Sustainable investing gets boost from COVID-19 and Australian investors

In last Tuesday’s Chanticleer, on the back page of the Australia Financial Review, a story outlining MSCI’s push to lure superannuation funds to its range of ESG indices appeared. It is evident from the article:

- ESG is going to be a focus for Australia’s largest superannuation funds;

- MSCI is a market leader creating ESG indices for passive investments to track; and

- In 2020 one of MSCI’s ESG indices outperformed the broader Australian equities market.

Sustainable investing has received a boost from COVID and the demands of Australia’s most demanding investors.

Super’s green push lures MSCI ran on the back page of the Australian Financial Review last Tuesday. It is evident from the article:

- ESG is going to be a focus for Australia’s largest superannuation funds;

- MSCI is a market leader creating ESG indices for passive investments to track; and

- In 2020 MSCI’s ESG indices outperformed the broader Australian equities market.

This has not been a phenomenon unique to Australia. Globally, sustainable investing accelerated during the COVID-19 pandemic, with more investors taking environmental, social and/or governance (ESG) factors into account and investors often reaping an extra return for that consideration.

The COVID-19 pandemic has focused investors’ attention on the vulnerability and resilience of communities and intensified discussions around sustainability. Social factors have taken on greater importance as the health and safety of communities worldwide has become a significant consideration for investors. Other events, such as the horrific death of George Floyd and the aftermath had investors considering the ‘social’ factor. In addition to these, bushfires and climate change added to the importance of considering environmental factors in investment decision-making in 2020.

These considerations – climate change, the Black Lives Matter movement and the COVID-19 pandemic – have concentrated investors’ minds on ESG factors and more companies are being challenged for substandard behaviour and poor management of ESG factors.

This is evidenced by Google Trends, the search term “ESG” has never been as popular as it is today. Compared to early March 2020, the number of searches for ESG had doubled by January 10-16, 2021.1 This highlights that people are increasingly seeking information on the topic.

Performance lift from ESG

Added to a greater awareness of ESG is that we now know that doing good has helped some companies to perform better financially during this crisis. Last year, MSCI, one of the world’s largest index providers released a research paper, Five Lessons for Investors from the COVID-19 Crisis, which we discussed here.

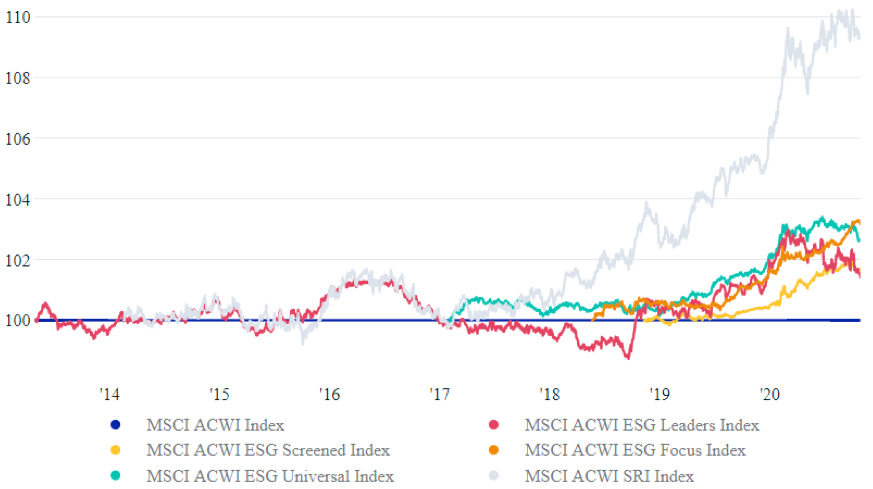

The experience through the COVID-19 pandemic highlights that ESG investing is more than just an ethical consideration. Taking into account ESG factors helped to lift shareholder returns during the COVID-19 pandemic. This outperformance during the pandemic has added to the long-term track record of these indexes, as can be seen in the exhibit below, which displays the longest available history for major MSCI ESG global equity indexes compared to MSCI All Country World Index (ACWI).2

Figure 1 Performance of MSCI ACWI ESG Indices since inception vs MSCI ACWI

Source MSCI blog: Is ESG Investing a Price Bubble? Probably not. Dated 9 December 2020. Data from May 31, 2013, to Nov. 30, 2020. MSCI ESG Universal Index represents an ESG weight-tilt approach; MSCI ESG Leaders is a 50% best-in-class sector approach; MSCI SRI is a 25% best-in-class sector approach; and MSCI ESG Focus is an optimized approach designed to maximize ESG exposure. The data shows live-track performance for each index: MSCI ACWI ESG Leaders has been live since June 6, 2013; MSCI ACWI SRI since March 24, 2014; MSCI ACWI ESG Universal since Feb. 8, 2017; MSCI ACWI ESG Focus since June 25, 2018; and MSCI ESG Screened since Dec. 14, 2018.

