Global gold fever settles in

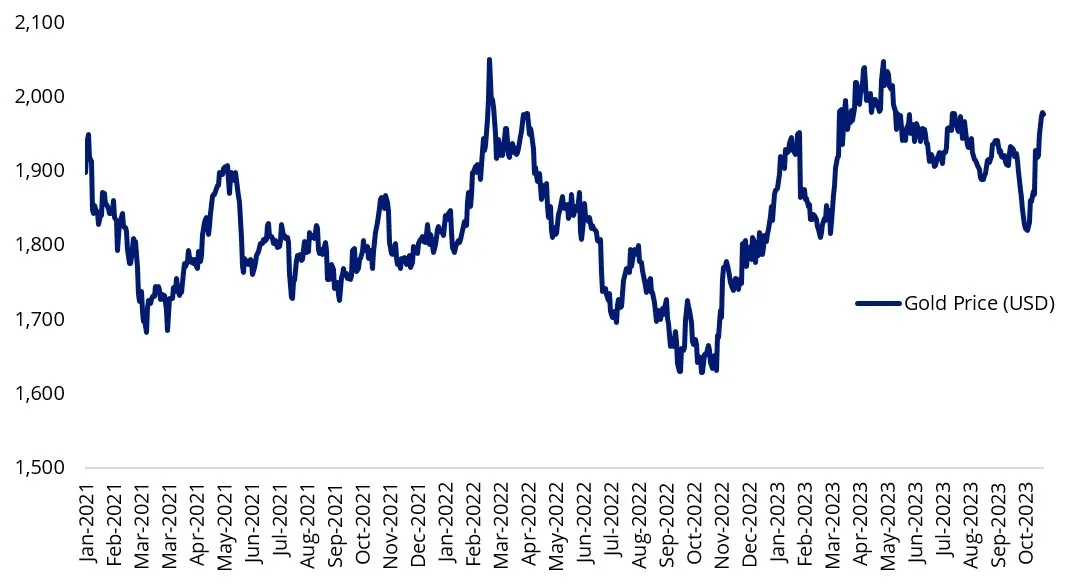

Gold’s ’safe-haven’ appeal has been reinforced, with the gold price rising to a 13-week high as conflict intensifies in the Middle East.

Gold’s ’safe-haven’ appeal has been reinforced, with the gold price rising to a 13-week high as conflict intensifies in the Middle East.

Since October 7 the precious metal surged as much as 10 per cent to US$1982 per ounce, hitting a five-month high.

Chart 1: LBMA Gold Price PM

Source: Bloomberg

According to the World Gold Council, “as a crisis hedge gold has a solid history, driven by its lack of credit risk and negative correlation to risk assets.”

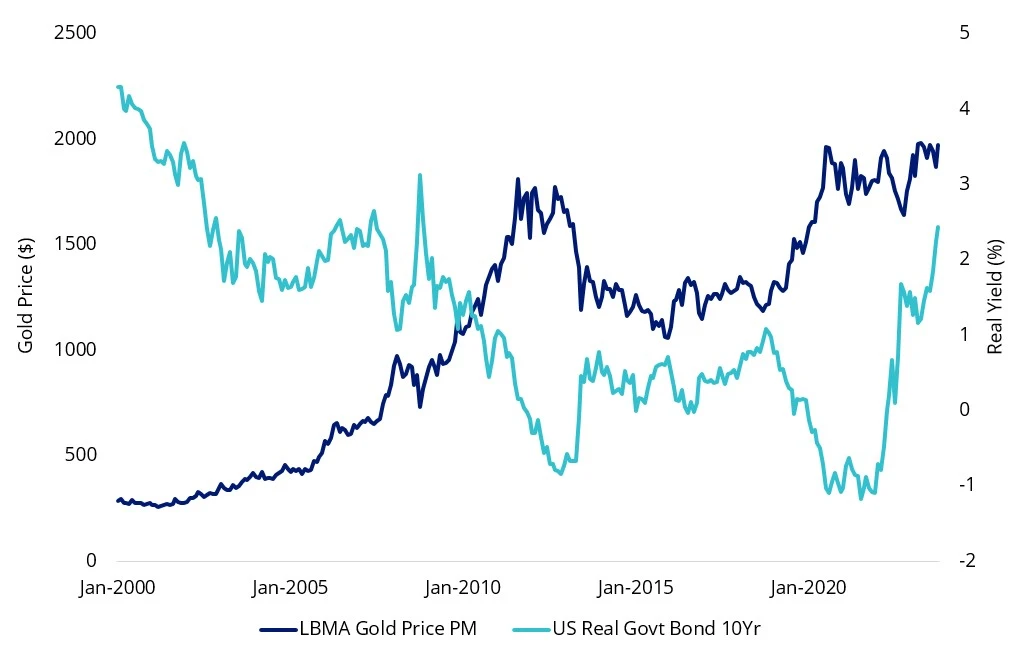

The gold price has increased recently despite rising bond yields, marking a divergence in the long-term inverse relationship between the gold price and bonds. Traditionally, rising bond yields act as a negative catalyst for gold and other precious metals that pay no interest. Gold tends to rise when bond yields fall as lower bond yields reduce the opportunity cost of holding a metal that pays no income.

