Gold and real yields: A new era of unconventional correlation

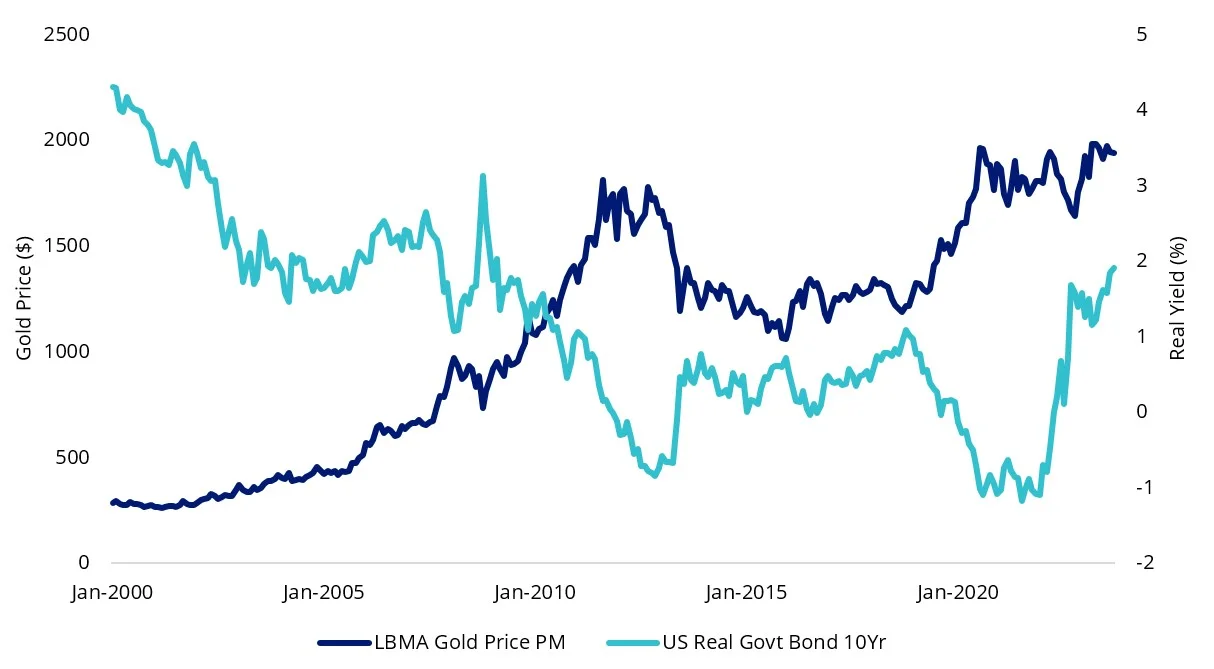

The recent rise in real yields has not coincided with a decline in the gold price, as history would lead us to expect. Let’s delve into the factors behind gold’s resilience and what peaking real yields could signify for the gold outlook.

Gold’s price has risen over the past twelve to eighteen months, while real rates have been flat. For years the price of gold was inversely correlated with US real yields. When real rates fell, demand for gold increased and vice versa. Demand for the yellow metal from central banks outside of the US and developed Europe and strong demand in China has kept the gold price relatively high. Now, with the spike in real rates potentially coming to an end, Western demand for gold could surge.

The long-term case for a stronger gold price remains and that an allocation to gold is an important diversification tool for portfolios. Previous rate hiking and inflationary environments have been supportive of the price of gold and it could go higher into the rest of 2023.

Gold and real yields

Real yields are positive when interest rates are higher than the rate of inflation. In 2020 they turned negative when rates fell to close to zero. As inflation spiked, rates had to rise faster for real rates to rise.

Historically, real yields and the price of gold have tended to be negatively correlated, that is, when real yields fall, the price of gold goes up, and vice versa. Unlike bonds, gold does not pay coupons, nor is there an interest rate attached. This means that when real yields are high, investors may be more inclined to move their money into assets such as bonds to earn a real return. Naturally, when the return of the assets is negative, in real terms, demand for gold increases.

