Investing Evolved: HALO

HALO stands for Heavy Assets, Low Obsolescence: These are companies that have cash flows tied to essential real-world demand supported by long-lived infrastructure, regulated frameworks, and long-term contracts.

We think that if you apply a HALO screen to Australian equities, it points to an existing approach many savvy investors are already using.

A recurring joke in the sitcom Modern Family was Phil Dunphy's creative ways of starting a phone conversation. He’d ask a question, which he would then answer as he picked up the phone. The answer is usually a pun on hello.

What's the most dangerous type of uranium cake? Yellow!

Nature's sure-fire sunburn remedy? Aloe

And of course, our favourite, what's the best first-person shooter about genetically modified space marines? Halo!

We think that the last one would be updated in today’s investing environment, if Phil Dunphy were a fund manager, not a realtor, a gag in the show right now would be, “How should you assess Australian equities right now?” Halo!

What is HALO in investing?

In investing, HALO stands for Heavy Assets, Low Obsolescence. These are companies that have cash flows tied to essential real-world demand supported by long-lived infrastructure, regulated frameworks, and long-term contracts.

Josh Brown of Ritholtz Wealth Management first referenced HALO in February 2026. Institutional desks quickly adopted the concept at Goldman Sachs and Morgan Stanley as a lens for identifying businesses that are not only resilient to AI disruption but may become more profitable because of it.

Applied to the Australian market, the HALO universe spans mining, energy, infrastructure, utilities, transport, telecommunications, staples and logistics. The S&P/ASX 200's exposure to these names is heavily concentrated in a small number of mega-cap miners.

Therefore, we think, the problem for many investors is that they are not getting enough meaningful exposure to all the HALO companies via funds that track or are benchmarked to the S&P/ASX 200. An equal-weighted approach could reduce concentration and provide more meaningful exposure to these HALO companies. The VanEck Australian Equal Weight ETF (MVW) utilises an equal weight approach and is used in the analysis below.

The HALO Framework

HALO companies share a common characteristic: their competitive advantages are rooted in physical assets that are difficult, expensive or impossible to replicate. These include pipelines, toll roads, rail networks, power stations, mine sites, ports, fibre networks and distribution centres. The assets are essential to the functioning of the economy, supported by long-duration contracts or regulatory frameworks. They generate cash flows that are relatively insulated from technological disruption.

The framework distinguishes "atoms" and "bits". Companies in the "bits" economy (software, digital platforms, media) are structurally exposed to disruption from AI and automation. Companies in the "atoms" economy (physical infrastructure, energy production, logistics) are not only less exposed to that disruption, they may also benefit from it, as AI adoption increases demand for energy, data centre infrastructure, and the physical supply chains that support them.

In the Australian market, HALO candidates span four broad categories: mining and resources (BHP, Rio Tinto), energy producers (Woodside, Santos, Origin), regulated infrastructure and utilities (APA, Transurban, AGL, Aurizon) and essential services and logistics (Telstra, Coles, Qube Holdings).

MVW and the HALO universe

The S&P/ASX 200 holds a combined 22.4% in the 12 core ASX HALO names. MVW holds 17.3%. At the headline level, that would suggest the cap-weighted index has greater HALO exposure. However, the composition of that exposure tells a different story.

BHP alone accounts for 9.9% of the S&P/ASX 200. Add Rio Tinto at 2.2%, and two mega-cap miners represent 12.1% of the benchmark's total HALO allocation. These are commodity price-takers whose earnings are driven by the iron ore spot price and Chinese steel demand. They meet the "heavy assets" criterion, but their earnings are cyclical in a way that pipelines, toll roads and power stations are not.

Strip out BHP and Rio Tinto, and the picture reverses. MVW holds 14.3% in diversified HALO (the infrastructure, energy, utilities, telco, staples, and logistics names that represent the core of the thesis) versus the S&P/ASX 200's 10.3%. That is a 1.4x overweight to the HALO names with contracted revenues, regulated cash flows, and essential demand characteristics.

The individual stock multiples illustrate the point.

Source: FactSet, as at 31 March 2026. MVW multiple is MVW portfolio weight divided by S&P/ASX 200 benchmark weight. Not a recommendation to act.

AGL Energy is held at 6.5 times its benchmark weight in MVW. Aurizon, the monopoly rail freight operator, is at 5.6 times. Qube Holdings, which controls critical port and logistics infrastructure, is at 4.2 times. APA Group, which operates 15,000 kilometres of gas pipeline, is at 3.0 times.

This is not a deliberate thematic tilt but rather a direct consequence of equal weighting. By equally weighting at each quarterly rebalancing, MVW increases exposure to smaller and mid-cap companies that are rounding errors in the market capitalisation weighted, S&P/ASX 200 Index.

March 2026: HALO in practice

March 2026, we think, supported diversification to the HALO investment thesis. Middle East tensions pushed Brent crude above US$116 per barrel. At the same time, the RBA signalled that interest rates would be higher for longer.