Chart 2: Real yield versus gold price

Source: Bloomberg

Investment banks increase allocation

In Investment Bank JP Morgan’s latest Global Markets Strategy Report, Chief Market Strategist Marko Kolanovic said “ We additionally increase our allocation within commodities to gold, both as a geopolitical hedge, and given the expected retracement in real bond yields.”

The Investment Bank sees the gold price rising to US$2175 per ounce by quarter 4, 2024.

Fellow Investment Bank Morgan Stanley has also taken a shine to the precious metal. In its recent Asset Allocation Insights it describes its current positioning as; “we like alternative investments the most in the current environment and are positioning with a mix of gold, hedge funds as well as select private investments to enhance returns, lower portfolio volatility and manage equity beta risk.”

Central Bank buying remains strong

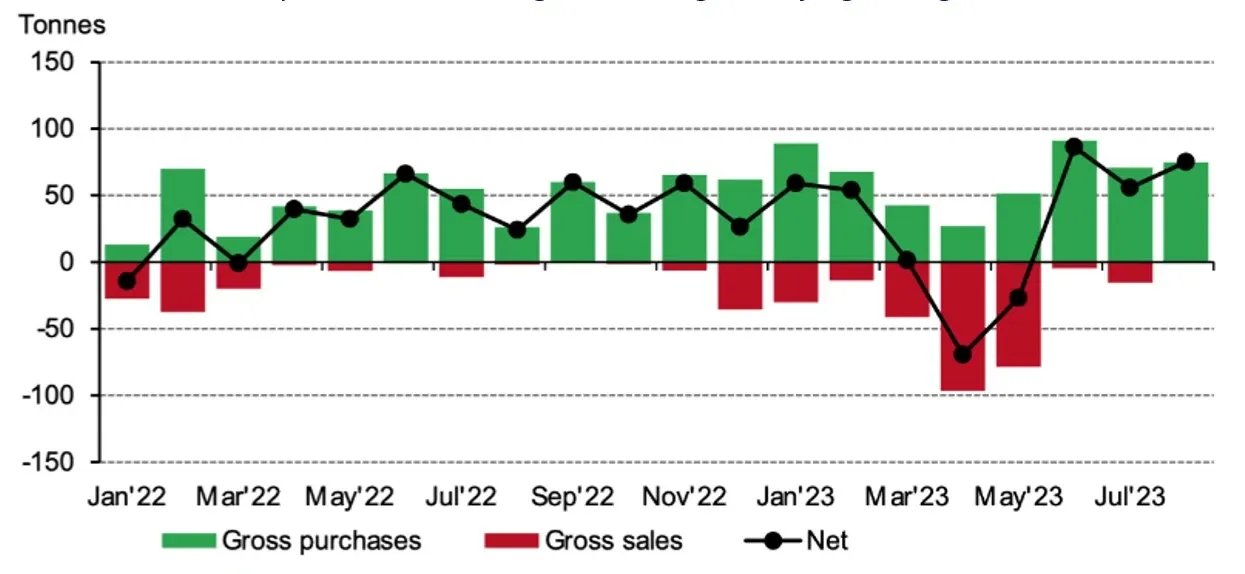

Central banks also continue their pursuit of the precious metal. According to the World Gold Council, central banks globally added a net 77 metric tons to their gold reserves in August, a third straight month of net purchases. Across the three months to August, gold buying by central banks totalled a net 219 tons.

Chart 3: Central banks post another strong month of gold buying in August

Source: IMF, respective central banks, World Gold Council.

The Council said, “central bank buying remains healthy. Even accounting for net sales earlier in the year, the pace of buying so far this year suggests that we are on course for another strong annual total.”

