ANZ’s latest subordinated debt deal and how these bonds work

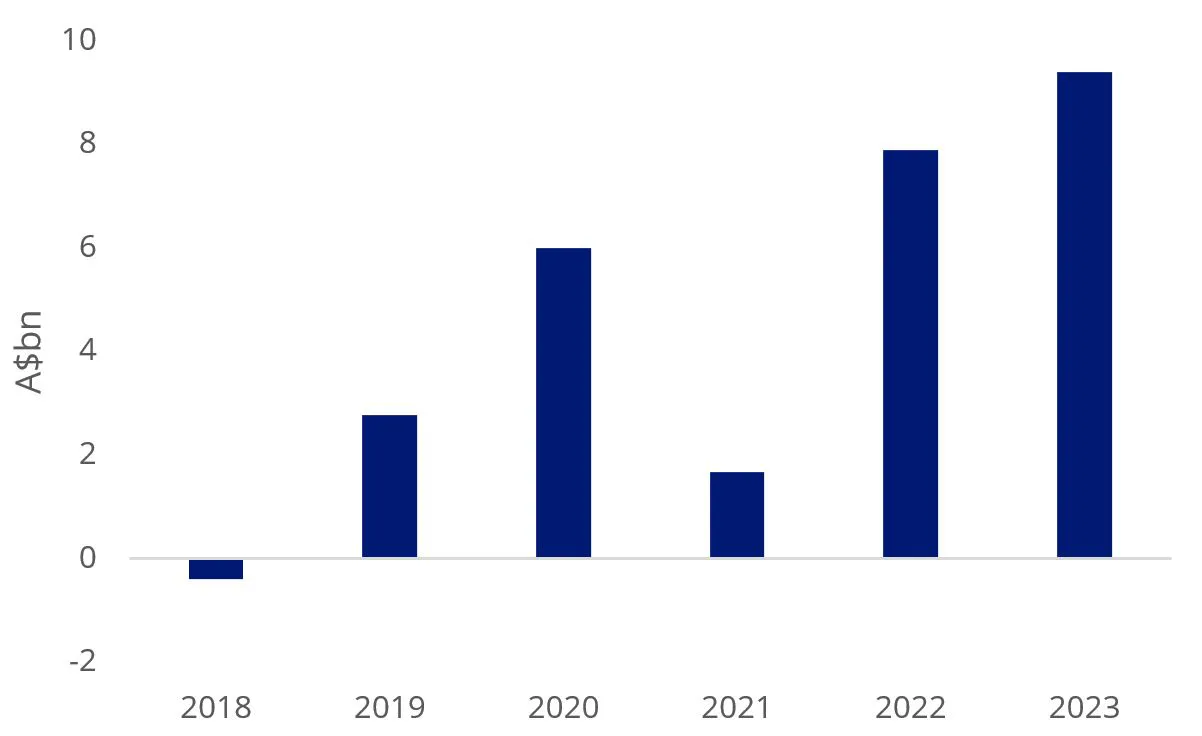

With inflation remaining stubborn and the APRA requirement for capital means that banks will need to continue to issue subordinated debt in 2024. Australian major bank net issuance was $9bn last year.

Chart 1: Major Bank AUD tier 2 net issuance

Source: Bloomberg.