But you can see in the chart below, that the recent rise in real rates, did not result in a corresponding fall in the gold price. Real yields haven’t been this high since 2009.

Chart 1: Real yield and gold price

Source: Bloomberg, August 2023. Past performance is not indicative of future results.

Central bank buying

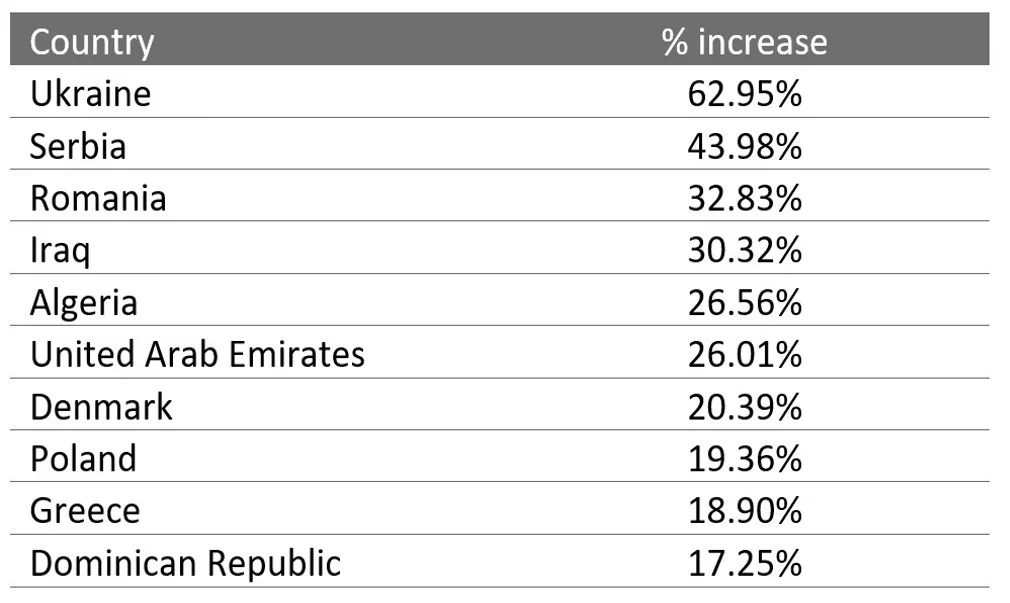

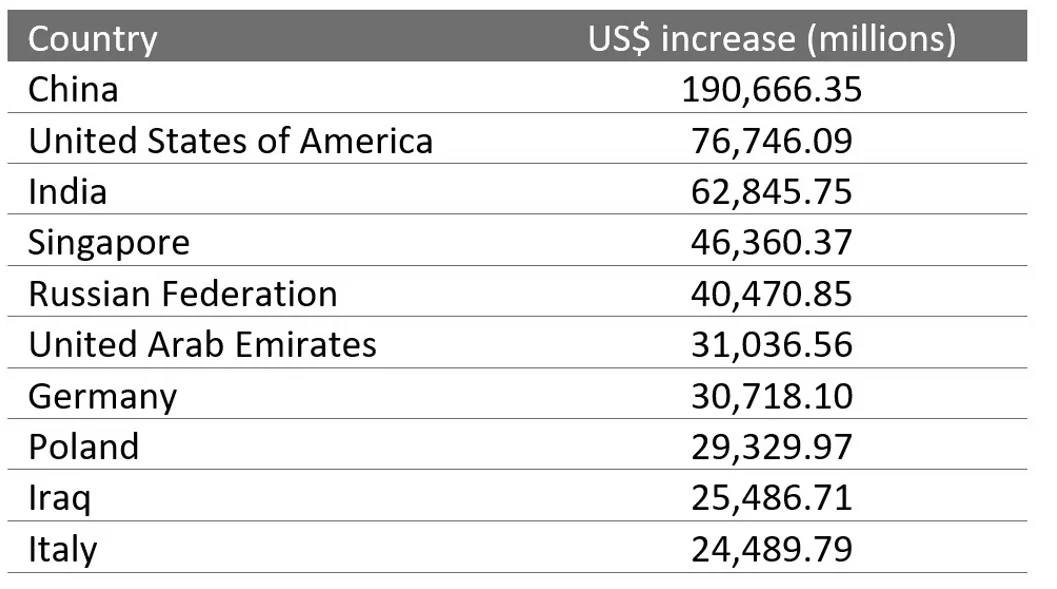

Normally in this environment, demand for gold falls, but that has not been the case this hiking cycle. Over the past four quarters, many central banks around the world have been accumulating gold reserves, and there has been a US$747 billion increase in gold reserves in central banks worldwide. Many of those central banks driving demand are not developed nations, so therefore are not as entwined to US real rates.

Table 1: Largest % increase in gold reserves over past four quarters

Table 2: Largest total increase in gold reserves over past four quarters

Source for table 1 and 2: World Gold Council, https://www.gold.org/goldhub/data/gold-reserves-by-country, Countries with less than US$10 billion removed from analysis.

As the Fed starts to slow down its rate hiking cycle, and inflation falls, real yields may stagnate or even reverse. Inflation is expected to continue to run well above the Fed’s 2% target.

