Riding the blue wave

We believe the spill over effect of a stronger US economy, its widening current account deficit (imports exceed exports) and a predicted weaker US dollar, is emerging market growth.

The consensus is that emerging markets are a potential beneficiary from the US ‘blue wave’ as the Democratic Party won control of all three houses of government this month. By controlling the three houses there is reduced probability of the legislative gridlocks that have been a feature of the most recent Presidencies. With the likelihood of further Democratic fiscal expansion, there is greater confidence in the US economic recovery and subsequent inflation.

We believe the spillover effect of a stronger US economy, its widening current account deficit (imports exceed exports) and a predicted weaker US dollar, is emerging market growth.

The blue wave has spurred emerging markets stocks and currencies

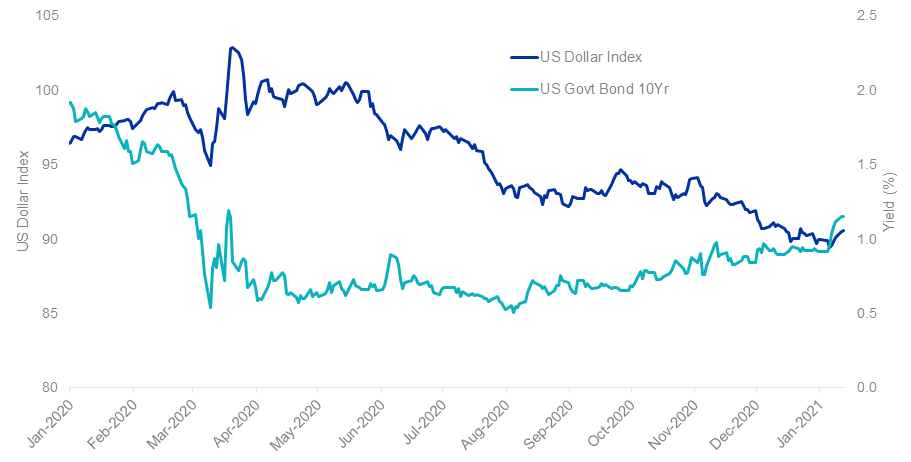

It has been well documented that the US dollar has weakened through 2020 as the US Government and the US Federal Reserve undertook unprecedented steps to stimulate the economy. It is expected that fiscal and monetary policy will continue to be expansionary into 2021.

This month the Democrats won control of the US senate for the first time in six years with victories in two runoff elections in Georgia. The result was surprising given the market expected, at best, one seat going to the Democrats. Betting was two to one against both in going blue in December.

Immediately after the Georgia run-off results US 10 year treasury yields broke through 1% for the first time since March 2020. This is an indication the market expects US growth.

Chart 1: US dollar and US treasury yields

Source: Bloomberg, VanEck

Emerging market equities, as measured by the MSCI Emerging Markets Index, is up 4.85% since the beginning of the year (to 11 January 2021. Source: Morningstar Direct).

It is expected that US inflation will reach 2% by the end of 2021 and rise above 2% into 2022. This will be supported by the private sector with increased risk appetites encouraged by low rates and government stimulus.

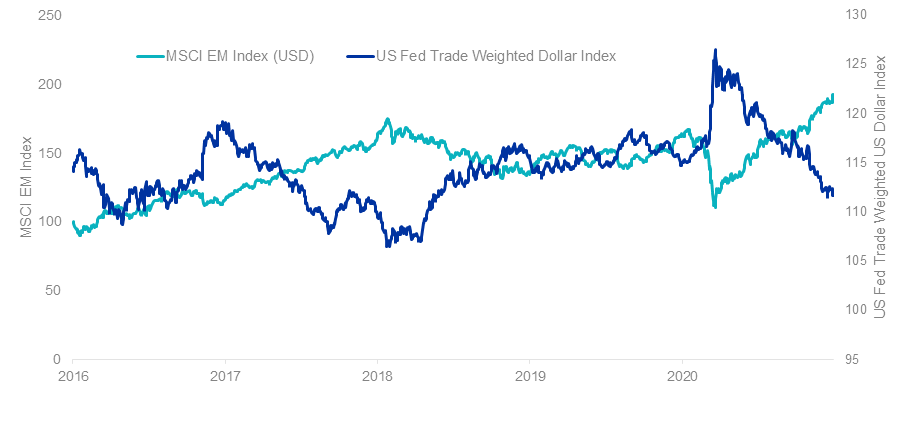

The expectation too is that the Federal Reserve will keep US interest rates low for some time and the sizable fiscal stimulus likely under the new administration will potentially leadi to a wider fiscal deficit. When combined with a US budget deficit, it also suggests that dollar weakness could persist beyond then. This makes emerging markets assets more attractive.

