China’s trade surplus: Historic high gets higher

China’s external surpluses

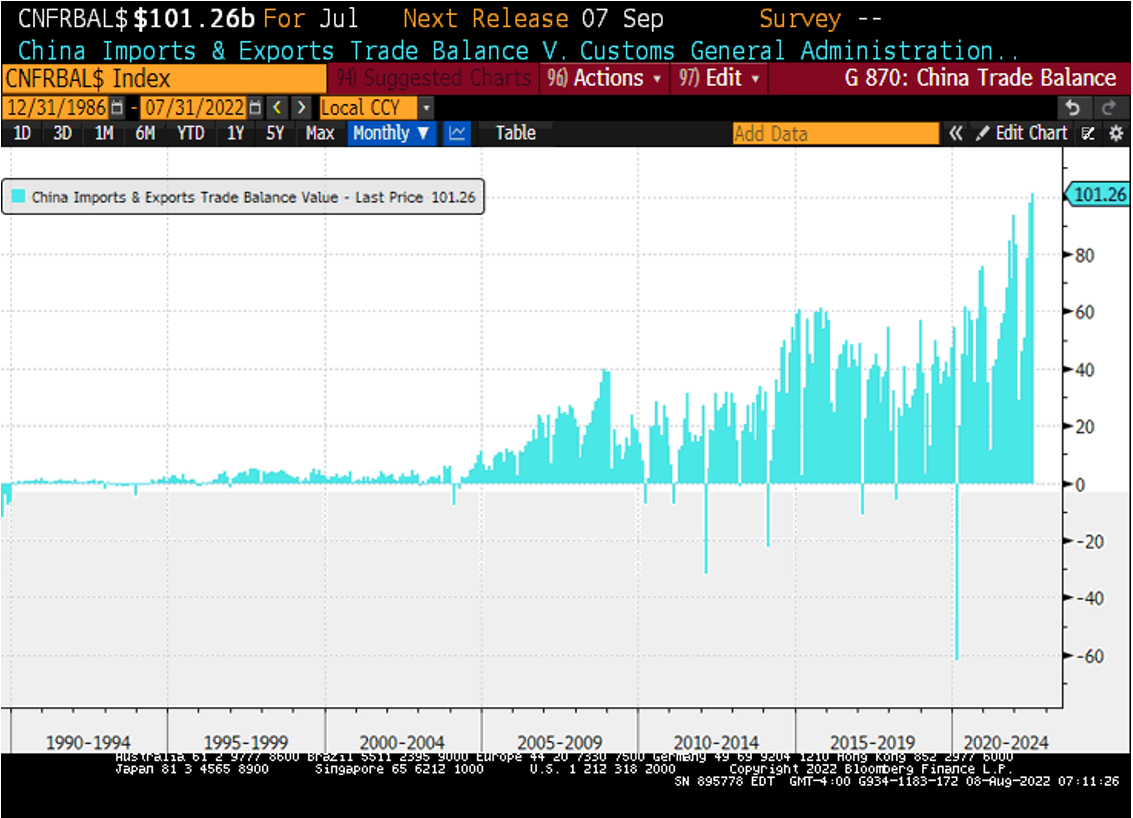

China’s trade surplus topped US$100b in July – a historic record for a month (see figure 1 below). What are the main takeaways? First, such a large trade surplus is growth-positive at the margin – an important consideration when other growth drivers (such as household consumption) are still soft, and the consensus growth forecast for 2022 has been cut below 4%. The contribution of net exports to China’s real GDP growth surged above 20% in 2020-21 – not a negligible amount. And this also suggests that authorities will continue to be super-conservative with any additional policy stimulus (on top of the infrastructure plan), focusing on specific sectors and specific issues (real estate). In regards to the stimulus timeline, we would expect to see a lot of frontloading – forthcoming credit and money aggregates for July should provide more colour (and evidence that this is indeed the case).

Global growth outlook

The second takeaway from China’s foreign trade numbers is that exports growth remains solid (up by 18% year-on-year), suggesting that the global supply chain disruptions might be easing (especially in Europe and Asia) and that the global growth backdrop might not be as dismal as news headlines suggest (I saw a couple of “Schroedinger’s recession” comments in my inbox this morning). Indeed, the latest labour report in the U.S. was quite upbeat, strengthened the market’s conviction about another large rate hike in September – the Fed Funds Futures currently price in +69.6bps vs. +56.6bps on August 1.

China’s currency depreciation

The last takeaway is that larger trade surpluses can translate into large(r) current account surpluses, which is one of the key fundamental drivers for the currency. Granted, there are other equally important factors – interest rate differentials (5-year yield differential between China’s government bonds and U.S. Treasuries is still negative and close to the widest – negative – point in years), foreign direct investments (down in Q2), portfolio inflows (we do not have the actual Q2 number yet, but most likely outflows – just as they were in Q1). But larger current account surpluses can partially compensate for these negatives, reducing the depreciation pressure on the renminbi and stabilising the currency. Stay tuned!

Figure 1: China trade surplus

Source: Bloomberg LP. China Imports & Exports Trade Balance Value Index (CNFRBAL$) measures the difference between the movement of merchandise trade leaving a country (exports) and entering a country (imports).

Published: 08 August 2022

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange trades funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.