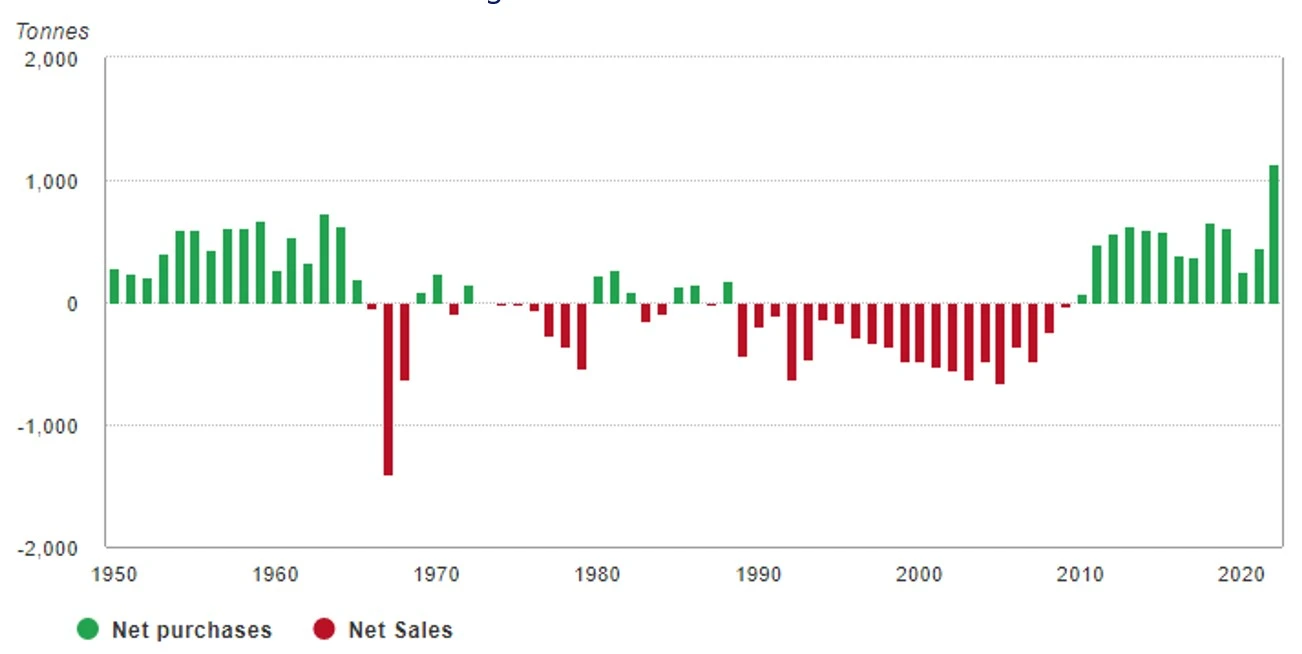

This demand comes on the back of the strongest year of central bank buying on record in 2022.

Chart 4: Central banks demand for gold rose in 2022

Source: World Gold Council

It’s not just the gold price that has benefited from the current crisis.

