Gold miners’ re-rating calls for mass appeal, not mass production

Gold correction

US dollar strength kept pressure on gold throughout September. The dollar, as measured by the US Dollar Index (DXY), trended higher as the stock market slid from its all-time highs. The pandemic stimulus-driven bull market looks to be in jeopardy as the S&P 500 fell sharply at the beginning of the month and the dollar responded to the risk-off sentiment. Gold may have seen additional pressure as a source of cash from equity-related margin selling. Gold had been consolidating above US$1,900 per ounce since its US$2,075 high on August 7. The consolidation now looks more like a correction, as gold fell to a near-term low of US$1,848 on September 28. For the month, the gold price declined US$81.98 (4.2%), ending at US$1,885.82 per ounce. The bottom of the current gold bull market trend is around US$1,800. We expect this correction to remain above this level.Gold miners retreated with gold, as the NYSE Arca Gold Miners Index fell 7.4%.

Miners remain on point, operationally

We attended the virtual sessions of the Precious Metals Summit and Gold Forum Americas (a/k/a The Denver Gold Forum). The Precious Metals Summit features junior gold miners, most of which are cashed up from recent equity raises. As a result there was an abundance of drilling results, project updates and plans for more drilling. In our view, with new money comes new discoveries. Several of our holdings have recently announced discoveries that we believe will help advance their projects towards production. For example, De Grey Mining looks to have a multi-million ounce discovery in the Pilbara region of Western Australia. Corvus Gold has made additional discoveries at its Southern Nevada project that may turn it into a district-scale play. Galway Metals’ drilling has turned some isolated gold occurrences into a trend that may host over a million ounces in New Brunswick, Canada.

The Gold Forum Americas conference reiterated and enhanced the industry trends that we have been talking about for several years. Large gold producers tripped over one another to inform investors of their cash-generating ability and commitment to return money to shareholders through increasing dividends and/or share buybacks. Balance sheets are pristine, as those who aren’t already in a net-cash position should get there by early 2021. While there isn’t much growth among the large companies, many emphasised sustainable production bases for 10 years. Newmont even went beyond, indicating it can sustain current annual production levels of around six million ounces into the 2040s. In the past we were lucky to get five years of guidance. Most companies continue to use conservative pricing in the US$1,200 to US$1,300 per ounce range to calculate reserves and project economics. Companies also expressed a commitment to increasing Environmental, Social and Governance (ESG) initiatives. All of this bodes well for gold equity investors and demonstrates the sustainable financial and operating strength of the industry.

Still, room for improvement

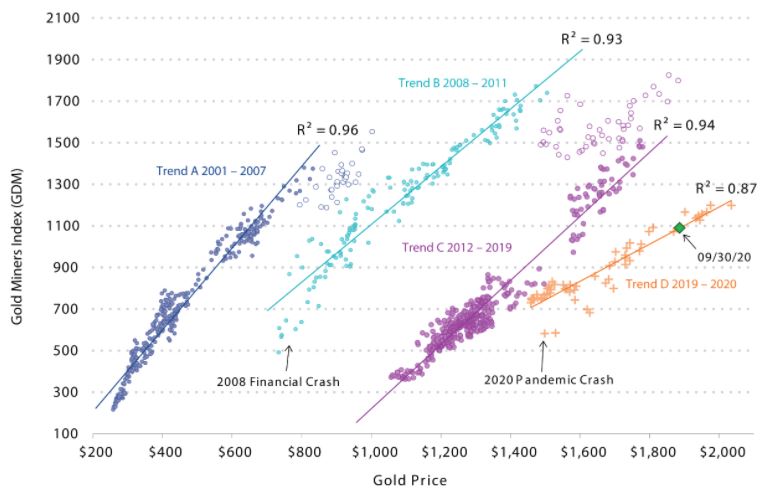

Gold reached its all-time high of US$2,075 per ounce in August. At the same time the Gold Miners Index topped out at 1,271, far below its all-time high of 1,855 in September 2011 when gold reached its former high of US$1,921. Since the current bull market began in December 2015, gold has advanced 98% to its August 2020 high, while the Gold Miners Index gained 266% over the same period. If the Gold Miners Index had returned to its old 2011 high of 1,855 in August this year, it would have advanced 435% since the current bull market began. Here we explore the reasons that gold miners have not reclaimed their all-time highs with gold.