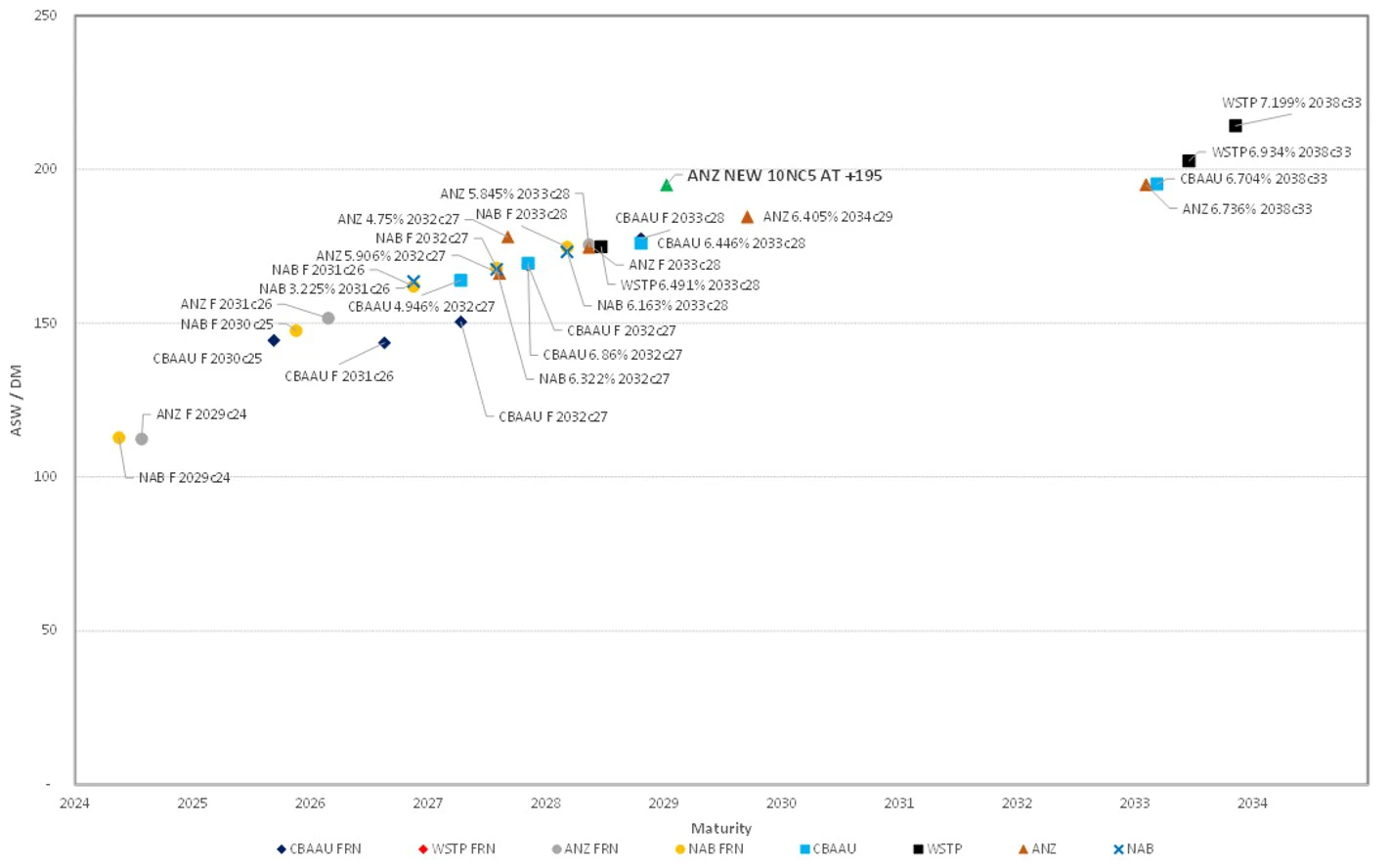

One such issue printed last week, ANZ’s $2.25 billion 10 year callable at 5 years (10NC5).

The deal was split between $850 million fixed to floating rate and $1.4 billion floating rate as was priced at 195 bps above the three month bank bill swap rate for floating rate, while the fixed to floating was 195 bps above the semi-annual quarterly asset swap (SQ ASW). This was 17 bps wider than the secondary market.

Figure 1: Major Bank AUD tier 2 curve

Source: Deutsche Bank, Bloomberg, As at 9 November 2023.

This follows Commonwealth Bank of Australia’s $1.25 billion issue in October last year that was also favourably priced. CBA’s floating rate slice priced at 205 bps above the three-month bank bill swap rate, while its fixed rate component priced at 205bps above SQ ASW.

Subordinated debt is becoming more and more important for Australian financial institutions as part of their obligations to fulfil APRA obligations.

