The distortion in Australian equities

A regulatory safeguard designed to protect superannuation members may now be distorting Australia’s equity market.

The structure of the Australian equity market is unique in the world; we’re all aware it is concentrated, but a regulatory change is causing an unintended distortion.

In a recent AFR piece, it was argued that the Your Future, Your Super regime is providing an impediment for investors to allocate capital as they naturally would.

This risk for large institutions underperforming is too big, so rather than underperform, they tend to track the market, or invest in those companies that influence the direction of the market, for example the mega caps.This results in fundamentals not driving Australian share market returns; rather the focus on stocks that influence the benchmark is what we are seeing driving the share market.

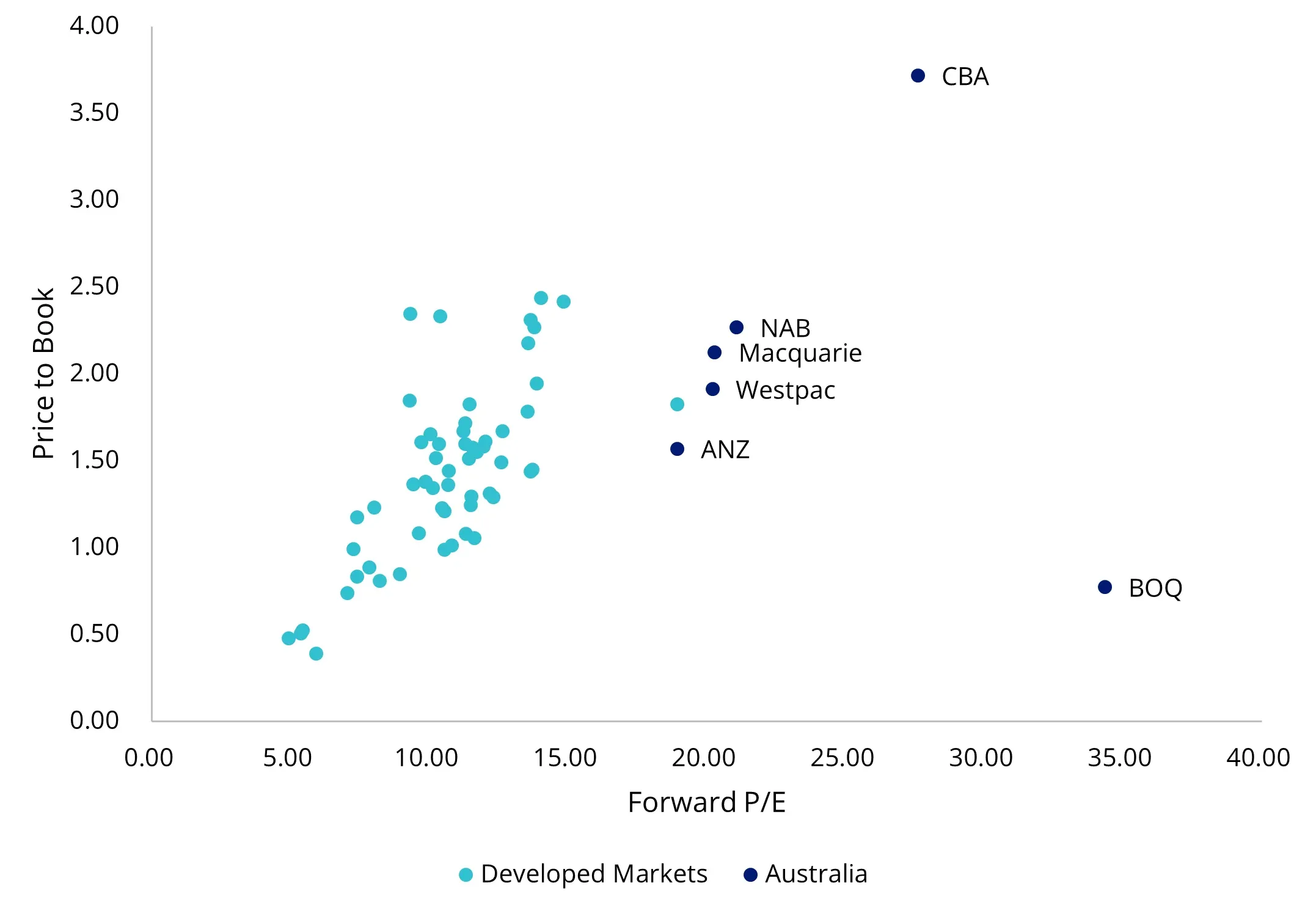

We’ve seen this in action - Australian banks remain among the most expensive in the world, despite very few analysts having these as a buy.

While sector bias makes sense if you are bullish on the sector, given the well-noted pressures on banks, with margins under pressure and an economic outlook not conducive to growth, we believe a less concentrated approach to Australian equities may be prudent. Overall, we think that diversification, rather than concentration, is the approach.

Take advantage of Your Future, Your Super distorting Australian equities

Last week, the AFR’s Jonathan Shapiro wrote about the (unintended) consequences of Your Future, Your Super for the market and investors, including superannuation members. The article cites three concerns:

