Why China equities warrant a look in

China is about to join the rest of the re-opened world, with its major cities emerging from COVID lockdowns. Its central bank and government are supporting economic activity and recent price action too presents, in our view, a compelling entry opportunity for investors.

While much of the developed world is facing higher inflation, higher rates and governments with historically high levels of debt, China still has ‘dry powder’ to stimulate its economy.

Over the last two-odd years there has been a lot of discussion about an allocation to China in a portfolio and recently this talk has shifted as to whether China is investable or not. Investors that ignore China do so at their own peril, despite China becoming the largest economy into the rest of the century; being positioned differently from other developed market economies therefore providing diversification benefits; and being Australia’s largest trading partner.

Putting geopolitical concerns aside, China equities we think, warrants an investment allocation. China is about to join the rest of the re-opened world, with Shanghai and the other major cities emerging from COVID lockdowns. China’s central bank and government are supporting economic activity, evidenced by a sharp rise in China’s credit impulse. The recent price action too presents a compelling reason to consider an entry opportunity for investors.

Beijing and Shanghai are reopening

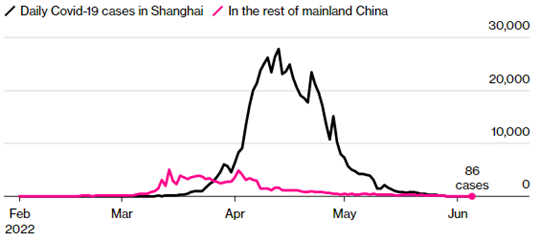

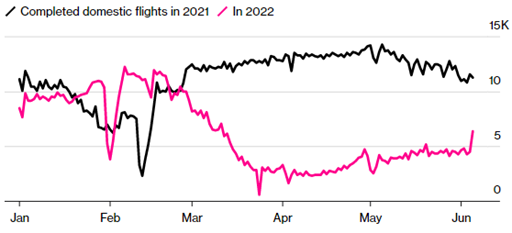

China’s worst COVID-19 outbreak is ending, with cases continuing to fall, all major cities loosening restrictions and daily life mostly returning to normal.

| Figure 1: China's largest outbreak in more than two years looks to be under control | Figure 2: Air travel in China rebounded as cities reopened |

Source: Variflight Source: Variflight

Markets reacted accordingly so far in the first seven days of the month with the “New Economy” sectors up over 3%, as shown by the MarketGrader China New Economy Index. Should the China market react to re-openings as they have in other markets, analysts expect a ‘strong rebound’. Global supply pressure is expected to ease with China’s reopening.

China equity market is also responding to positive policies

China’s tech stocks jumped last week as the government’s latest batch of new game approvals bolstered bets that the industry’s business outlook is on the mend.

China’s entertainment regulator on Tuesday approved licenses for 60 new games. Many investors see this as a flag toward policy normalisation following Beijing’s wide-ranging tech crackdown in 2021. CNEW holdings G-BITs, Kingnet, Shenzhen Shengxunda and 37 Interactive all rose in excess of 1.8% following the approvals even though none are directly involved in the 60 ratified games.

While the regulatory overhang for China and the China tech sector will weigh on investor’s minds, China has been working for many years to open its equity market for offshore investors. Chinese authorities worked hard to ensure its A-share market was included in MSCI and FTSE indices by satisfying stringent liquidity and accessibility criteria. We think China A-Shares are investable and the government will be working with industry as policy makers stimulate the domestic economy.

The importance of China

Overall, we remain optimistic about China, given the mainland’s strong fundamentals. China will soon become the world’s biggest economy and it will be China’s younger, urbanising demographic that will drive economic growth as the economy re-opens.

A-share companies in the consumer, healthcare, and technology-related sectors, which source the bulk of their profits and revenues from the domestic market, look to be well placed to benefit from the economic expansion and government and central bank attempts to kick-start growth.

