/return trade-off than the S&P/ASX 200 Accumulation Index.

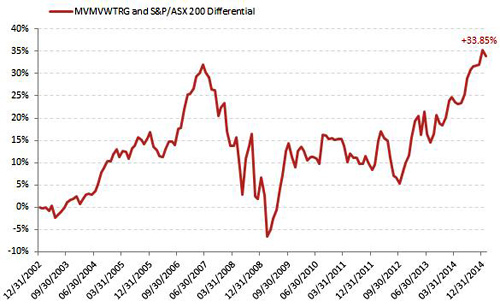

Since the inception of the MVW Index its cumulative outperformance versus the S&P/ASX Accumulation Index is 33.85%. MVW Index has outperformed in ten out of the last 13 years. To give some scale to this, the cumulative absolute difference between the two indices is presented in the following graph.

Cumulative absolute difference: January 2003 to January 2015

Source: Market Vectors Index Solutions (MVIS), FactSet as at 31 January 2015

Results are calculated to the last business day of the month and assume immediate reinvestment of all dividends and exclude costs associated with investing in the ETF. You cannot invest directly in an index. The above performance information is not a reliable indicator of current or future performance of the Indices or the ETF, which may be lower or higher.

Equal weight delivers better returns without excessive risk.

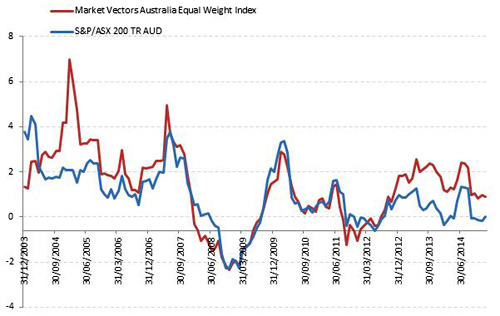

The Sharpe Ratio provides a measure of risk-adjusted performance. Since its inception the MVW Index has a consistently higher Sharpe Ratio than the S&P/ASX 200 Accumulation. That is, the better return identified above is not the result of greater risk-taking.

Rolling 12 month Sharpe Ratios: January 2002 to January 2015

Source: Market Vectors, Morningstar Direct as at 31 January 2015.

Shakespeare’s Twelfth Night contains the often quoted, “Be not afraid of greatness: some are born great, some achieve greatness and some have greatness thrust upon them.” This is part of a letter to convince Malvolio to think beyond his lower class trappings and grab the chances that are before him. Similarly, investors seeking new opportunities and attracted to passive investing for its low cost, should consider investments beyond traditional market capitalisation indices.

The Market Vectors Australian Equal Weight ETF is the only equal weight ETF in Australia. By equally weighting 74 of the most liquid stocks in the ASX it provides a better diversified portfolio and its index has consistently delivered better returns than traditional market capitalisation indices without excessive risk.

For more information on MVW and other non-traditional ‘passive’ ETFs, click here or call 02 8038 3300.

IMPORTANT NOTICE: This information is issued by Market Vectors Investments Limited ABN 22 146 596 116 AFSL 416755 as responsible entity (‘MVI’) of the Market Vectors Australian Equal Weight ETF. MVI is a wholly owned subsidiary of Van Eck Associates Corporation based in New York (‘Van Eck Global’).

This is general information only and not financial advice. It does not take into account any person’s individual objectives, financial situation or needs (‘circumstances’). Before making an investment decision in relation to the Fund, you should read the product disclosure statement (‘PDS’) and with the assistance of a financial adviser consider if it is appropriate for your circumstances. The PDS is available at www.marketvectors.com.au or by calling 1300 MV ETFs (1300 68 3837).

The Fund is subject to investment risk, including possible delays in repayment and loss of capital invested. Past performance is not a reliable indicator of current or future performance. No member of the Van Eck Global group of companies guarantees the repayment of capital, the performance, or any particular rate of return from the Fund.

Market Vectors Australia Equal Weight Index (‘MVW Index’) is the exclusive property of Market Vectors Index Solutions GmbH based in Frankfurt, Germany (‘MVIS’). MVIS makes no representation regarding the advisability of investing in the Fund. MVIS has contracted with Solactive AG (‘Solactive’) to maintain and calculate the MV Index. Solactive uses its best efforts to ensure that the MV Index is calculated correctly. Irrespective of its obligations towards MVIS, Solactive has no obligation to point out errors in the MV Index to third parties.

Market Vectors® and Van Eck® are registered trademarks of Van Eck Global.

© 2015 Van Eck Global. All rights reserved.

Published: 09 August 2018