Gold’s bearish trend ready to reverse?

A wild ride for gold in September

The gold market was overwhelmed by the relentless strength of the US dollar in September. The US Dollar Index (DXY) spent the month making new 20-year highs, driven by tough talk from the US Federal Reserve (Fed) on inflation and expectations for continued rate increases. The dollar has also been the preferred safe haven globally as China imposed further COVID lockdowns and UK tax cuts prompted heavy selling in pound sterling. The gold price fell through long-term support at US$1,680 on September 15 and continued to slide amid heavy outflows in gold exchange traded products. The decline ended on September 28 when gilt market volatility caused UK pension funds holding liability-driven investment (LDI) funds to get margin calls that threatened to take down the financial system in the U.K. The Bank of England (BOE) had to intervene with emergency purchases of gilts to calm the markets. Gold became the safe haven for a day, rising US$31 as the DXY fell. This cut gold’s losses to US$50.43 (3.0%) to end the month at US$1,660.61.

Miners focused on showcasing operating abilities

Gold stocks outperformed gold, with the NYSE Arca Gold Miners Index gaining 7.09%. We attended the Precious Metals Summit and Gold Forum Americas Conferences in Colorado. These events bring investors together with the vast majority of gold companies globally. While weak gold prices and inflationary pressures were areas of concern, the miners were more interested in showcasing their operating abilities, property attributes, and project pipelines. Managements are less concerned about financial risks due to strong balance sheets and lighter capital requirements than in past down cycles.

Cost inflation is not going away for now

Many companies are expecting cost inflation to persist into 2023, with little visibility beyond. With rising costs, some of the majors are reviewing reserve pricing with an eye to raising it roughly by US$100 from the industry average of around US$1,250 per ounce. Producers generally calculate reserves at the base of the long-term gold price trend, which is currently around US$1,400. This would also allow companies to avoid write-downs as they run reserve economics using a higher price along with the higher costs.

All producers are committed to continuing dividend payouts and buybacks. In fact, Kinross Gold boosted its share buyback programme. However, if the gold price remains at current levels, we may see some companies trim dividends, particularly those who link dividends to cash, cash flow, or the gold price.

End in sight for gold’s bearish trend?

The failure to hold long-term support at US$1,680 caused gold to fall into a bearish trend marked in purple on the chart. If the trend continues, gold might fall to its bull market base (blue line) around the US$1,400 level in the first quarter of 2023. Physical demand in India and China has been healthy and strong demand from upcoming Indian festival and wedding seasons, along with the lead-up to Chinese New Year should enable gold to remain above US$1,400.

Figure 1: Gold entered a bearish trend when it broke its long-term support of US$1,680

Source: Bloomberg. Data as of September 2022.

There are a number of catalysts that may enable gold to break out of its narrow trend. An obvious catalyst would be an aggressive Russian escalation in the war with Ukraine, Europe, and the West. Other catalysts include a global financial crisis, a reversal of Fed policies, or debt problems.

As interest rates rise, the odds of a financial crisis increase. Governments have been suppressing yields since the financial crisis in 2008. Such distortions to the financial system are like a time bomb, waiting for unwanted volatility in an inflation-driven tightening cycle. Other than UK banks and pension fund managers, who had ever heard of a LDI fund? According to Bloomberg, the size of the LDI market tripled in size to £1.5 trillion in the decade through 2020. Who knew UK pension funds were using leveraged derivatives in LDI’s to hedge their liabilities? Why were they not adequately stress tested for a rising rate environment? The shock jolted currency and bond markets around the world. The LDI crisis was a black swan event. Perhaps it is also the canary in the coal mine. How many more black swans will be exposed around the globe as rates rise?

All is not well in global financial markets

Many financial metrics are flashing red. Five-year charts show major currencies including the Yen, Pound, Dollar, and Yuan are at extremes. Treasury yield charts appear parabolic and the yield curve is inverted. The gold/silver ratio rose above 90 in September. Stock market indices and cryptocurrencies are at critical support levels. All of this can be summarised in the Goldman Sachs US Financial Conditions Index. Notice the dramatic tightening in the financial conditions chart that has reached levels of the pandemic crash and, if it continues on its trajectory, could rival the financial crisis in 2008/2009.

Figure 2: Tightening financial conditions in the U.S. could signal trouble ahead

Source: Bloomberg. Data as of October 2022.

In 2019, the Fed was forced to end its tightening cycle when the repo market blew up and gold broke out of its long-term trading range. On September 21, the BOE announced plans to reduce its gilt holdings, which is analogous to the Fed’s quantitative tightening (QT). Just one week later, the BOE was forced to buy gilts to avert a crisis. In September, the Fed started another attempt at QT, allowing US$95 billion in Treasuries and mortgage-backed securities to roll off its balance sheet each month. How long until the Fed is again forced to reverse course? The Fed has had it easy so far. It can talk tough on inflation with the strong economy and low unemployment. However, it looks as if the economy is turning. Companies as diverse as FedEx, Scotts Miracle-Gro, Micron Technologies and Nike are missing earnings and downgrading guidance. Ocean shipping rates have plummeted. Most housing indicators are trending lower. The Census Bureau reported two years of flat or declining real household income and the rising cost of essentials are driving consumer spending. Meanwhile, both Consumer Price Index (CPI) and Personal Consumption Expenditures Price Index (PCE) inflation came in above expectations at 8.3% and 6.2% year-over-year respectively.

In addition to a weakening economy, debt service is about to become a major problem. In 2007, before the financial crisis, public debt stood at US$6.0 trillion and debt/GDP was 41%. Public debt has doubled in the past decade to US$26 trillion. Over the same period, debt/GDP has risen from 78% to 105%. When rates are near zero, so too is debt service. At current treasury rates of around 4%, debt service would eventually amount to US$1.0 trillion a year, surpassing Social Security and defense as the largest item in the Federal budget. According to the Monthly Treasury Statement cited in the Wall Street Journal, net interest expense hit US$63 billion in August, or US$756 billion a year. The Committee for a Responsible Federal Budget estimates President Biden will increase deficits by a further US$4.8 trillion over the coming decade, while the Fed is poised to raise rates further. The US is not alone, most countries around the world share similar debt problems.

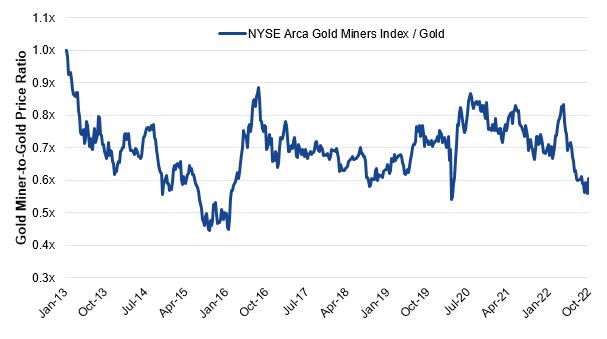

Miners are probably oversold relative to gold

If a gold catalyst emerges, gold stocks stand to gain from oversold levels. One simple way of looking at gold stock valuations is to divide the equities by the gold price. The chart shows both the NYSE Arca Gold Miners Index-to-gold and MVIS Junior Gold Miners Index-to-gold price ratios are now at the same levels as the pandemic crash. MVIS Junior Gold Miners Index-to-gold price ratio is also near the historic lows set at the bottom of the five-year bear market that ended in December 2015.

Figure 3: Gold miners are trading near their lows relative to gold prices

Source: Bloomberg. Data as of September 2022.

Published: 11 October 2022

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange trades funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.