Stepping back, one of the reasons investors diversify globally is to gain exposure to different economic cycles than those being experienced domestically. With much of the developed world facing higher inflation, higher rates and governments with historically high levels of debt, China’s economy has different economic fundamentals. China still has ‘dry powder’ to stimulate its economy. Its central bank is working hard to create lending and growth in China, unlike much of the rest of the world, is expected to be positive in the seconds half of 2022.

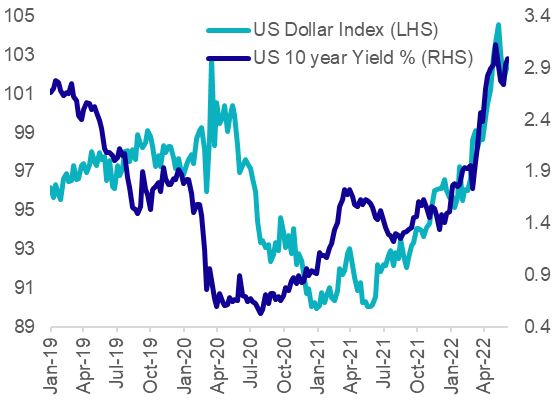

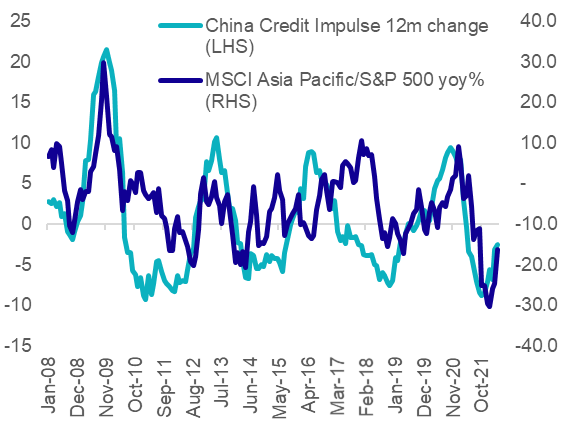

Recently, US dollar and treasury yields have pulled back from recent highs, which is good news for China, as dollar strength has been part of the tightening conditions. The other positive for China, and the rest of Asia, is the improvement in China’s credit impulse.

| Figure 3: US dollar Index and US 10 year yields (%) have pulled from highs in May | Figure 4: China’s credit impulse rising good for Asia equities |

Source: Bloomberg Source: Bloomberg

The credit impulse is expected to continue to rise as China’s Central Bank is urging lenders to boost loans. During the past week China’s Central Bank also said it would support lenders to lower financing costs, as well as stepping up help for small businesses in order to stabilise the economy and jobs.

China is Australia’s largest trading partner, and while recent tensions between the governments have been in the news investors, irrespective of the geopolitical views, that do not have a China exposure do so at their own peril, we think.

As a diversifier and a growth allocation China equities, we think, warrants consideration.

There are limited ways through which Australian investors can acquire China A-shares and more specifically, the sectors that are the growth engine of the growing services sector and recent price action presents a compelling reason to consider an entry opportunity.

VanEck gives investors unequivocal access to China A-Shares via its RQFII licence that allows for deeper and broader access and better risk management. The VanEck China New Economy ETF (CNEW) tracks the MarketGrader China New Economy Index (CNEW Index) which includes 120 China A-shares, equally weighted, from the Healthcare, Consumer Staples, Consumer Discretionary and Technology sectors, all with the best Growth at a Reasonable Price (GARP) attributes.

