Conflicts and markets: Investor considerations

Markets and geopolitics are both unpredictable, yet are entwined. As war wages on in Europe, the Middle East has become a new battleground of conflict, and the effects of both weigh on markets.

Markets have moved with such speed and velocity, in both directions since 7 October it has been difficult for investors to adjust with so much information and misinformation being circulated. That and they have to reflect on the human impact too.

Wars create uncertainty, impact lives, generally have a negative impact on the economies and weigh on markets.

The outbreak of World War 1 resulted in the US share market falling by an estimated 18% in three months. World War 2 resulted in a ~30% drop. So far, since the 7thof October, the gold price has risen, recently surging through its US$2,000 price barrier for the first time since May, while uncertainty has weighed on equity markets. This makes sense because investors have used gold as a safe-haven asset in times of uncertainty, hence its place in many long-term diversified portfolios.

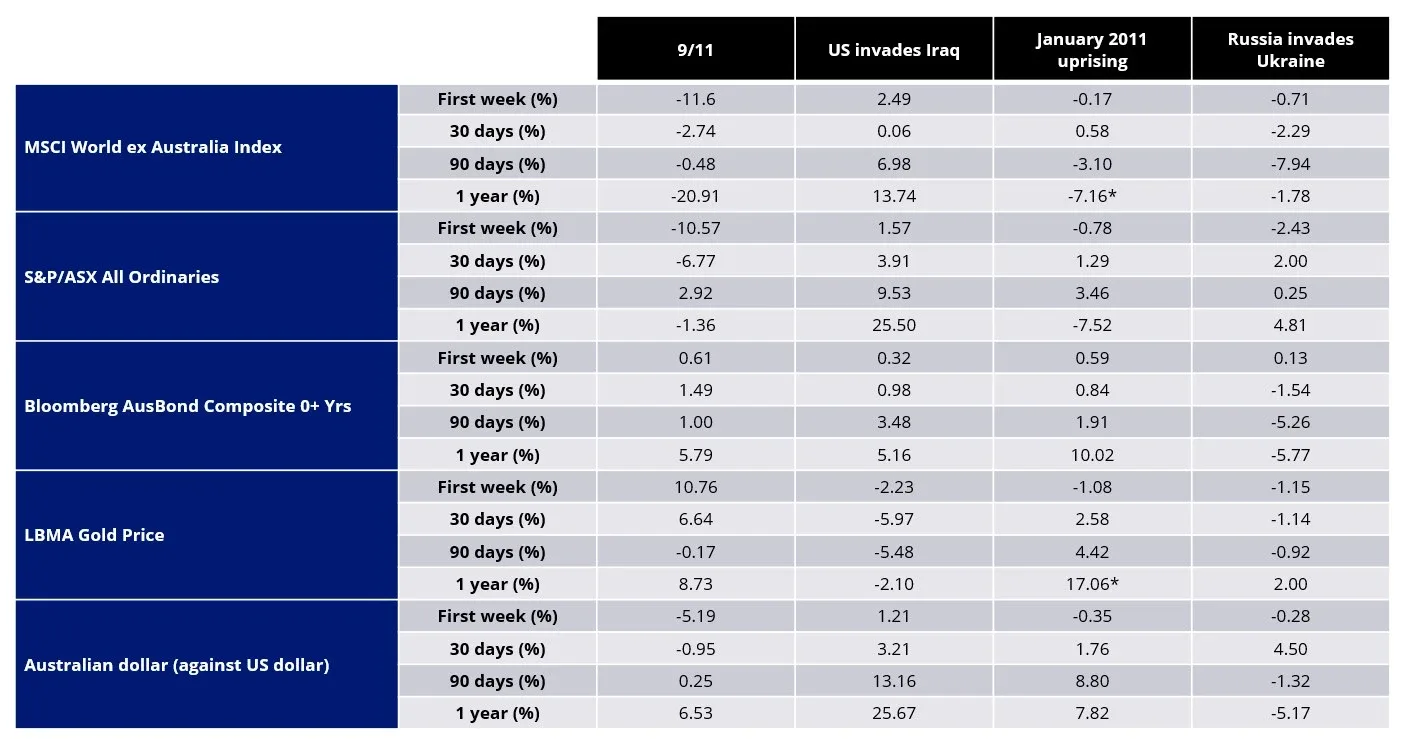

Conflicts since the two world wars have tended to be confined to smaller geographic areas, but that is not to diminish their potential to overflow beyond borders. The table below highlights four events since the turn of the century and their impact on the returns of share and bond markets, the gold price and our currency.

Table 1: Performance impact of major geopolitical events since the turn of the century

Source: VanEck, MSCI, S&P, Bloomberg, Morningstar, ABS *captures the period of European debt crisis. You cannot invest in an index. Past performance is not a indicator of future performance.

What is evident is that no two crises or conflicts had the same impact on markets. Different factors, such as the nature of the event can influence share market returns in the immediate term, but as time goes on, there may be other factors that have an even bigger influence on markets. 2011’s European Debt crisis arguably had a bigger impact than the uprising in 2011, though at the end of January of that year, as more nations’ rulers were deposed, markets seemed to be on the brink.