Previous research from MSCI had shown that companies with high MSCI ESG ratings showed lower levels of systematic risk, lower cost of capital and higher valuation levels — measured by price-to-book and price-to-earnings (P/E) ratios — compared to companies with low MSCI ESG ratings in the MSCI World Index from January 2007 through May 2017.3 This valuation premium is also noticeable in MSCI ESG indices, as shown in the table below.

Figure 2 Valuation Measures of MSCI ESG indices Compared to MSCI ACWI

|

|

MSCI ACWI Index

|

MSCI ACWI ESG Screened Index

|

MSCI ACWI ESG Universal Index

|

MSCI ACWI ESG Leaders Index

|

MSCI ACWI ESG Focus Index

|

MSCI ACWI SRI Index

|

|

Price to book

|

2.2

|

2.2

|

2.3

|

2.5

|

2.2

|

2.5

|

|

Price to cash earnings

|

11.2

|

11.6

|

11.6

|

12.0

|

11.5

|

12.4

|

|

Price to earnings

|

18.8

|

18.9

|

18.9

|

19.2

|

18.7

|

19.6

|

Source: MSCI, data from May 31, 2013 to Jan 29, 2021

This supports several other research pieces which have found a link between ESG investing and performance.4 Dr Philipp Krueger, an Assistant Professor of Responsible Finance at the University of Geneva, has studied the relation between ESG characteristics and investment performance. Krueger says:

High sustainability footprint investors also display higher risk-adjusted performance … We further document that this enhanced risk-adjusted performance of high sustainability footprint portfolios is primarily driven by a strong reduction in total portfolio risk, suggesting risk mitigation as being one of the main channels through which portfolio-level sustainability generates long-term value.5

ESG fund inflows rise sharply

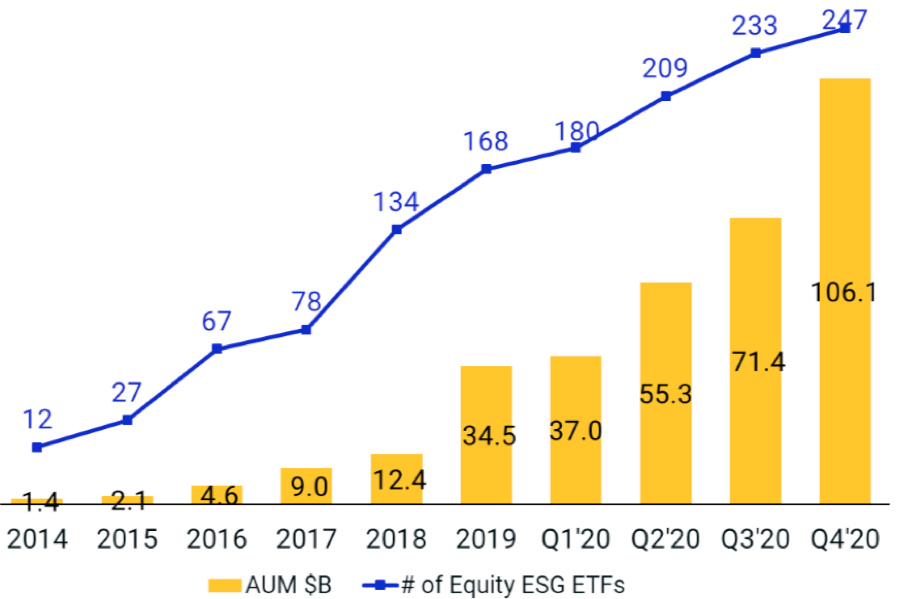

Inflows into ESG funds have soared in recent years and months, in part motivated by outperformance since the COVID-19 pandemic erupted. Over the past four years, inflows into ESG funds have surged. For instance, the growth in ETFs tracking MSCI ESG indices has risen sharply, measured in terms of the number of ETFs and assets under management (see the chart below). The acceleration of inflows and strong performance has driven up prices for high-ESG-rated companies and thus pushed up returns for ESG investments.

Figure 3: ETFs Based on MSCI ESG Indices

Source MSCI, December 2020.

ESG analysis takes a lot of work

Careful analysis is required of a company’s policies, procedures and practices before investors can fully assess its ESG worthiness.

Considerations as varied as labour standards, workplace diversity including gender and ethnic diversity, efficiency of resource use, risk controls, management competency, environmental impacts and whether a company produces controversial products such as weapons or adult entertainment, are just some factors which need to be considered as a part of an ESG framework.

While such analysis has traditionally been the domain of active funds management, MSCI is now the leading global ESG researcher. With its large team of analysts and extensive research, its ESG ratings can help investors avoid the risk of an ESG failure overwhelming a company’s financial performance or reputation.