Fed policy, recession fears lending further support for gold

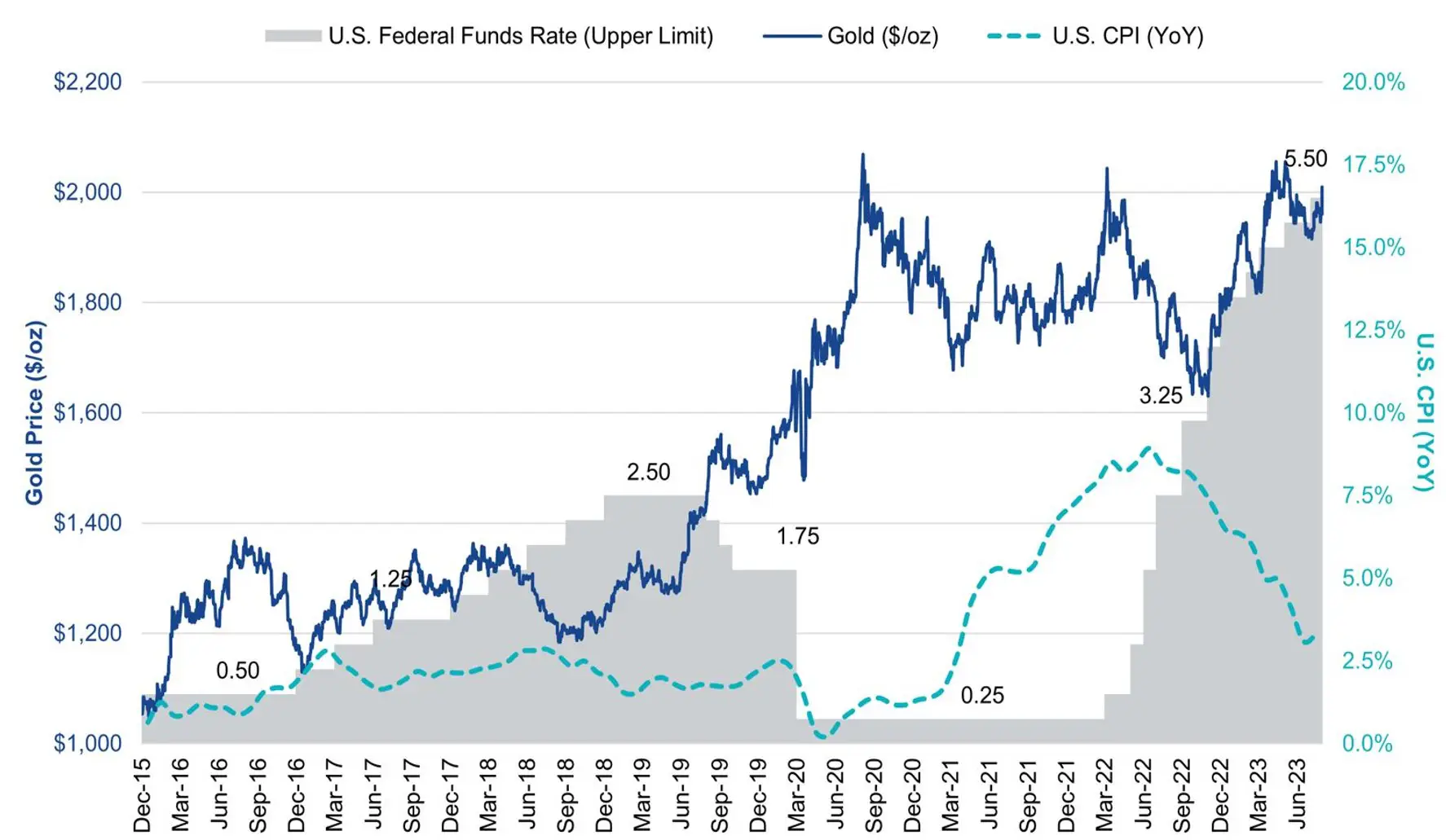

We expect that gold can rally further ahead of any Fed pause or pivot as the market becomes more certain that the end of the hike cycle is approaching. As developed market investors consider, gold trading up as the US dollar weakens in anticipation of a pause, we could see more and more gold buying.

Chart 2: Recent interplay between gold, target Fed rates and inflation

Source: Bloomberg, St. Louis Federal Reserve Bank (FRED). Data to 14 April 2023. Past performance is not indicative of future results.

Worsening financial conditions in 2024 are expected to lead to the end of the Fed’s rate hiking cycle. The market, though not the Fed (yet), is already pricing in cuts in the first half of 2024. This is positive for the price of gold. However, we believe the market has yet to price in the negative impact of a policy change in the fight against inflation and the increasing likelihood of any type of recession. Gold’s appeal increases in a recessionary environment.

Now could be a compelling entry point should more developed market investors seek gold’s role as an inflation hedge, as a safe haven in periods of economic, financial and geopolitical volatility, and importantly, as a portfolio diversifier.

Additionally, because changes in the price of gold in US dollar terms and AUD/USD currency movements are uncorrelated there is no investment rationale to hedge your gold exposure back to Australian dollars. Read why we believe that an unhedged exposure is the best way for Australian investors to access this asset class.