Valuations

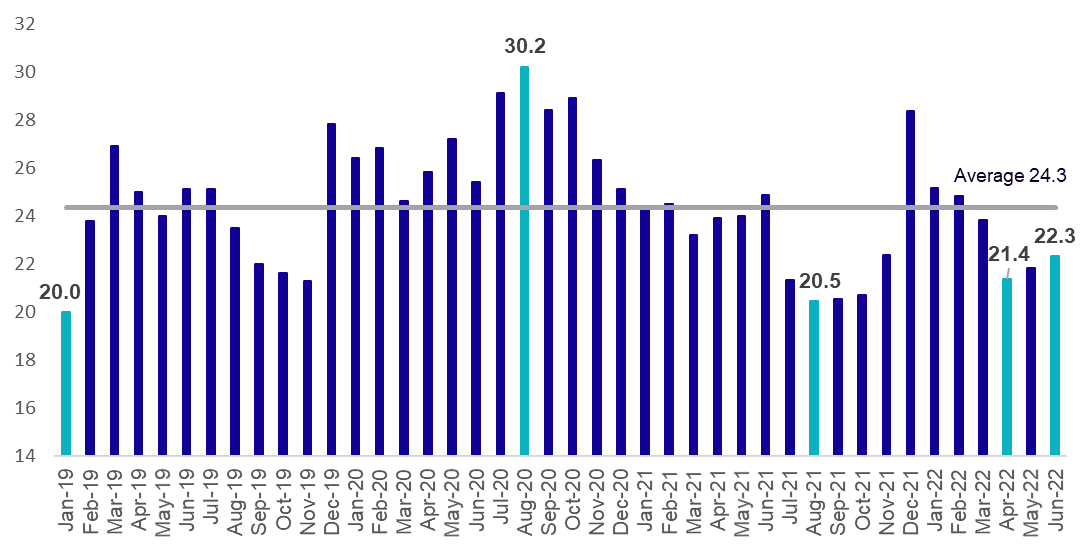

Following the recent selloff, the constituents of the CNEW Index traded at a median trailing P/E of 21.4x in April, well below its average, since CNEW’s inception, and the lowest valuation since October 2021, when the median was 20.7x. The current valuation of 22.3x represents a 26% discount to the CNEW Index’s valuation in August 2020, when it peaked following a massive post-COVID run up, as illustrated in Figure 5.

The last time CNEW Index had experienced a significant decline in its median trailing P/E was July/August 2021, when the multiple fell to 20.5x from 24.9x in June 2021. That multiple compression was followed by a 19% rise in the Index (price returns in Australian dollars) until it peaked five months later in December 2021.

Figure 5: Median trailing price to equity (P/E) for MarketGrader China New Economy Index, 2019 - 2021

Sources: MarketGrader, FactSet, 6 June 2022.

Sources: MarketGrader, FactSet, 6 June 2022.Even accounting for the recent selloff in China, CNEW is still up 13.81% p.a. since November 2018 when it launched. Noting that this past performance is by no means indicative of future performance.

CNEW performance since inception

|

As at 8 June 2022 |

|

|

||||

|

MTD |

1 Month |

3 Months |

1 Year |

3 Years |

Since inception# |

|

|

|

|

+7.37 |

-9.22 |

-23.16 |

+12.15 |

|

#CNEW inception date is 8 November 2018 and a copy of the factsheet is here.

Source: VanEck, Morningstar Direct. Performance is in Australian dollars. Results are calculated daily and assume immediate reinvestment of all dividends. CNEW performance includes management fees and other costs incurred in the fund but excludes broker fees and buy/sell spreads associated with investing in CNEW. Past performance is not a reliable indicator of future performance of CNEW.

CNEW gives Australian investors easy access via an ASX-listed ETF, to China A-shares and the enormous potential growth opportunities in China’s New Economy sectors, including the technology and healthcare sectors.

Only VanEck offers specific China A-shares ETFs so that investors can participate in what may be the next growth phase for domestic China investments, beyond limited opportunities in H-shares, Red-chips and NYSE listed ADRs.

Key risks

An investment in the ETF carries risks associated with: ASX trading time differences, China, financial markets generally, individual company management, industry sectors, foreign currency, sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the PDS for details.

Published: 17 June 2022

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange trades funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.

CNEW tracks the CSI MarketGrader China New Economy Index. "MarketGrader" And “CSI MarketGrader China New Economy Index” are trademarks of MarketGrader.com Corporation. MarketGrader does not sponsor, endorse, sell or promote the Fund and makes no representation regarding the advisability of investing in the Fund. The inclusion of a particular security in the Index does not reflect in any way an opinion of MarketGrader or its affiliates with respect to the investment merits of such security.