- Time horizon tensions – The major problems here are that super funds themselves are growing increasingly uncomfortable with the severe constraints placed upon them to truly invest for the long term. Mid and small caps with significant growth potential over a long period are being overlooked (and thus missed).

- The risks of risk aversion – “Benchmarking is dulling the wisdom of the Australian share market crowd to properly value its constituents because too much capital is passive and focused on stocks that influence the benchmark.” The article cites the 2025 price rise of CBA to prices that few could justify. Rather than trade opportunistically, Your Future, Your Super is impeding investors' ability to allocate capital as they naturally would.

- Governance and incentives – A lack of ‘active management’ involvement could lead to less pressure on boards, who sleepwalk on higher prices, but at the cost of efficiency and the potential of better gains.

The article points out something we have said before: “benchmarks were always intended to measure and evaluate how well capital has been allocated, not to drive the capital allocation process itself.”

The irony of Your Future, Your Super distorting the market is that it is creating a risk: concentration risk.

We think that this concentration is an opportunity for long-term investors, not wedded to your future, your super benchmarks. While the YFYS benchmarking has turned industry super funds into the world's most expensive index trackers, herding billions into the same names or arguably the same name. That herding creates dislocations, and dislocations create a short book. When everyone is forced to own the same thing, the things they are forced to ignore get mispriced.

The most concentrated share market in the world

The Australian share market is dominated by five banks and two miners. The ASX 200 is one of the most concentrated developed-market indices on the planet.

