Global healthcare in good stead

We think the current environment bodes well for healthcare which is considered a defensive sector, possessing characteristics that tend to outperform during economic uncertainty. Healthcare has a relatively low correlation with the rest of the global economy and is being supported by an aging population and growing middle class. This places it, we think, in good stead in the current stage of the economic cycle.

The Australian and developed global markets are experiencing central banks tighten monetary policy in an effort to fight inflation. This fight has had its casualties, local company Milkrun announced recently it was going into administration, while on a global scale poorly managed US Regional banks as well as Swiss bank, Credit Suisse, have suffered distress events.

Investors have had limited places to hide.

Diversification is an important tool in the construction of an investor’s portfolio. It can mitigate losses and capture upside.

Astute investors aim to achieve true diversification, requiring a disciplined approached that deploys capital in an equitable manner across important facets of the global and local economy. Often, however, they can be obstructed by a concept in behavioral finance known as ‘home bias’, that is investing their capital predominantly locally, consequentially hindering their ability to extract the true benefits from global companies or different sectors such as the ones mentioned above.

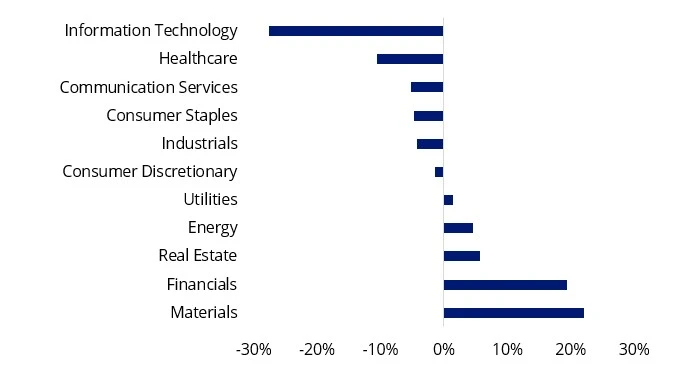

An example in the Australian market is the sector composition which is heavily concentrated toward financials and materials. Heathcare is an example that is under-represented in the S&P/ASX 200 compared to the global MSCI World Index, by 10.52%1.

Chart 1: S&P/ASX 200 Active Weights vs MSCI World

Source: Bloomberg S&P, MSCI, as at 28 April 2023. Indices used: AS51 Index - S&P/ASX 200 and MXWO Index - MSCI World Index

While the Australian Healthcare sector is small, it’s also dominated by one big player, CSL. ETFs provide investors an opportunity to gain exposure to underweight sectors beyond the Australian market in sectors such as healthcare.

Diversified exposure to healthcare is difficult to obtain by buying individual stocks or market capitalisation strategies because this can result in unintended risks such as concentration to certain names thereby taking on the business risk of a handful of companies rather than the holistic sector performance.

Healthcare, we think, is one such sector where a more diversified approach may be appropriate and there are a number of tailwinds supporting the sector.

In the United States, for example, the sector is benefiting from a more accommodative Food and Drug Administration (FDA), greater clarity around drug pricing as a result of the 2016 US election and from support within the Inflation Reduction Act.

We also think there is a greater potential for increased M&A activity, as larger capitalised players have high cash reserves and interest rates may soon stabilise.

This backdrop provides an opportunity Australian investors often overlook.

One of the companies that became a household name during the COVID-19 pandemic was Moderna Inc, a biotechnology company that focuses on developing mRNA therapies and drugs for infectious, immune-oncology and cardiovascular diseases. Its price was initially swept up in the early COVID-19 hysteria, since then shedding 62% from its highs. Valuations look more compelling for investors with a trailing price-to-earnings (P/E) of 11.47 and price-to-book (P/B) of 2.711. The company also has strong long-term opportunities in their pipeline as well as a revenue stream from COVID boosters. In partnership with Merck, Moderna is developing a cancer vaccine, which is currently in Phase 2 trials. The results so far are promising compared to what is currently available for reducing the risk of death and cancer reoccurrence in melanoma patients. Additionally, Phase 3 data for a respiratory syncytial virus (RSV) vaccine has indicated at an 83.6% efficacy against mild disease. Moderna also seems to be closer than its competitors developing a combined COVID-19, flu and RSV vaccine.

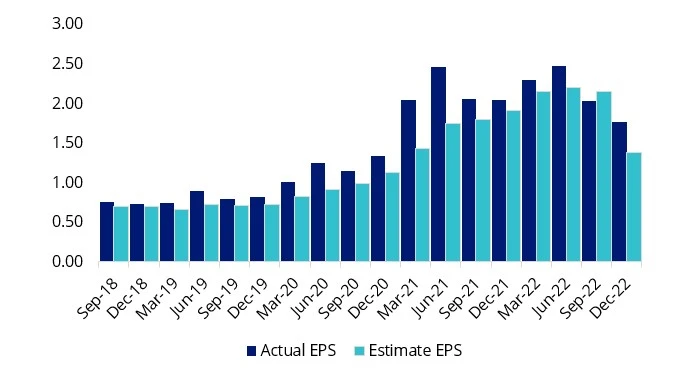

Biotechnology companies aren’t the only potential beneficiaries of the current environment. West Pharmaceutical Services Inc operates in medical equipment and services with a diverse reach in the US, South America and Europe. Its goods are often provided at a low-cost relative which has provided robust growth. They provide laboratory drug delivery and medical equipment design and development, such as containment and packaging. These products include seals and stoppers for injectables (70% of the market), syringe components and injection systems. They also provide services in more complex solutions for intricate medical devices. The stock has seen significant uptick in performance recently due to its long-dated success in market dominance, a sustainable growing demand as well as strong management and corporate governance. One demonstration of this is its ability to have consistent reoccurring EPS surprises.

Chart 2: Quarterly EPS Surprises

Source: Bloomberg. Not a recommendation to act.

VanEck’s Global Healthcare Leaders ETF (HLTH) gives investors exposure to a diversified portfolio of the largest international companies from the global healthcare sector. HLTH tracks the MarketGrader Developed Markets (ex-Australia) Health Care Index (HLTH Index), and currently includes companies like Moderna and West Pharmaceuticals, that deliver growth at a reasonable price (GARP). Companies are selected on the basis of the strength of 24 fundamental indicators across four factor categories:

-

- Growth;

- Value;

- Profitability; and

- Cash flow.

The HLTH Index identifies the top 100 companies with the best GARP attributes, selects only the top 50 by market capitalisation, then equally weights the constituents. The result is a portfolio of 50 fundamentally sound and attractively valued companies with the best growth prospects in the healthcare sector.

HLTH has a higher EPS and sales growth as expected by its growth characteristics. This is coupled with the comparatively lower price to earnings and price to cashflow which exemplifies the reasonable price aspect of the approach.

Source: FactSet, as at 28 April 2023.

Key risks

An investment in the ETF carries risks associated with: ASX trading time differences, financial markets generally, individual company management, industry sectors, foreign currency, country or sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the PDS for details.

Published: 24 May 2023

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange trades funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.

"MARKETGRADER" and “MARKETGRADER DEVELOPED MARKETS (EX-AUSTRALIA) HEALTH CARE INDEX” are trademarks of MarketGrader.com Corp. and have been licensed for use for certain purposes by VanEck. HLTH is based on the MARKETGRADER DEVELOPED MARKETS (EX-AUSTRALIA) HEALTH CARE INDEX, but is not sponsored, endorsed, sold or promoted by MarketGrader, and MarketGrader makes no representation regarding the advisability of investing in HLTH.