Gold miners

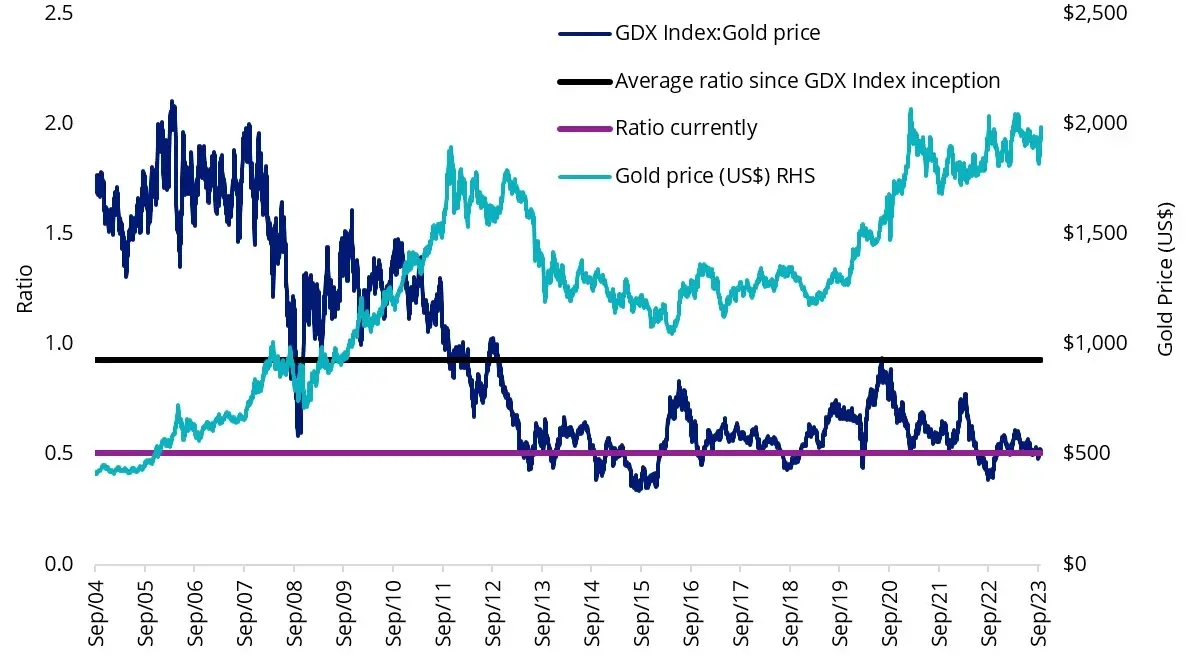

Meanwhile, gold equities have been outperforming the broader equity market buoyed by the gold price. Despite the impressive performance of gold miners recently, valuations in the sector remain historically attractive. Gold miners' stocks are trading well below historical averages. You can see this in the chart below, which shows the value of gold mining equity, measured using the NYSE Arca Gold Miners Index relative to the gold price.

Chart 5: Ratio of Gold Miners to Gold Bullion price

Source: Bloomberg, as of 20 October 2023. All figures in US dollars. GDX Index Inception is 29 September 2004. GDX Index is the NYSE Arca Gold Miners Index. You cannot invest directly in an index. Past performance is not a reliable indicator of future performance.

The gold mining sector’s balance sheets, cash flow generation and capital allocation strategies are as strong as they have ever been.

Gold miners tend to outperform gold bullion when the price rises and underperform when the gold price falls.

ETFs are an efficient way for investors to access gold investing, both miners and physical gold.

Accessing gold with the specialists

VanEck’s global leadership in gold investing stretches more than 50 years, encompassing gold equites and bullion across ETFs and active funds.

Below we outline the risks of each type of exposure to gold, owning gold bullion and owning gold miners:

Differences between gold miners and bullion

|

|

Gold bullion |

Gold miners |

|

Insurance costs |

Gold must be insured, as it can be stolen. |

None |

|

Storage costs |

Gold bullion has to be vaulted in a safe location. |

None |

|

Correlation to currencies |

High - The value of gold is priced in relation to the US dollar, therefore monetary, fiscal and - as we are finding out now - defence, policies, are a major contributor to the fluctuation in currencies and therefore gold. |

Low to medium as gold miners are able to hedge their cash flows, thus mitigating the risks of currency movements. |

|

Supply constrained / exploration |

Mine output is dropping and ore grades are getting lower and lower. |

Some miners are mining existing deposits. Some also explore and they may find gold, or there may be no gold. It might also be uneconomical to mine the discovered deposit. This is a risk of owning miners. It is worth noting that the rate of finding new gold deposits has been falling, therefore supply of new gold is finite supporting the share price of miners currently mining high grade gold. |

|

Artificial ownership risks |

High – There is more ‘paper’ gold than physical gold and these artificial securities, owned by banks and hedge funds, can distort the price of physical gold. |

Low |

|

Income |

No |

Miners pay dividends to investors |

|

Management risks |

Not applicable |

Like owning any publicly traded company, The quality of management, is a risk of owning gold miners. |

|

Correlation to equity markets |

Low |

Higher than bullion, especially during an equity market downturn |

|

Regulatory risks |

No |

Miners are subject to the rules and regulations of the country of the location of their mines and of the country they are listed in. |

|

Geopolitical risks |

The price of gold may rise if investors are uncertain about geopolitical issues affecting global markets. |

The price of gold miners may rise if investors are uncertain, however, they may also fall, especially if the geopolitical risk directly affects the gold miner or its mines. |

Two ETFs for portfolio considerations:

- NUGG – accessing physical gold, that ‘delivers’

- GDX – investing in a diversified portfolio of gold mining companies

|

VanEck Gold Bullion ETF (ASX: NUGG). |

VanEck Gold Miners ETF (ASX: GDX) |

|

|

While each gold strategy has its merit for portfolio inclusion, you should assess all the risks and consider your investment objectives.

Past performance is no guarantee of future performance. The above is not a recommendation. Please speak to your financial adviser or stock broker.

Key risks

An investment in NUGG or GDX carries investment risk. These risks vary depending on the fund and may include gold pricing risk, currency risk, custody risk, Australian sourced gold bullion risk, ASX trading time differences, financial markets generally, individual company management, industry sectors, country or sector concentration, political, regulatory and tax risks, fund operations and tracking an index. See the PDSs for details on risks.

Published: 27 October 2023

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (‘VanEck’) is the issuer and responsible entity of all VanEck exchange trades funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.