When private equity starts buying back, it could be cheap

GPEQ tracks the LPX50 index and is Australia’s only listed private equity ETF strategy. The ETF provides immediate access to a highly diversified private equity portfolio diversified across regions, private equity investment styles and categories, vintages & currencies. Indirectly, GPEQ provides access to more than 4,500 private equity investments and 550 private equity funds.

There are three types of private equity companies in GPEQ:

- Direct Private Equity - Investments directly from the balance sheet. These companies may also act as investment managers and generate fees.

- Fund of funds - Listed funds that invest in closed-end private equity funds.

- Private Equity Managers - Private equity fund managers that generate fee income from managing private equity funds.

A private equity fund of funds and a holding in GPEQ, Pantheon International Plc, recently announced a share buyback, which is always a strong signal for listed fund-of-fund companies. This transaction follows corporate actions from GPEQ holdings HgCapital Trust and Gimv. Similarly, private equity firm Eurazeo recently confirmed it will return €2.3 billion to shareholders via dividends and buybacks. At the time of announcement, this was approximately 27% of the balance sheet.

When a fund of funds is repurchasing its shares, it is a message to the market that it is investing cheaply in assets the trust already knows and likes. Wide discounts are often prevalent among trusts, but many listed funds are often reluctant to buy back their own shares, despite repurchases providing shareholders with an immediate return by enhancing the net asset value per share (i.e. the number of shares outstanding is reduced, but the total asset value stays the same).

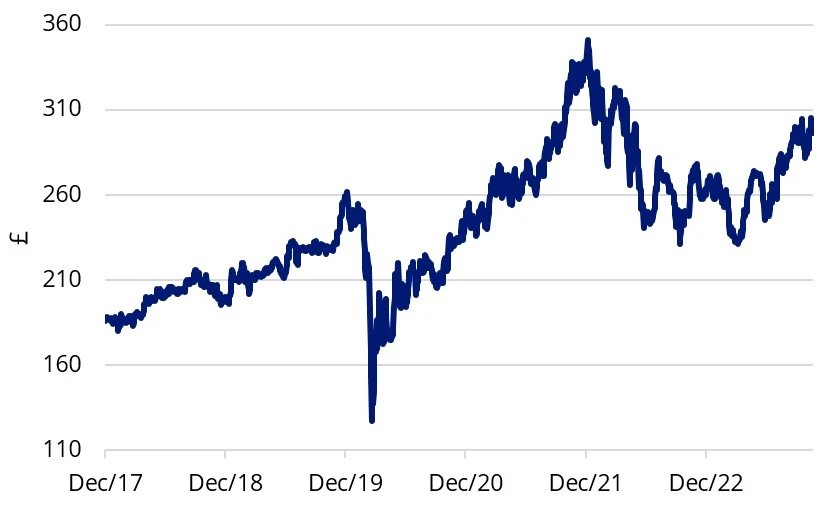

Pantheon, which has a current market capitalisation of £1.5 billion will spend up to £200 million to buy back shares, which have been trading at an average 43.6% discount over the past twelve months. According to Pantheon’s Chairman John Singer, “The current discount represents an exciting opportunity that we intend to seize on behalf of shareholders.”

Chart 1: Pantheon International Share price

|

Key Numbers:

|

Source: Data to 14 November 2023 unless otherwise indicated. Bloomberg, Questor, The Daily Telegraph, Pantheon International. This is not a recommendation to act. Past performance is not a reliable indicator of future performance.

