What about Ukraine?

Federal Treasurer Josh Frydenberg and Minister for Superannuation Jane Hume released a joint statement earlier in the month that called on the $3.5 trillion super industry to sell Russian assets in light of the ongoing military conflict. Amid ongoing sanctions the value of these assets are close to zero. But what about the other side of the conflict? What about Ukraine?

Following Russia’s invasion of Ukraine, asset values in both countries plummeted. Economic sanctions enforced on Russia were swift. As a result, the Russian market became uninvestible. First MSCI said that it was pulling Russian securities from its emerging market equities indices. FTSE Russell swiftly followed suit and was joined by S&P Dow Jones and Morningstar. The moves were just as swift for fixed income indices. On March 7, JP Morgan announced that Russia would be excluded from all of its fixed income indices. Yet Ukraine remains. Ukraine enjoys the moral support of the rest of the world with governments and institutions like the IMF affirming their commitment to Ukraine.

JP Morgan runs the widely followed family of emerging market bond indices. These include a hard currency index known as EMBI, its corporate bond counterpart CEMBI and the local currency emerging market debt index GBI-EM. It is these indices, singularly or blended that most emerging markets bond investors use as their benchmarks.

For example, our actively managed emerging markets bonds ETF (EBND) aims to outperform a 50%/50% blend of EMBI (Hedged to Australian dollars) and GBI-EM.

The value of Russian and Ukrainian bonds collapsed following Russia’s invasion. While at the time, EBND didn’t have exposure to either country’s bonds, we have subsequently traded Ukrainian bonds. The reason we did not hold prior to invasion illustrates the importance of an unconstrained, active approach in emerging markets bonds. The accumulation of Ukrainian bonds could further illustrate this point.

Prior to the Russian invasion

In December Russia was around 5% EBND’s blended index. As you know, these are now worth close to zero. EBND did not have any exposure to Russia, so the portfolio was less impacted by the fall in Russian bond prices than funds that did have Russian exposure.

The reason we didn’t hold Russian bonds was that it failed our policy/politics screen, which is a part of our investment process. We believed the probability of sanctions was much higher than the market’s expectations, especially after President Biden was inaugurated, and we also believed that their price impact of any sanctions would have been larger than what markets had priced in.

What about Ukraine?

We think Ukraine is able to finance itself and therefore pay back the debt.

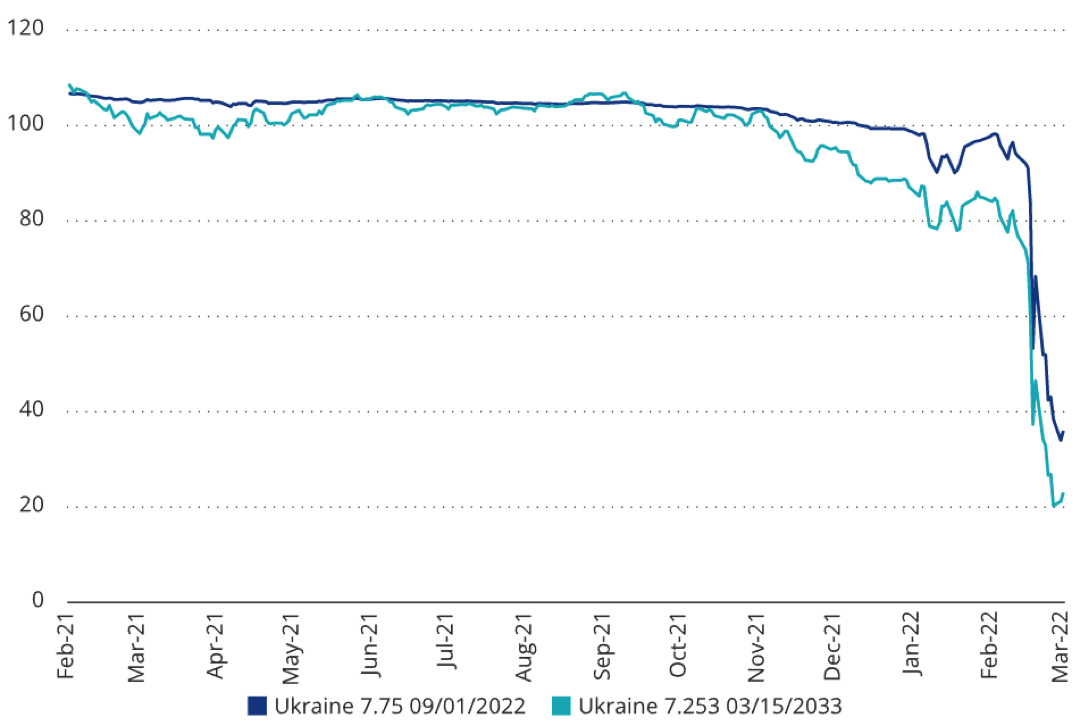

Chart 1 shows Ukraine ‘22s and ‘33s. The shorter-dated bonds are now trading at around 36 cents on the dollar, while the longer-dated bonds are trading around 23. The market seems to be pricing in a default. We think there may be potential upside if the Ukrainian government continues to function through to September. If Ukraine’s payment capacity is viewed by the market as more permanently intact, then that is supportive for Ukrainian bonds.

