ETF Myth Busters

ETFs (Exchange Traded Funds) are being blamed for everything. Apparently they will be the cause of the next bubble, are distorting the market and are leading the financial world to Armageddon. Much of the criticism has come from active fund managers who stand to lose the most from the rise of passive investing. These so-called threats can be refuted.

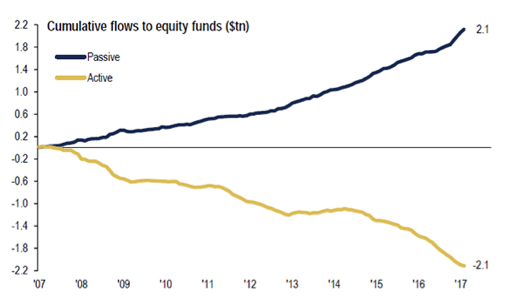

Source: Bank of America Merrill Lynch Global Investment Strategy, EPFR Global, Morningstar

Globally, the rise of passive investing since the GFC has changed the investment landscape with a notable change in investor appetite for active investing. These investments build investors’ wealth as high fees don’t erode returns. It has also been well documented that active managers have been struggling to outperform their benchmarks. Therefore in more recent times, in addition to providing investors with lower fees, passive funds have also been delivering investors with above average returns when compared to their active peers.

The rise of ETFs is part of the rise of passive investing. ETFs are passive funds that are traded on an exchange such as ASX. They track an index, in contrast to active funds, which seek to outperform an index. There are a growing number of Australian investors who are using ETFs rather than actively-managed funds for the reasons identified above

This trend has sparked a reaction. In the past few weeks, the financial press has carried stories about ETFs fuelling a price bubble, distorting the market and creating inefficiencies. It is worthwhile to deconstruct these claims to determine whether they myths or legitimate concerns of which investors should be aware.

Myth 1: ETFs create bubbles and inefficiencies

Let’s start with the claims that ETFs are creating the next ‘bubble’ and are responsible for market inefficiencies. The argument is that ETFs are mindlessly driving up prices by buying stocks regardless of their fundamental value.

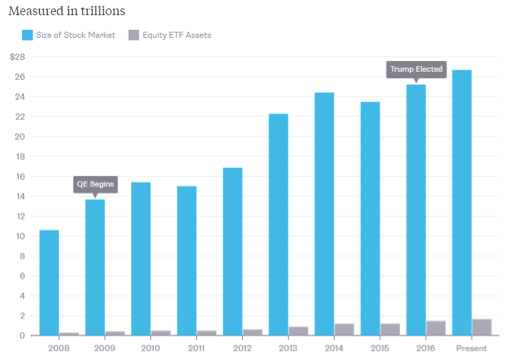

This is a myth. In Australia, ETFs do not own enough of the stock market to be a systemic risk or to even alter fundamentals in any meaningful way. The ASX’s total stock market value is $1.7 trillion, up from $1.5 trillion dollars in 2012. In that time ETFs grew from $10 billion in 2012 to be around $30 billion today of which only 42% is invested in Australian equities. Even though ETFs have tripled in size, they still only represent 1.7% of the stock market. Elsewhere, according to Bloomberg, ETFs in the US represent 6% of the equity pie. Again, not enough to alter the market significantly.

Source: Bloomberg

Myth 2: ETFs impact market liquidity

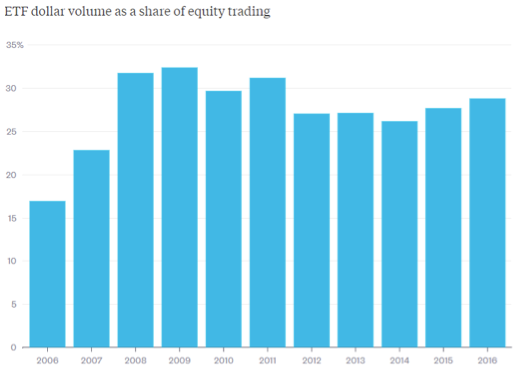

Even though ETFs only own 6% of US equities, they account for around 30% of the trading volume – double what it was 10 years ago.

Source: NYSE, Bloomberg

Bloomberg claims this could present a problem “if more and more people stop trading stocks and bonds in favour of ETFs, it will drive up trading costs in the underlying securities while potentially making it more difficult to exit on big sell-off days.”

But currently in Australia ETFs represent just 2.5% of trading volume. This is not enough to distort the economics of trading. Investors should perhaps be aware that trading by ETF fund managers is not evenly spread over the year. Most of it happens on the days the indices rebalance. Investors should avoid trading on these days like they would avoid buying stocks the day before they go ex-dividend or selling right afterwards.

The liquidity concerns about ETFs are the same liquidity concerns investors have with active funds that get too large. They can just as easily impact a stock’s liquidity (and value) on days when they trade.

The liquidity of ETFs and the rules which they operate under are not well understood by most critics of ETFs. We have written about ETF liquidity previously - here

Myth 3: ETFs are risky and complex like derivatives

In terms of the regulatory regime under which ETFs operate, in Australia they are registered managed investment schemes as defined by the Corporations Act. Therefore they operate under the same rules as apply to unlisted registered managed funds and are regulated by ASIC, as well as a subset of the ASX rules, overseen by ASX. Like managed funds, the assets of the ETFs are also physically held by a custodian. ETFs are not complex derivative instruments. Rather they are transparent, highly regulated investment vehicles which marry the best features of unlisted managed funds and listed securities, backed by real assets.

Myth 4: ETFs inefficiently allocate resources

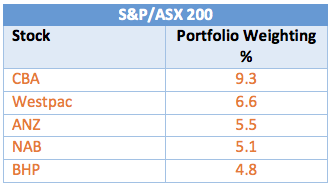

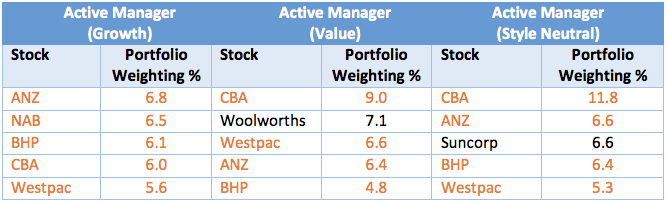

Another criticism of ETFs is that because of their disproportionately large flows, ETFs have been distorting the market by buying stocks that active fund managers wouldn’t necessarily buy. The table below illustrates that active funds are buying the same stocks as the market capitalisation index in almost similar proportions.

Source: Morningstar Direct, as at 30 June 2017. Stock highlighted orange appear in more than one portfolio.

The hysteria about ETFs is based on myths. ETFs are not creating a bubble nor are they inefficient or significantly distorting the market. Much of the negative focus on ETFs has been written by those who stand to lose the most. One group not complaining about ETFs are those who have invested. Often they are getting better than average returns and VanEck’s second annual smart beta survey illustrates that 99% of those who invest in those passive funds are satisfied with their performance.

This information is issued by VanEck Investments Limited ABN 22 146 596 116 AFSL 416755 (‘VanEck’). This is not a solicitation to buy or an offer to sell shares of any investment in any jurisdiction. It is general information only and not financial advice. It does not take into account any person’s individual objectives, financial situation or needs. Before making an investment decision in relation to any VanEck funds, you should read the relevant PDS and with the assistance of a financial adviser consider if it is appropriate for your circumstances. PDSs are available at www.vaneck.com.au or by calling 1300 68 38 37.

Related Insights

Published: 09 August 2018