What China’s reopening means for markets

China’s road to reopening is front of mind for investors as we go into 2023. Markets are craving a good news story, and the relaxation of China’s zero-COVID policy, along with the prospect of a sustained growth rebound could indeed be the best news story of the new year.

China’s road to reopening is front of mind for investors as we go into 2023. Markets are craving a good news story, and the relaxation of China’s zero-COVID policy, along with the prospect of a sustained growth rebound could indeed be the best news story of the new year.

Recent policy shifts have strengthened our view that China is likely to reopen by Spring 2023. Over the past few weeks we have seen top policymakers confirm a move in the country’s COVID doctrine in public communications - the COVID zero slogan has officially been removed from any press conferences or official documents, meanwhile, larger cities including Beijing, Guangzhou and Chongqing have all relaxed restrictions. Most recently China has deactivated its national COVID tracking app.

Recent moves by the Chinese government to restore financial stability signal the country is also shifting to prioritising economic growth. Bloomberg recently reported that China has asked some of the nation’s biggest banks to help stabilise the domestic bond market. Meanwhile, last month Chinese regulators called on banks to stabilise lending to the property sector in an attempt to turn around the real estate crisis.

Reuters has reported that the nation is working on a stimulus package worth more than US$143 billion to support its semiconductor industry, which could be its biggest-ever fiscal incentive package.

Following recent developments, Morgan Stanley raised its forecast for China’s gross domestic product in 2023 to 5.4% from its previous outlook of 5%, predicting a rebound in activity will come earlier and be sharper than expected.

In a recent note the Investment Bank said, “from our perspective, policymakers are taking concerted action to lift growth across all fronts,” the note said. “This is the first time since 2019 where domestic macro policies and COVID management are aligned in supporting a growth recovery, rather than acting as countervailing forces.”

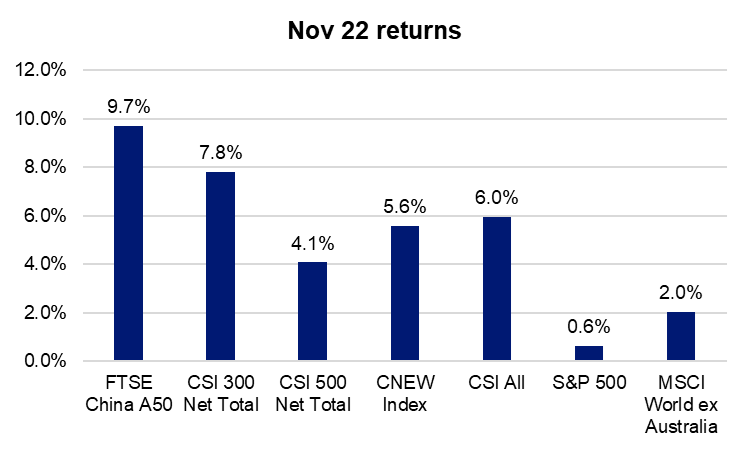

The Chinese equity market has been bolstered by the about turn in policy with the CSI 300 rising by 6.6% to a two-month high in the first week of December. Chinese equity markets are likely to run further over the next 12 months given valuations are still at very depressed levels. In particular, we expect domestic consumption (e.g restaurants, travel) to recover strongly, supported by excess household savings for the past three years.

Source: Bloomberg as at 30 November 2022. Past performance is not indicative of future results. You cannot invest directly in an index. CNEW Index is the MarketGrader China New Economy Index.

Further property market-easing measures – including credit support for debt-laden housing developers, financial support to ensure completion and handover of projects to homeowners as outlined in the 16-point set of internal directives by the country’s banking regulator and central bank – can provide tailwinds to Financials, Industrials and Materials sectors.

Morgan Stanley’s China Chief Equity Strategist Laura Wang says the bank has “just upgraded Chinese equities to overweight within the global emerging market context after staying relatively cautious for almost 2 years since January 2021. Wang says, “We now see multiple market influential factors improving at the same time which is for the very first time in the last two years.”

How investors can tap China’s reopening

The consumer sector could be the place to be for investors as China reopens, the sector has been beaten up by the pandemic related disruptions – the activity gauges indicate weak levels of consumption overall in the last two years. Given China’s savings rate is one of the highest in the world, we think that the pent-up demand must go somewhere eventually, on goods and services, as evidenced in the developed markets once the country pivots to reopening.

We are starting to see momentum building in the consumer sector. Kweichow Moutai (600519 CH) and Luzhou Laojiao (000568 CH), two of the largest white liquor producers in the country, have generated 10.75% and 18.65% month to date. From the Q3 earnings while sales growth was largely in line with expectations, the net profit growth of liquor companies was stronger than thought from product mix upgrades and expense savings. We believe the sector will react strongly once the sentiment improves.

We also continue to see growth prospects in the onshore domestic IT companies, e.g. semiconductor manufacturers, as China shifts its focus onto independence in the supply chain in technology. Despite the headwinds from the US CHIPs Act, China is preparing a support package of over 1 trillion RMB ($143 billion) aimed at local semiconductor companies according to Reuters. Zhejiang Jingsheng Mechinical & Electrical (300316 CH), one of the domestic producers, generated 7.38% MTD.

Volatility is here to stay and patience is required. There are key risks to China’s reopening, including public health concerns around the spread of the virus, and disruptions resulting from infected citizens isolating at home. China’s latest economic gauge for November came in lower across the board in Industrial Production (2.2% yoy vs consensus 3.5%), Retail Sales (-5.9% yoy vs -4.0% consensus), Fixed Asset (5.3% YTD vs consensus 5.6%) and Property investments (-9.8% YTD vs -9.2% consensus). Given the domestic economic weakness and the complexity of external factors this year, we think the nation’s central bank will keep the monetary policy intact, as evidenced by the net injection of 150 billion RMB ($22 billion) to facilitate lending in the economy.

With recession clouds forming over the US and Europe, and slowing economic growth forecast across many parts of the world, Chinese equities could be the place to be in ‘23.

Published: 19 December 2022

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange trades funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.