Many active fund managers maintain that they incorporate ESG factors into their investment analysis. However, investors need to ask whether their ESG analysis is in-depth or superficial. If they don't have a big team crunching the numbers and examining all aspects of a company's management operations, corporate policies and governance, then their ESG analysis is likely to produce little insight.

The adoption of an index can help asset owners apply a consistent approach to integrating ESG at both the strategic asset allocation level as well as across all individual allocations. Superannuation funds and institutions have been gradually adopting greater ESG investment. MSCI found in its Integrating ESG into Benchmarks paper6 that switching to an ESG policy benchmark such as tracking an index may lead to a more consistent approach across an entire investment portfolio than adopting an ad hoc or arbitrary approach to ESG integration.

Swiss Re, one of the world’s largest reinsurers, in 2017 said it would shift its entire investment portfolio worth around US$130 billion to MSCI’s ESG indices family, choosing benchmarks that systematically integrate ESG criteria rather than more traditional benchmarks. Guido Fürer, Group Chief Investment Officer at Swiss Re, said MSCI benchmarks “represent a suitable tool to achieve the desired investment behaviour and set the right measurement both from a performance and ESG perspective.”7

In Australia, institutional investors have been at the forefront of sustainable or responsible investing. It is estimated that around $1.9 billion in assets under management (AUM) is controlled by Australian investment managers known to be applying responsible investment to some or all of their investment practices. That amounts to 60% of the professionally managed AUM, according to the Responsible Investment Benchmark Report 2020 from the Responsible Investment Association Australasia.8

Exchange traded funds (ETFs) can be used to readily meet the demand for ESG investments from retail investors, self-managed superannuation funds, and institutional investors including large super funds. VanEck has two ETFs focused on sustainable and ESG Investing: VanEck MSCI International Sustainable Equity ETF (ESGI) and the VanEck MSCI Australian Sustainable Equity ETF (GRNV). Both ESGI and GRNV track MSCI indices that screen for fossil fuels and socially responsible investments combined with targeting ESG leaders.

Further details about index methodologies and revenue screens can be found on our respective fund pages for ESGI and GRNV, where you can also find our quarterly reports which outline the carbon intensity and ESG exposure of these two portfolios.

Published: 12 February 2021

IMPORTANT INFORMATION

VanEck MSCI International Sustainable Equity ETF (ESGI) and the VanEck MSCI Australian Sustainable Equity ETF (GRNV) are issued by VanEck Investments Limited ACN 146 596 116 AFSL 416755 (‘VanEck’). This is general advice only, not personal financial advice. It does not take into account any person’s individual objectives, financial situation or needs. Read the PDS and speak with a financial adviser to determine if either fund is appropriate for your circumstances. The PDS is available here. An investment in ESGI carries risks associated with: financial markets generally, individual company management, industry sectors, ASX trading time differences, foreign currency, country or sector concentration, political, regulatory and tax risks, fund operations and tracking an index. An investment in GRNV carries risks associated with: financial markets generally, individual company management, industry sectors, fund operations and tracking an index. See the PDS’s for details. No member of the VanEck group of companies guarantees the repayment of capital, the payment of income, performance, or any particular rate of return from any fund.

ESGI and GRNV are indexed to a MSCI indices. ESGI and GRNV are not sponsored, endorsed or promoted by MSCI, and MSCI bears no liability with respect to ESGI, GRNV or the MSCI Index. The PDS contains a more detailed description of the limited relationship MSCI has with VanEck and the funds.

1 https://trends.google.com/trends/explore?q=esg,environmental%20social%20and%20corporate%20governance

2 https://www.msci.com/www/blog-posts/is-esg-investing-a-price-bubble/02231869256

3 ibid

4 A report from Federated Hermes International, ESG investing: does it just make you feel good or is it actually good for your portfolio? has unearthed a strong correlation between ESG corporate governance and shareholder returns over the short and long term. Research from JP Morgan, A Quantitative Perspective of how ESG can Enhance your Portfolio, has found a link between good ESG governance and improved financial performance. In its 2015 research paper, Finding Alpha in ESG, Credit Suisse finds that portfolios constructed based on ESG data added alpha over a seven-year time horizon.

5 Gibson, Rajna and Krueger, Philipp, The Sustainability Footprint of Institutional Investors (January 14, 2018). Swiss Finance Institute Research Paper No. 17-05.

6 MSCI, Giese, Guido and Lee, Linda-Eling and Dimitris, Melas and Nagy, Zoltan and Nishikawa, Laura, Foundations of ESG Investing, Part 2: Integrating ESG into Benchmarks (May 2018).

7 Press Release, Swiss Re Among First in the Reinsurance Industry to Integrate ESG benchmarks into its Investment Decisions (July 6, 2017).

8 MSCI, Giese, Guido and Lee, Linda-Eling and Dimitris, Melas and Nagy, Zoltan and Nishikawa, Laura, Foundations of ESG Investing, Part 2: Integrating ESG into Benchmarks (May 2018).