Gold as a portfolio diversifier

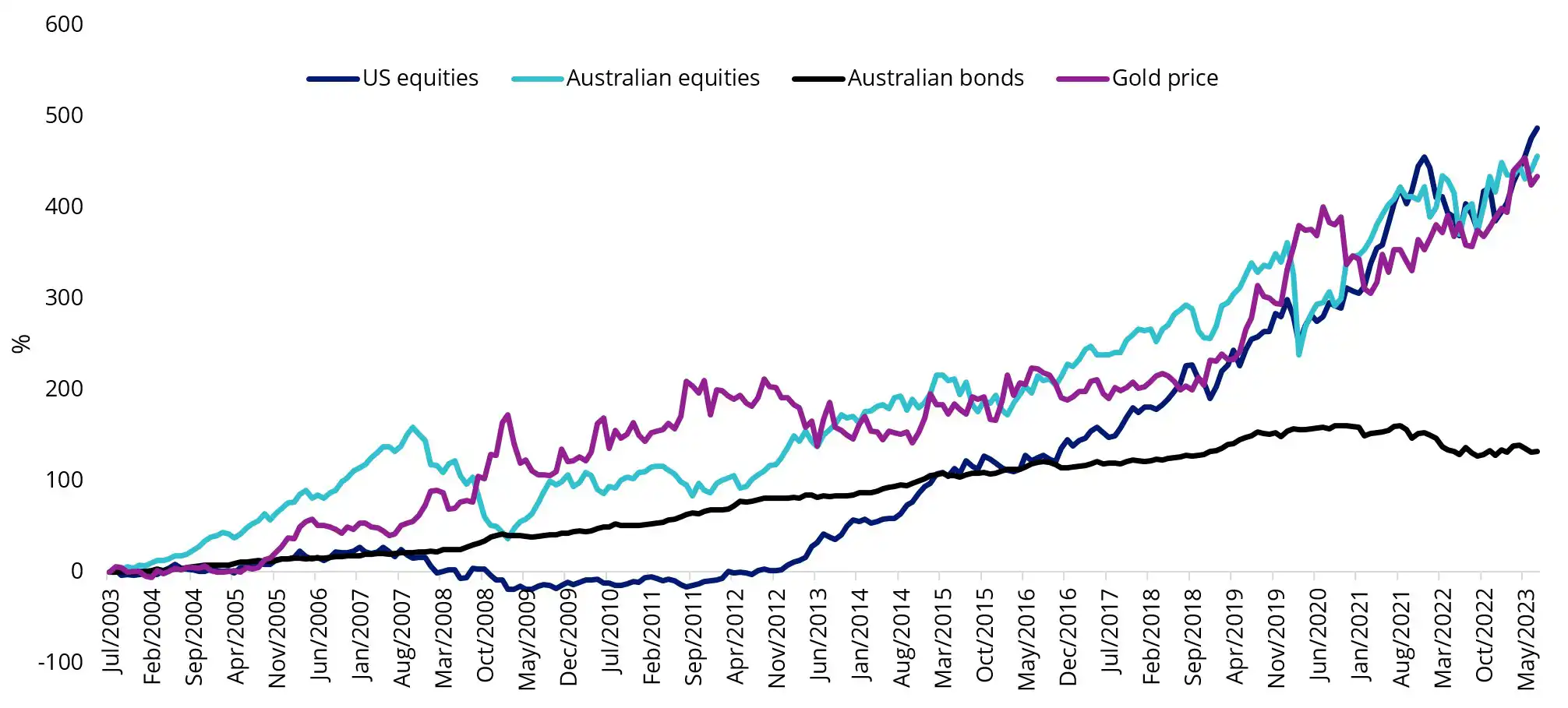

We have often stated that trying to “time” the gold market is futile. Because of its attributes, we believe that gold should be considered for a permanent allocation in any portfolio. Its low correlation with most other asset classes makes it an effective portfolio diversifier, which we have discussed previously in our Investors Guide to Gold. Black swan events cannot be predicted, but investors can be proactive and maintain a gold allocation that offers some protection when these events do happen. The performance of the gold price over the past 20 years, from an Australian investor’s point of view, should not be overlooked.

Chart 3: Twenty-year asset class performance

Source: Morningstar. All returns are in Australian dollars. US equities is the S&P® 500 Index. The gold price is LBMA PM Gold Price. Australian equities is the S&P/ASX 200 Index. Australian Bonds is Bloomberg AusBond Composite 0+ years Index. You cannot invest in an index. Past performance is not indicative of future results.

ETFs are an efficient and, we think, optimal way for investors to invest in gold. VanEck Gold Bullion ETF (NUGG) is the lowest cost, physically-backed gold bullion ETF on ASX.

Key risks of NUGG:

An investment in the ETF carries risks associated with: Gold pricing risk, currency risk, custody risk, gold bullion risk, concentration risk, liquidity risk, operational risk and regulatory and tax risk. See the PDS for details.

Published: 05 September 2023

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.