Today the geopolitical complex, in the information/digital age we live in, adds greater complexity. Investors’ reactions are often made in haste, with incomplete information and this can influence other reactions.

Markets tend to recover from these types of events. What we do know is that these events are rarely predictable, and their long-term impact is always unknown.

In markets, investors are often making decisions based on small samples, unknown outcomes and exaggerated pessimism and optimism.

It’s probably worthwhile revisiting, how humans make decisions when confronted with uncertainty. These lessons seem important because uncertainty seems to be a constant for investors.

Nobel prize-winning Daniel Kahneman and his colleague, Amos Tversky have shown that people make poor decisions when faced with uncertainty. Their research highlighted three decision-making processes that people use to assess probabilities or make estimations:

- representativeness;

- availability; and

- adjustment and anchoring.

A better understanding of these processes, which all humans often quickly go through, could improve judgments and decisions in situations of uncertainty especially if we are aware of our inherent biases.

Representativeness

One example Kahneman and Tversky use to explain a judgement that uses representativeness asks us to consider Steve. Steve is described as a shy, withdrawn person with little interest in people. Steve needs order and structure. He is described as a meek and tidy soul. Now we must assign Steve an occupation from a list of probabilities (for example, farmer, salesman, pilot, librarian, GP). Representativeness is the process that we use to assess Steve. We assess what we are told about Steve against the degree to which he is representative of the stereotype of the occupations in the list and many people would conclude that Steve is a librarian. This approach can lead to serious errors because representativeness does not consider several factors that should affect judgements of probability. These errors include insensitivity to probability and sample size.

Insensitivity to probability – There are more farmers in the world than librarians, yet when we consider what occupation Steve has, we do not consider this information. It is much more likely that Steve is a farmer because there are so many of them. Even when researchers’ experiments included relevant population statistics, the relevant probabilities were ignored when descriptions, even irrelevant ones, were given.

Insensitivity to sample size – People assign their knowledge or ‘averages’ to represent samples without regard to the size of the sample. This can lead to errors. For example, after being told the average height of a man is 5’9”, when people are then asked to assign the probability that a random sample of men would be higher than 6’ for different sample sizes, time and time again people suggest the probability is the same for a sample of 10,000, 100 or 10. This is flawed because only as a sample gets larger it is more likely to be closer to the 5’9”, smaller samples are more likely to stray from the mean.

Representativeness causes humans to be unreliable in estimating probabilities in smaller samples. People need to be aware of this. We think it is unlikely, for example, that the S&P/ASX All Ordinaries will return 9.65% 12 months after a geopolitical event, even though that is the average of the 1-year row in the table above, a sample of only four.

Availability

Availability is the decision-making process of assigning the likelihood of an outcome by the ease with which instances can be remembered.

According to Kahneman and Tversky, “For example, one may assess the risk of heart attack among middle-aged people by recalling such occurrences among one’s acquaintances.” This leads to biases, often overestimating the likelihood of occurrence.

Recent occurrences too are likely to be more readily remembered and therefore will increase the estimation of occurrence. Furthermore, the impact of an experience will impact decisions. For example, the impact of seeing (or even hearing about) a shark attack will have an impact on your assessment of the probability of a shark attack.

These geopolitical events are like shark attacks. They are rare. Investors, like swimmers, should exercise caution, but they shouldn’t stop you from trying to seek your long-term investment goals.

Adjustment and anchoring

Finally, it is useful to remember we are bad at assessing risks and nothing illustrates this more than the way we anchor and adjust our estimates. The experiment that best highlights this involves two groups of students. One group is asked to estimate the answer for:

1 x 2 x 3 x 4 x 5 x 6 x 7 x 8

The other estimates the answer for:

8 x 7 x 6 x 5 x 4 x 3 x 2 x 1

Kahneman and Tversky hypothesised that adjustments we make quickly when estimating are typically too low, so the resulting guess will be lower than the real answer. Furthermore, because the result of calculating an estimate is based on a starting point, which is established in the first few steps of making an estimate, estimates will be higher in the descending sequence than the ascending sequence. This is because the descending sequence, anchored by a higher starting point, should give a higher ‘estimate.’ The results of Kahneman and Tversky’s experiment confirmed both predictions. “The median estimate for the ascending sequence was 512, while the median estimate for the descending sequence was 2,250. The correct answer is 40,320.”

As investors, we may have been anchored by the horrific pictures coming out of the Middle East. The estimation of the impact on the price of oil, for example, may have been overestimated.

The lesson from the current crisis

Kahneman and Tversky’s proved we are poor decision-makers when faced with uncertainty. In markets and geopolitics, uncertainty is the only constant. Successful long-term investors survive short-term volatility by sticking to investment principles that have withstood the tests of time. For portfolios, this may include better diversification. For equities, investing in profitable companies with strong balance sheets and stable earnings has historically given resilience to portfolios. But it’s important to stay the course. We think 2022 and 2023 could become a case study in the rationale for looking beyond the positive and negative commentary and concentrating on long-term goals.

Published: 08 November 2023

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.