Chart 1: Ukraine International Bond Prices

Source: Bloomberg. Data as of March 8, 2022.

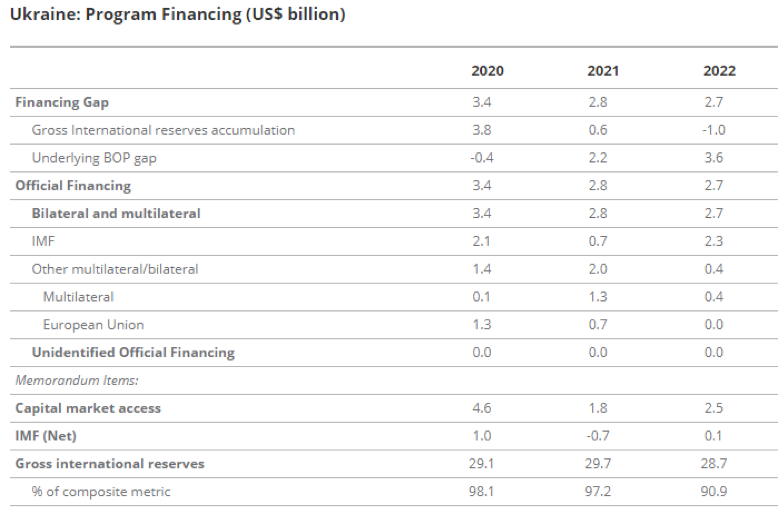

Ukraine has continued to make crucial bond interest payments despite the turmoil on the ground. If we review Ukraine’s external financing, we think the country is likely to be able to continue to finance itself. Table 1 shows Ukraine’s external financing requirement, and its financing, for 2020, 2021 and the forecast for 2022. The key thing to note is that 2022’s US$2.7 billion was fully funded by the official sector, before additional support that is being announced for Ukraine internationally.

Table 1: Ukraine’s External Financing in 2022

Source: IMF. BOP is defined as Balance of Payments (BOP) – it is the difference between all money flowing into the country in a particular period of time (e.g., a quarter or a year) and the outflow of money to the rest of the world.

While we didn’t hold Ukraine at the time of the Russian invasion, under our investment process, the country has improved on the metrics that had constrained us from owning it; its policy/politics score is improving. Our process considers and incorporates non-systematic risks like a war. The reason Ukraine’s policy/politics score has improved is that there has been an outpouring of international support for Ukraine that dwarfs its external financing requirements.

Not only is Ukraine already financed by official creditors, but the amount of financing that looks to be in the pipeline as a reaction to Ukraine’s invasion dwarfs current financing. These include:

- First, the European Union (EU) has welcomed Ukraine’s application to join. EU membership comes with significant funding. In countries like Poland, for example, it provides around 10% of budget financing. EU membership has transformed policy and led to a convergence of credit spreads in virtually all Eastern European member countries.

- The United States Congress is now considering legislation to provide Ukraine with US$6-US$10 billion in aid.

- The IMF has announced US$1.4 billion in additional financing, through a Rapid Financing Instrument (RFI).

- The IMF is likely to show forbearance, reflecting the international community’s attitude to the Ukraine. This is normal in situations like this, but the amount of international sympathy is high in this instance, based on our decades of experience considering such programs. What this means is that if ‘market financing, which in Ukraine’s case is assumed to be US$2.5 billion of bond issuance does not happen due to the invasion, the IMF is likely to compensate lenders.

- The Ministry of Finance of Ukraine informed its debtors that all of its regions are continuing to provide revenues to the central government. Remember that Crimea, Donetsk, and Luhansk (the latter two seceded from Ukraine) are already excluded from Ukraine’s financing assumptions, so the risk of Ukraine’s regions not providing revenue is already considered.

- The Ministry of Finance pledged to continue paying its obligations and, as noted above, paid the coupon due on 28 February 28 2022.

- Military spending could increase, but recent pledges by Germany and the EU make that likely to be foreign-funded going forward.

- There will be large reconstruction costs, but we see these as likely to be funded by international bilateral and multilateral agencies.

We continue to monitor the war and the politics from afar and our thoughts remain with those affected. While the region remains in conflict, we continue to actively manage our emerging markets bond portfolio in line with our philosophy. We believe an optimal portfolio of emerging market bonds is unconstrained by indices, and invests in bonds that offer the best value relative to their fundamentals while managing risk.

For more information on EBND click here.

Published: 17 March 2022

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange trades funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.