Trading at a discount is not unique for listed private equity companies

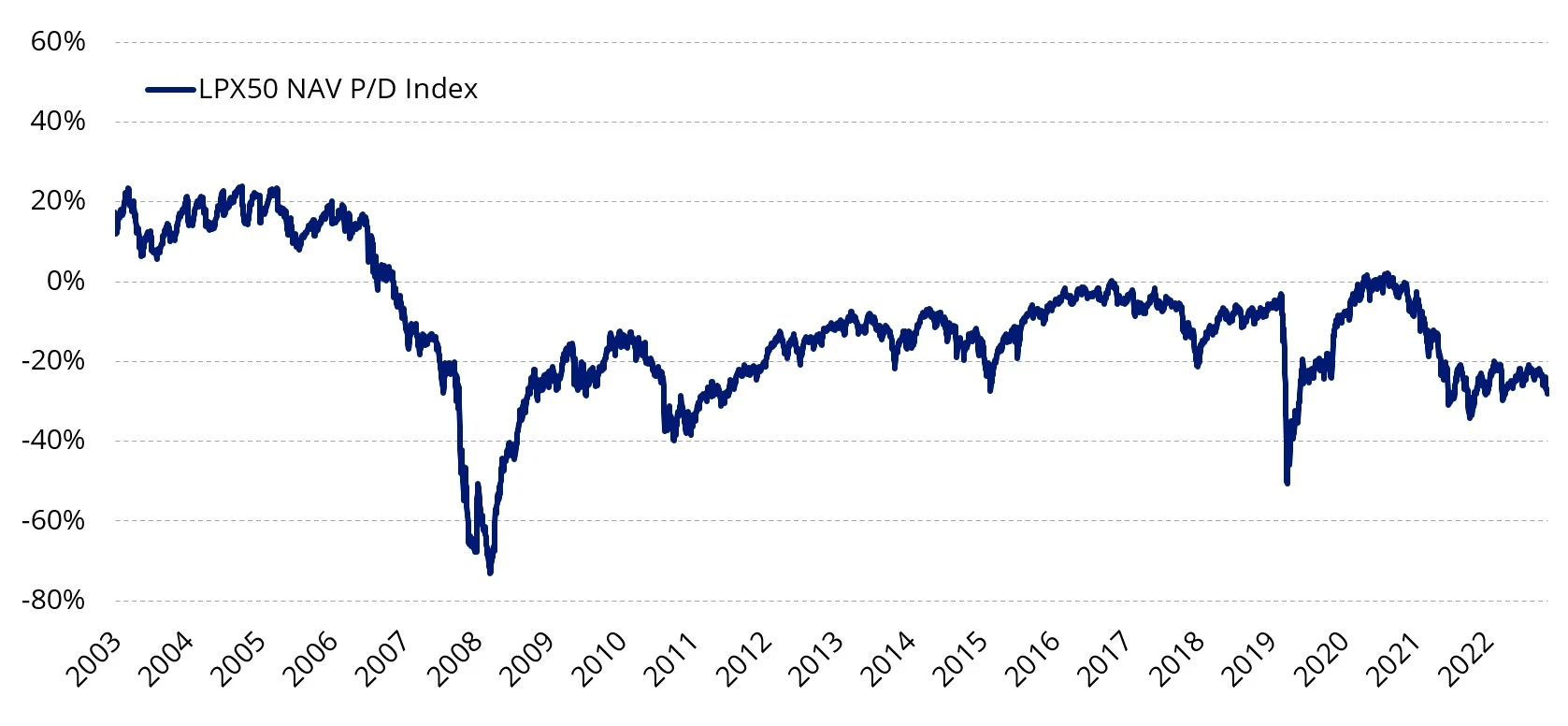

LPX has a deep research pedigree and publishes updated valuations regularly. LPX AG calculates the Net Asset Value (NAV) of the 50 largest Listed Private Equity companies, based on the underlying portfolio of private equity investments owned by each listed company comprising the LPX50 Index - this is the LPX50 NAV index. The current valuation level is still below the valuations, which were observed before 2007/08.

Chart 2: Listed private equity – discount level

Source: LPX AG. Data to 31 October 2023. You cannot invest in an index. Past performance is not a reliable indicator of future performance.

There could be more listed private equity companies that follow Pantheon’s lead and take advantage of these discounts for their shareholders. Further, listed private equity has historically outperformed broader equity markets when discounts are high.

Table 1 shows an analysis for the time period 1993-2023 (since the base date of the LPX50 Index) for every year the discount at the end of the respective year’s return of Listed Private Equity vs. Public Markets (in USD).

The empirical results suggest that in 81% of all years since 1993, Listed Private Equity outperformed Public Markets when a discount was observed at the end of the year.

Table 1: Discount/premium statistics

Source: LPX AG, Data Basis: For the current year, the highest month-end value is taken into consideration for the calculation. Past performance is not a reliable indicator of future performance. LPX50 base date 31 December 1993. Launch date 2 April 2004. Data prior to launch date is simulated and based on current methodology.

Listed private equity so far in 2023

While unlisted private equity may have been hogging the headlines in 2023, listed private equity has avoided much of the spotlight even though its returns and, as noted above activity, have been noteworthy. The VanEck Global Listed Private Equity ETF (GPEQ) has returned 22.96% for the year to 23 November 2023, though we would always caution, that past performance should not be relied upon for future performance.

Table 2: GPEQ trailing returns as at 23 November 2023

Source: VanEck, Morningstar, Bloomberg. Results are calculated daily and assume immediate reinvestment of all dividends. GPEQ results are net of management fees and other costs incurred in the fund but do not include brokerage costs and buy/sell spreads incurred when investing in GPEQ. Past performance is not a reliable indicator of future performance. You cannot invest directly in an index. GPEQ inception date is 23 November 2021 and a copy of the factsheet is here.

GPEQ allows Australian investors to include private equity as a part of their alternative allocation of their portfolios via a single trade on ASX.

Key risks

An investment in the GPEQ carries risks associated with listed private equity, ASX trading time differences, financial markets generally, individual company management, industry sectors, foreign currency, country or sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the PDS for more details on risk.

Published: 29 November 2023

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (‘VanEck’) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.

LPX and LPX50 are registered trademarks of LPX AG, Zurich, Switzerland. The LPX50 Index is owned and published by LPX AG. Any commercial use of the LPX trademarks and/or LPX indices without a valid license agreement is not permitted. Financial instruments based on the index are in no way sponsored, endorsed, sold or promoted by LPX AG and/or its licensors and neither LPX AG nor its licensors shall have any liability with respect thereto.