This chart plots gold versus gold miners (as measured by the Gold Miners Index). Notice that gold and gold miners trade along four discreet trends that have shifted to the right over time. Within each trend, the extent to which gold miners’ price movements can be explained by gold price movements (as measured here by the coefficient of determination, or “R-squared”6) is very high—near 1.0, or nearly 100% of the time in some cases. Alternatively, trend shifts to the right indicate that a given gold price movement corresponds to a lower gold miner price movement than in a preceding trend. In other words, gold miners have been de-rated relative to gold. Flatter trend lines also indicate lower gold miners’ price beta7 to gold (beta being the performance leverage gold miners naturally carry to gold).

Gold vs NYSE Arca Gold Miners Index

2001 - 2020 Weekly Close

Source: Bloomberg, Van Eck Research

The chart shows that gold miners have suffered three de-ratings since 2007, with their beta to gold declining as well. The first two de-ratings occurred in late 2007/early 2008 and late 2011/early 2012 (trends A-B-C). These were caused by poor operating and financial performance on many fronts. Cost inflation eroded the operating leverage that investors expected. Rising costs also caused capital projects to fall short of expected returns. Companies made a habit of missing their production and cost guidance.

When rates fell after the financial crisis, the senior gold miners loaded up on debt and many companies overpaid for acquisitions that didn’t perform as promised. As a result, top managements of all the large gold producers lost their jobs. New managements have learned the hard lessons of the past and the industry has completely turned itself around by instilling the right incentive structure from the board to the mines. This is shown by recent financial and operating results and the strategies we have highlighted from the Gold Forum Americas.

Unfortunately, despite all of the improvements, the sector still suffered another de-rating in 2019 (trends C-D). We believe there are two reasons for this:

- Many generalist investors abandoned gold equities in the last cycle due to poor management. We have yet to see many of these investors return. So far in this cycle, most investors are using bullion ETFs for exposure to the gold market. Bullion ETF inflows have shattered records in 2020. Meanwhile net inflows to both active and passive equity funds have been anaemic.

- There is a lack of growth amongst the large gold companies. Historically, a rising gold price brought exploration excitement, high quality discoveries and expanding production. While this excitement is still driving junior gold miners, it is missing among the large companies. Multi-million ounce gold deposits have become very rare and global production is probably past its peak. The large companies are now focused on maintaining current production levels in the long term.

So far in 2020 gold has advanced 24%, while the Gold Miners Index is up 34%. If Trend D remains in place through the current cycle, the index may reach its historic 2011 high if/or when gold reaches US$2,755 per ounce. Generally speaking this would translate to a 46% increase for gold and a 70% increase for gold miners at current levels. We believe gold miners can do better.

Building mass appeal over building mines

We believe, the key to achieving a positive re-rating, better performance and higher valuations is to win generalists back to the sector. Scotia Capital Markets estimates that the average dividend yield of the large gold producers will rise to the average of the S&P 500 sometime in 2021 at 1.5%. Scotia also reckons that if gold prices become sustainable around the US$2,000 per ounce level, cash flows should enable yields in the 3% to 4% range. Managements are focused on the task and doing everything to make the gold industry appeal to a broader investor base with their ability to generate returns and mitigate risks.

Published: 09 October 2020

NYSE®Arca Gold Miners Index®is a trademark of ICE Data Indices, LLC or its affiliates (“ICE Data”) and has been licensed for use by VanEck in connection with the US Fund. Neither the Trust nor the Fund is sponsored, endorsed, sold or promoted by ICE Data. ICE Data makes no representations or warranties regarding the Trust or the Fund or the ability of the NYSE Arca Gold Miners Index to track general stock market performance.

ICE DATA MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND HEREBY EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE WITH RESPECT TO THE NYSE ARCA GOLD MINERS INDEX OR ANY DATA INCLUDED THEREIN. IN NO EVENT SHALL ICE DATA HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

No member of VanEck group of companies gives any guarantee or assurance as to the repayment of capital, the payment of income, the performance, or any particular rate of return of any VanEck funds. Past performance is not a reliable indicator of future performance.