Exhibit 1: The top 5 securities account for 32.73% of the S&P/ASX 200 Index

Source: FactSet, 31 January 2026

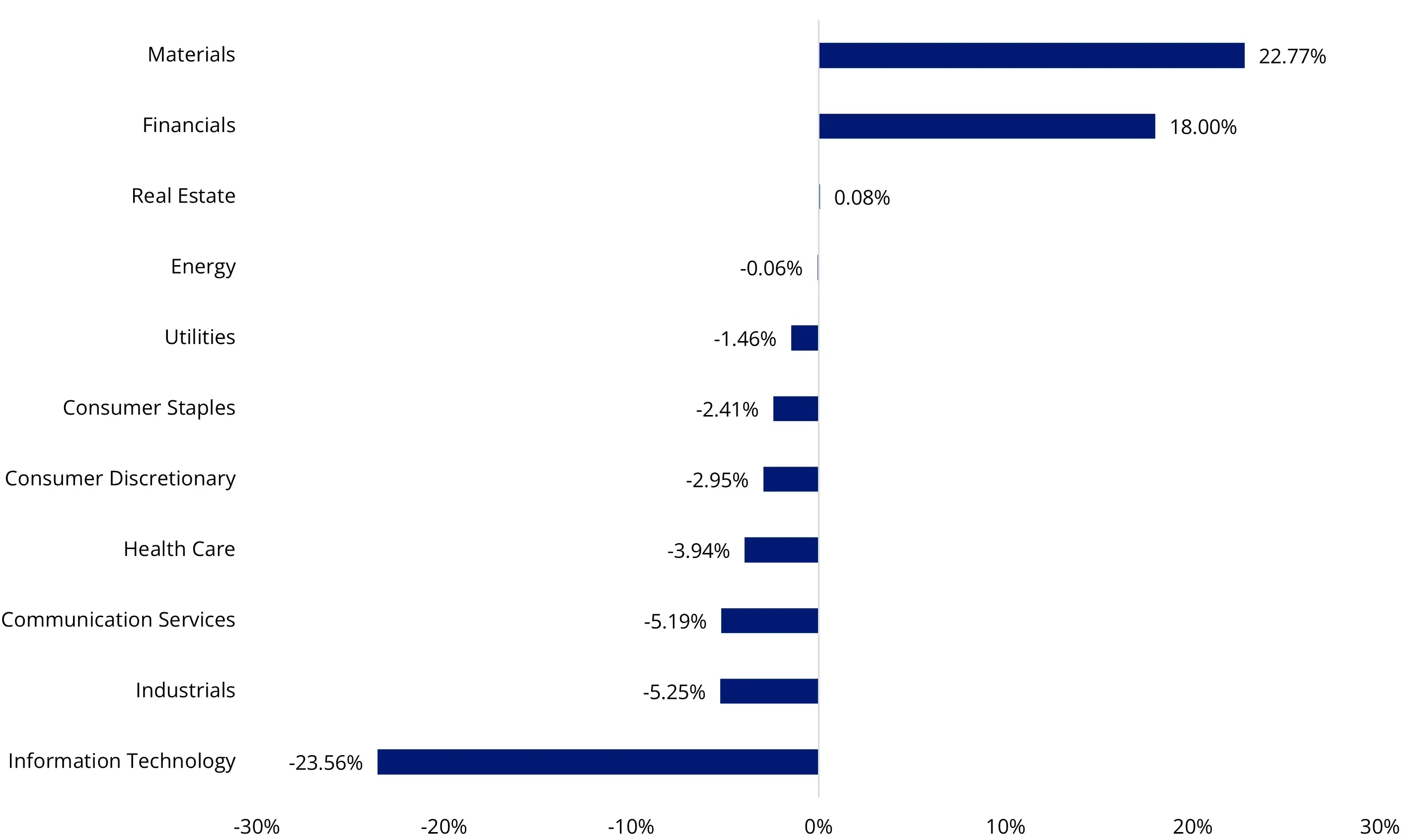

The Australian share market is structurally overweight materials and financials, and structurally underweight technology and global growth.

Exhibit 2: S&P/ASX 200 sector exposure relative MSCI World ex Australia Index

Source: FactSet, 28 February 2026. Difference calculated by subtracting MSCI World ex Australia GICS sector weights from S&P/ASX 200 GICS sector weights. Positive differentials imply greater exposure in Australian equities.

We think that this concentration is an opportunity for long-term investors, not wedded to Your Future, Your Super benchmarks.

If you own the index, you own the concentration. We’re not saying, don’t own the banks, we're saying, it’s worth pondering if it warrants such a large allocation.

Exhibit 3: Global bank valuations

Exhibit 4: Average big 4, price to earnings

Exhibit 3 source: Bloomberg, VanEck as at 5 March 2026 and Exhibit 4 source: Bloomberg, VanEck 24 February 2026.

A solution for managing concentration risk with alternative weighting

MVW has less exposure to the mega-caps that dominate the S&P/ASX 200 Index compared to many Australian equity portfolios. MVW is underweight mega cap companies and overweight those large companies outside the mega-caps. You can see below, relative to the S&P/ASX 200, MVW has a higher weighting to stocks outside the top 15.

Exhibit 5: S&P/ASX 200 and MVW company weightings (%)

Source: FactSet, 31 January 2026

Many advisers and their investors are already using MVW as their core Australian equity allocation, around which they can add high-conviction satellite ideas.