Over March 2026, the S&P/ASX 200 fell 7.15%, while MVW only fell 5.47%, representing an outperformance of 1.68%.

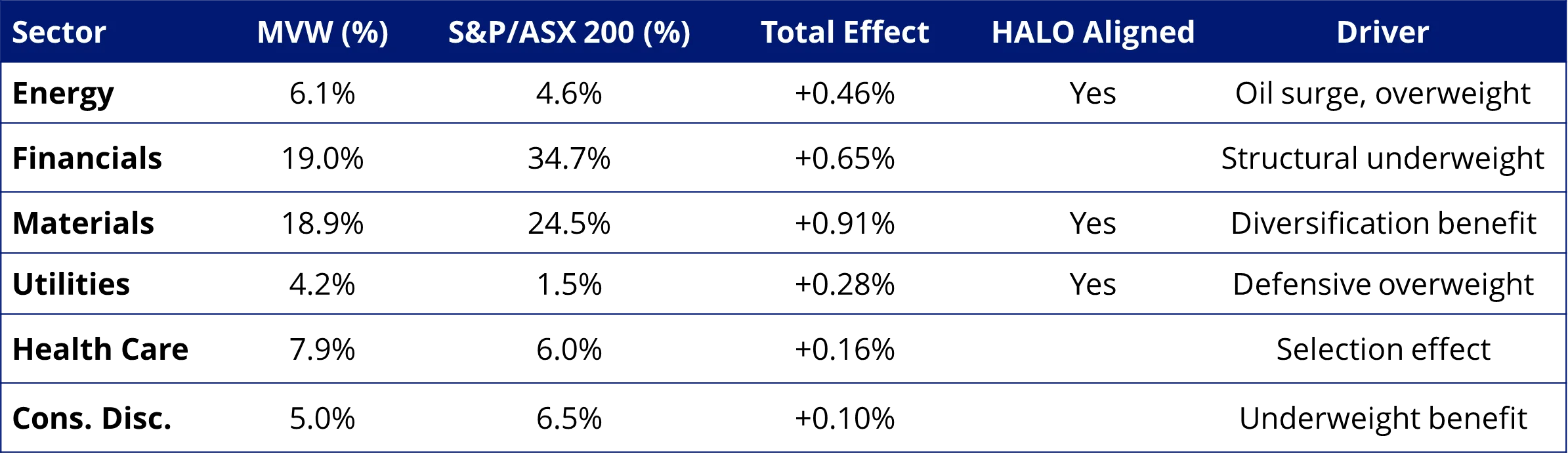

The sectors closely aligned with the HALO framework were among the strongest contributors to MVW's relative performance.

Source: FactSet, 27 February 2026 to 31 March 2026. Not a recommendation to act. Past performance is not indicative of current or future performance.

Energy, Materials and Utilities, the three sectors most directly aligned with the HALO framework, contributed a combined +1.65% of MVW's total +1.68% relative return. The equal weight structure amplified the benefit of smaller HALO names like APA Group (+8.15%), Santos (+17.75%), and Coles (+8.95%), and these companies had a proportionally larger impact in MVW than they did in the cap-weighted benchmark because MVW had a more meaningful exposure to them.

How should you assess Australian equities right now? Halo!

The macro environment that supported MVW’s outperformance in March 2026 has not resolved. Oil prices remain elevated on geopolitical risk, the RBA has signalled rates will stay higher for longer and household budgets are under pressure.

In this environment, companies with contracted, inflation-linked revenues and essential demand characteristics are better positioned to protect margins than those exposed to discretionary spending, credit cycles, or technological disruption, we think.

The S&P/ASX 200’s top-10 concentration currently sits around 49% and has been rising as investors crowd into banks and mega-cap miners. VanEck's research on the relationship between the S&P/ASX 200 concentration and subsequent equal weight performance shows that when concentration has been above the median level, the MVIS Australia Equal Weight Index has outperformed the S&P/ASX 200 over the subsequent five years in 100% of observations, with an average outperformance of +15.5%.

Equal weighting does not require a view on which specific HALO names will outperform. It provides diversified, proportional exposure to the full set of them, including the mid-cap infrastructure, energy, and utilities businesses that the cap-weighted index and many quality-screened alternatives structurally underweight.

For Modern Family fans, even Jay got in on the joke, proclaiming in Season 5 that he’d wanted to do this:

“Quick, what's the ring around an angel's head?”

An investment in our Australian equal weight ETF carries risks associated with: financial markets generally, individual company management, industry sectors, fund operations and tracking an index. See the VanEck Australian Equal Weight ETF PDS and TMD for more details.

MVW is likely to be appropriate for a consumer who is seeking capital growth and a regular income distribution, is intending to use the product as a core, minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

Published: 10 April 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.