Chart 2: US Fed Trade weighted Dollar Index vs. MSCI EM Index: 5-Year Performance

Source: Bloomberg to 31 December 2020

Why US dollar weakness is good for emerging markets equities

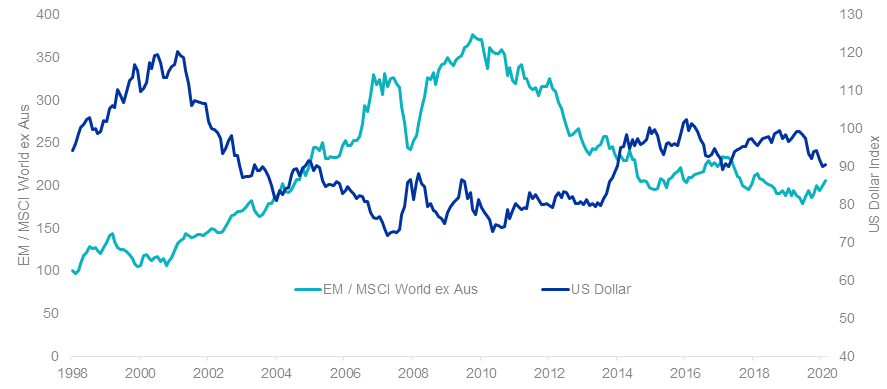

Historically a falling US dollar is often seen as good news for emerging markets, because it makes the cost of US goods and services, which they may import, cheaper in their own currencies. The weaker greenback is also good for exporting especially for countries which export commodities. The weaker US dollar is usually accompanied by stronger commodity prices, such as gold and iron ore, which in turn boosts growth and promotes trade surpluses for commodities exporters such as one of the world’s biggest emerging markets, Brazil.

You can see the relationship between emerging market equities outperformance relative to developed markets and the value of the US dollar. Emerging markets outperformed developed markets when the blue line is going up.

Chart 3: MSCI EM/MSCI World ex Australia versus the US dollar

Source: Bloomberg to 31 December 2020

Emerging markets equities may also benefit from the rollout of COVID-19 vaccines which has resulted in a rally in so-called value stocks as markets are buoyed by optimism of a recovery. This benefits large industrial and cyclical companies, many of which dominate emerging equity markets.

In Jeremy Grantham’s latest asset allocation post, Waiting for the last dance he concludes, “Emerging Market equities are at 1 of their 3, more or less co-equal, relative lows against the US of the last 50 years. Not surprisingly, we believe it is in the overlap of these two ideas, Value and Emerging, that your relative bets should go…”

Why US dollar weakness is good for emerging market bonds

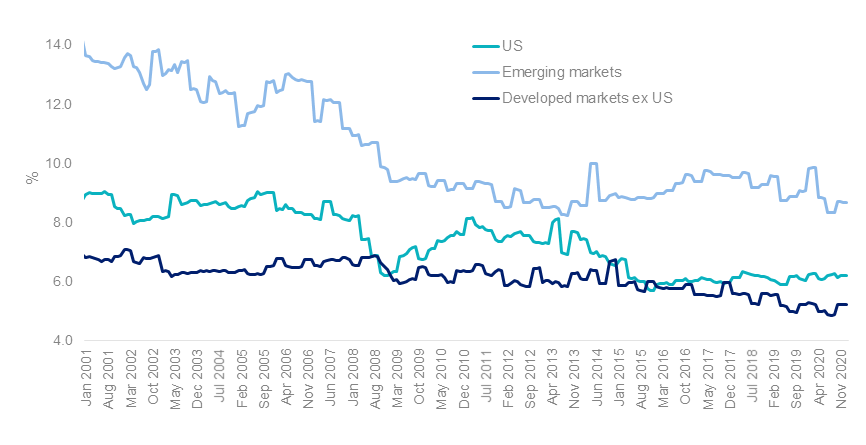

As many emerging markets governments and corporations issue their bonds in US dollars, when the US dollar falls it becomes easier for emerging market issuers to repay their debts (where the debts are set in US dollar). Due to the perceived increased risks in emerging markets the rates offered on these bonds are still generally higher than developed markets.

Chart 4: Effective interest rate paid on corporate debt

Source: DataStream/Worldscope, US is US Non-Financial - Effective Interest Rate, Emerging markets is Emerging Markets-Ds Non-Financial - Effective Interest Rate (please note for emerging markets only the rates for current country members are included for entire series), Developed markets ex US is World Ex US Non-Financial - Effective Interest Rate.

It is important to note however emerging markets are not a monolith and domestic factors play a huge role. This is where active management in emerging markets bonds can come to the fore. Active management allows the manager to avoid those countries with weaker fundamentals and prefer those emerging market economies that are better managed and therefore better insulated from geopolitical shocks that can occur in these developing nations.

Not that developed nations are immune from geopolitical risks, as Natalia Gurushina, our Chief Economist stated the day after the events in Washington on January 6, “Yesterday’s assault on Capitol Hill in Washington DC only strengthened our conviction about emerging markets as an asset class. Emerging markets’ share of global GDP is nearing 60%, they have higher growth rates, lower debt burdens, and improving macroeconomic policies. Many emerging markets are now “graduates” – or de facto developed markets. And don’t forget that we are actually getting paid for taking risks in emerging markets. Do I hear you asking about political noise? I think we got a pretty good answer to this question.”

Published: 18 January 2021

Issued by VanEck Investments Limited ACN 146 596 116 AFSL 416755 (‘VanEck’). Nothing in this content is a solicitation to buy or an offer to sell shares of any investment in any jurisdiction including where the offer or solicitation would be unlawful under the securities laws of such jurisdiction. This is general advice only, not personal financial advice. It does not take into account any person’s individual objectives, financial situation or needs. Read the PDS and speak with a financial adviser to determine if the fund is appropriate for your circumstances. The PDS is available here. An investment in EBND carries risks associated with: emerging markets bonds and currencies, bond markets generally, interest rate movements, issuer default, currency hedging, credit ratings, country and issuer concentration, liquidity and fund manager and fund operations. See the PDS for details. No member of the VanEck group of companies guarantees the repayment of capital, the payment of income, performance, or any particular rate of return from any fund.