Using MVW in a portfolio

Since it launched on ASX in 2014, MVW has become the fourth-largest broad-based Australian equities ETF. It is the largest smart beta ETF in its category and has enjoyed support from all parts of the market. These investors have been using MVW to replace or sit alongside their:

- Australian equity unlisted active fund, which charges higher fees,

- LICs that are trading at discounts, or

- ASX/200 trackers to reduce stock and sector concentration risks.

MVW has demonstrated resilience across market cycles, consistently avoiding concentration risk inherent in traditional market cap indices, particularly in the context of Australia’s heavily top-weighted financials and resources sectors. For investors focused on long-term stability and enhanced diversification, MVW’s equal-weighted approach offers a compelling alternative for core Australian equities. It is philosophically sound and empirically robust.

MVW’s management fee of just 35 basis points per annum makes it one of the lowest-cost investment funds in its peer group, including unlisted managed active funds. In a landscape where cost, transparency, and value are under the microscope, it’s worth taking a closer look at what’s really being paid for, and whether headline fee signals are telling the full story. MVW does not charge any performance fees.

In addition to MVW, another way to take advantage of the current market dynamics is with the VanEck Geared Australian Equal Weight Complex ETF (GMVW).

Using ALFA as a high conviction satellite.

ALFA is an unconstrained high conviction Australian equity portfolio that targets long and short positions. It uses a dynamic quantitative stock selection approach utilising sophisticated computations and programmed learning designed to be agnostic of market cycles and style rotations.

January marked the first anniversary of ALFA. We sent a note highlighting its outperformance of the S&P/ASX 200 and the drivers of this performance (please reply to this email if you would like that email resent to you.) We noted its performance “outcomes reflect the strategy’s ability to generate excess returns through a combination of its high-conviction long and short positioning and its systematic, style-agnostic investment process.”

Notably, ALFA’s management fee is approximately one-third of that charged by many comparable Australian equity long/short strategies. In a market where genuine long/short capability often comes at hedge fund-level pricing, ALFA offers access to this expanded toolkit at a lower cost.

In a way, equal weighting and long-short are complementary expressions of the same insight: the ASX is systematically distorted by concentration and institutional herding. MVW corrects the concentration passively. ALFA monetises the herding actively, running a long book of quality businesses that the market underweights and a short book of the crowded names that Your Future, Your Super forces institutional capital to accumulate.

To receive a copy of research reports or for more information on MVW, GMVW or ALFA, please contact me or visit our website here. And please do not hesitate to reach out for a customised portfolio solution. I am happy to show how MVW could be included as a low-cost core portfolio to replace/complement an active manager and/or S&P/ASX index tracker, or how ALFA could be used as a satellite position.

For portfolio management execution, please contact our Capital Markets desk on 02 8038 3317.

Key risks

An investment in the ETFs carries risks. These include risks associated with financial markets generally, individual company management, industry sectors, fund operations and tracking an index. GMVW borrows money to increase the amount it can invest. While this can result in larger gains in a rising market, it can also magnify losses in a falling market. The greater the level of gearing in the Fund, the greater the potential loss of capital. The Fund is considered to have a higher investment risk than a comparable fund that is ungeared. ALFA is considered to have a higher investment risk than a comparable fund that does not engage in short selling and leverage. Investors should actively monitor their investment as frequently as daily to ensure it continues to meet their investment objectives. Risks associated with an investment in ALFA include those associated with short-selling risk, leverage risk, prime broker risk, counterparties risk, concentration risk, operational risk and material portfolio information risk. See the relevant PDS and TMD for details.

Published: 05 March 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.

MVW is likely to be appropriate for a consumer who is seeking capital growth and a regular income distribution, is intending to use the product as a core, minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

GMVW is likely to be appropriate for a consumer who is seeking capital growth and a regular income distribution, is intending to use the product as a core, minor or satellite allocation within a portfolio, has an investment timeframe of at least 7 years, and has an extremely high risk/return profile.

ALFA is likely to be appropriate for a consumer who is seeking capital growth, is intending to use the product as a minor or satellite allocation within a portfolio, has an investment timeframe of at least 7 years, and has a very high risk/return profile.