How subordinated debt works

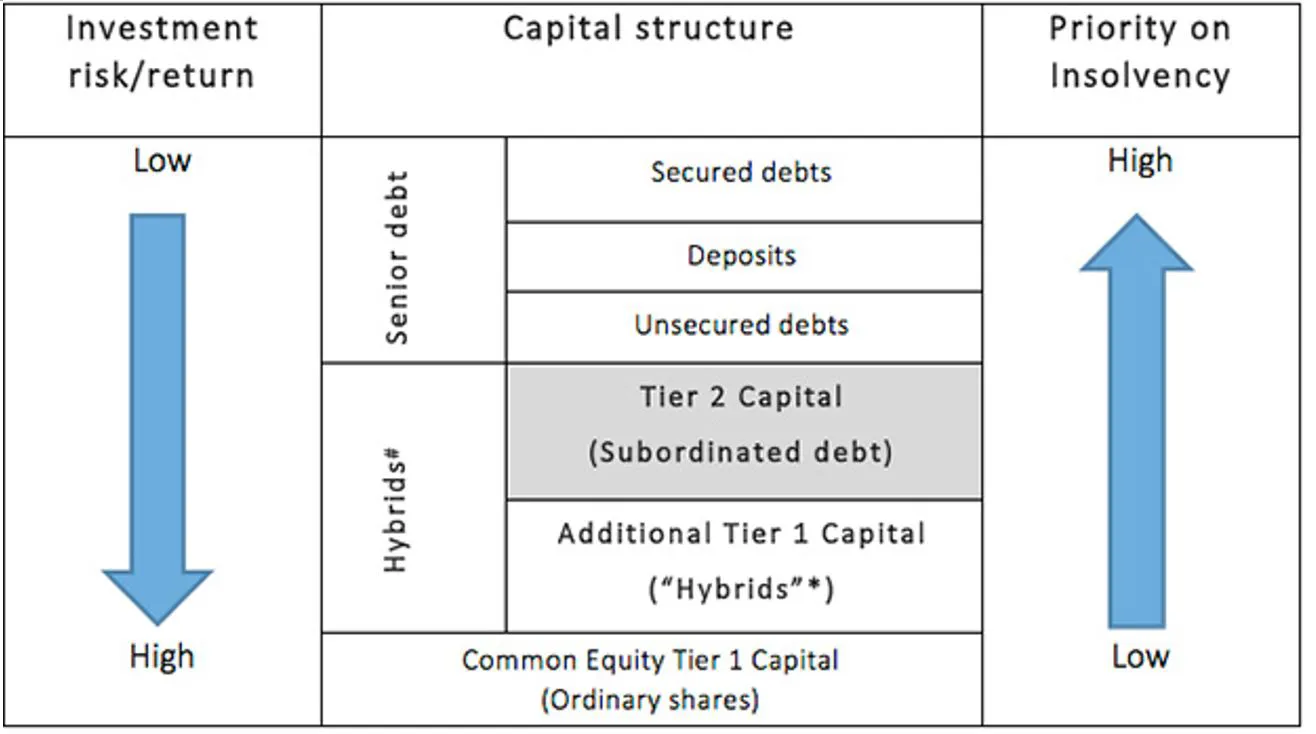

It is called ‘subordinated’ because it sits below ‘senior debt’ or traditional bonds in the capital structure, but it also sits above and takes priority over ordinary shares and hybrids, in the event of insolvency. See the shaded area in the chart below which provides a simplified example of the capital structure in a financial institution to illustrate how different securities issued by financial institutions rank in priority of payment in the event of collapse.

Figure 2: Simplified capital structure of a financial institution

#Per ASIC Report 365. *Per market convention.

You can see from the above chart that in the event of insolvency, priority is given to deposits and other senior debt. Shareholders get paid last, if at all.

Using subordinated bonds in a portfolio

The current higher interest rate environment and corresponding increase in credit risk premium given the uncertain economic outlook has improved yields on corporate bonds. In addition, sticky inflation has put a pause on predictions for immediate rate cuts.

Since subordinated debt ranks below traditional bonds and above hybrids, it is therefore considered more risky than traditional bonds and less risky than hybrids. As a result, financial institutions typically offer subordinated bonds with a higher interest rate than traditional bonds, but a lower interest rate than hybrids.

Because they are floating, they tend to do better when interest rates are rising and vice versa.

Subordinated bonds can be used to enhance the return on the fixed income portion of an investor’s portfolio or as an alternative to Additional Tier 1 Capital securities. Traditionally, they have only been available to wholesale investors, but they can be accessed on ASX via the VanEck Australian Subordinated Debt ETF (ASX code: SUBD).

Key risks

An investment in the ETF carries risks associated with: subordinated debt, bond markets generally, interest rate movements, issuer default, credit ratings, fund operations, liquidity and tracking an index. See the PDS for details.

Published: 16 January 2024

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.