A world not yet in sync

In our latest VanEck ViewPoint, we look at a range of considerations for investors when positioning their portfolios to navigate global markets. In this issue:

- Populism draws to a close in Europe

- China A-shares' debut in MSCI EM Index

- Hawkish Fed disconnects from market expectations

- Australian Federal Budget targets big banks and infrastructure

Populism draws to a close in Europe

Geopolitical factors continued to dominate much of the market commentary as the second quarter drew to a close. The defeat of far right parties in the Netherlands and France, a swing to the left in the UK election and the US pulling out of the Paris climate agreement put Europe at the centre of global political events.

China A-shares' debut in MSCI EM Index

MSCI announced plans in June to add mainland China shares (China A-shares) to its benchmark emerging markets index, at a weight of 0.73% after twice previously deciding against their inclusion. It is worth pointing out the Chinese see this as another step towards regaining their rightful place as the largest economy in the world.

Hawkish Fed disconnects from market expectations

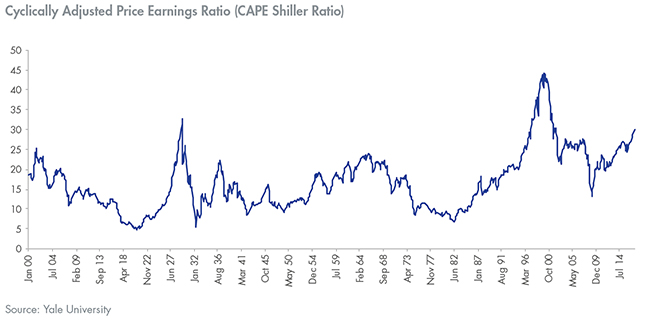

As President Trump has struggled to implement policies and his administration has been dogged by controversy, the Trump "reflation" trade has unwound. Despite most asset classes giving up most, if not all of their gains, the one asset class that appears to still believe in the reflation trade is US equities. The CAPE Shiller Price-to-Earnings measure ended May at 29.52. We have seen US equity valuations at levels beyond this twice before in history, in the lead up to the Great Depression and in the lead up to the Dot-Com Crash.

The greater concern however for those looking at the US economy more broadly is the bear flattening of the forward rate curve. As short term rates are rising, the long end of the curve has been falling, an outcome referred to as "bear flattening". Long term interest rates are reflective of the expectation of future short term rates. If there is a belief that future economic growth will be lower, investors are happier to lock in a lower long-term interest rate.

The persistent disconnect between the Fed's narrative (hawkish) and the recent data flow (sluggish) supports market expectations of the Fed's staying on hold until March 2018 versus one more hike in 2017 signaled by the Fed "dots". It is our view that the US Federal Reserve is walking a tight line between giving themselves room for monetary easing in the event of the next economic downturn and also putting at risk the current economic recovery at a time when it appears to be running out of steam.

Australia – Federal budget targets big banks and infrastructure

The 0.06% levy on banks with liabilities greater than A$100 billion imposed by the Federal Government in the May 2017 budget, drew sharp rebukes from CEO's of Australia's five largest banks. These criticisms of the Government appeared hollow after S&P shortly afterwards downgraded the debt of all other Australian banks. They highlighted that the only reason Australia's five largest banks were spared was because they had been deemed "too big to fail" which in the view of S&P "offsets the deterioration in these banks stand-alone credit profiles".

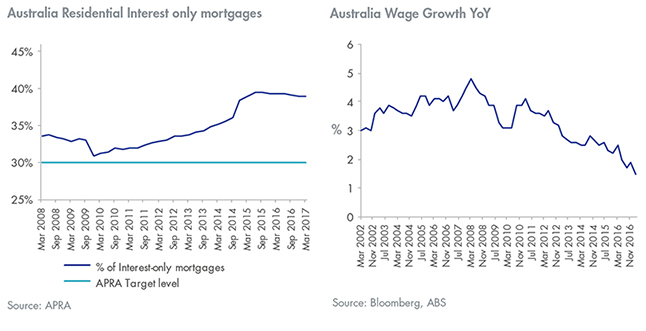

This followed on from APRA releasing additional macro prudential measures in March after Chairman Wayne Byres said that APRA "views a higher proportion of interest-only lending in the current environment to be indicative of a higher risk profile". When considering that the level of housing finance debt has continued to rise to its highest ever level, coupled with a lack of wage growth, rising mortgage rates and increased macro prudential restrictions, strong indications are that we have now reached the top of the housing cycle and a slow unwind of the recent rapid appreciation is likely.

Lost in the focus on housing affordability and the banking tax was the Government's planned investment in infrastructure. At a time when borrowing costs are at historic lows for the government, investment in projects that will provide long-term economic benefits makes sense. It has long been our view that this is particularly positive for listed infrastructure companies, with those that can demonstrate a track record of successfully operating large scale assets being able to position themselves as the ideal partner for government investment.

To read our latest VanEck ViewPoint click here

This information is provided in good faith by VanEck Investments Limited ABN 22 146 596 116 AFSL 416755 ('VanEck') It is general information only and not financial advice. This information is believed to be accurate at the time of compilation but is subject to change. VanEck does not represent or warrant the quality, accuracy, reliability, timeliness or completeness of the information. To the extent permitted by law, VanEck does not accept any liability (whether arising in contract, tort, negligence or otherwise) for any error or omission in the information or for any loss or damage (whether direct, indirect, consequential or otherwise) suffered by any recipient of the information, acting in reliance on it.

Published: 09 August 2018