The AI trade is back and China is in the frame

China’s AI opportunity may be hiding in plain sight, in the underappreciated companies building the infrastructure, devices and applications.

As we have written about previously, China's AI ecosystem is developing rapidly. DeepSeek, the Hangzhou-based lab whose open-source AI model rivalled OpenAI's ChatGPT, is now in discussions to raise capital at a valuation of more than US$20 billion. While significant, this figure represents a fraction of OpenAI's current US$852 billion or Anthropic's US$1 trillion valuation (as of April 2026). Alibaba has set a target of increasing annual cloud and AI revenue fivefold to US$100 billion within five years, while Tencent has unveiled a major upgrade to its foundational open-source AI model. Together, the developments suggest China’s AI champions are moving rapidly toward large scale commercial competition.

Beyond the mega-caps: why mid-cap AI exposure matters

When investors think about China's AI story, mega caps including Alibaba and Tencent tend to come to mind first. While these are important companies, they represent only one part of a much deeper ecosystem.

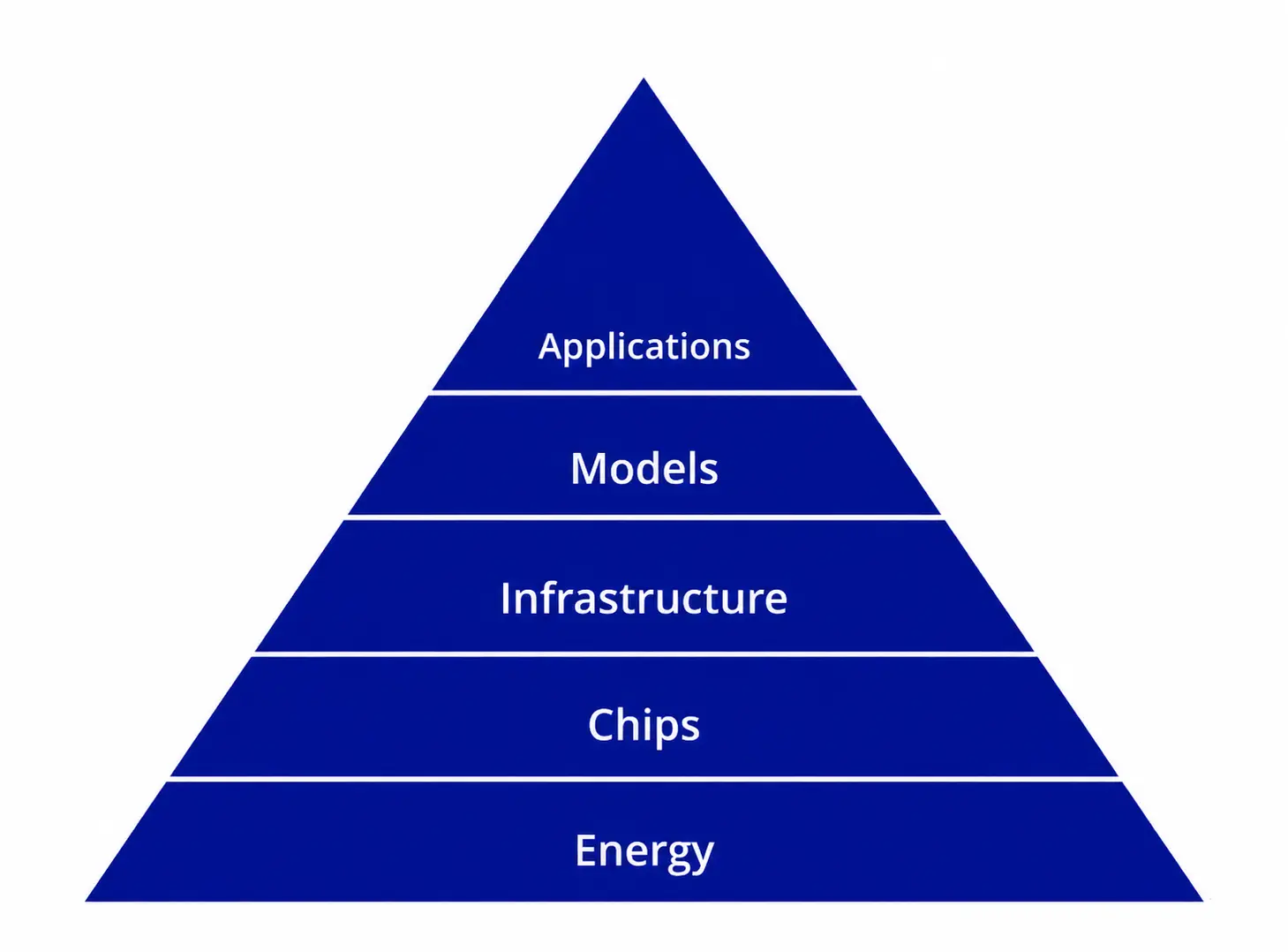

Nvidia CEO Jensen Huang once described the AI ecosystem as a “five-layer cake”, with applications at the top. More important, however, are the companies that form the physical backbone of the AI infrastructure build out. These are the manufacturers of optical transceivers that connect AI server clusters, the producers of high-density printed circuit boards (PCBs) and semiconductor materials that underpin chip fabrication, as well as the makers of Internet of Things (IoT) devices that bring AI capabilities into the physical world.

As AI moves from model training to real-world deployment and inference at the edge, the companies in this mid-cap segment become increasingly important. They also tend to be less exposed to the US-China tech war. Many derive most of their revenue domestically and sit at critical pinch points in supply chains that are difficult to replicate.

Source: Nvidia. Illustrative purposes only.

Understanding this layered structure, from model developers to infrastructure enablers to end-user integrators, is key to forming a complete view of where AI value is being created in China today.

A window into China's AI value chain

We categorise stocks listed on China’s A-share market according to their exposure to AI: Direct AI, AI-adjacent and AI-enabled. Together, they illustrate the breadth of opportunities emerging beyond the market’s better-known AI names.

Direct AI – Companies whose core business is artificial intelligence. These pure-play AI names currently trade at a fraction of comparable US AI software names.

|

Company |

Subsector |

AI Rationale |

Forward P/E |

|

Nanjing Sciyon Wisdom Technology Group |

Systems Software |

A developer of smart city AI platforms |

19.97 |

|

Rockchip Electronics |

Semiconductors |

A designer of AI system-on-chip (SoC) processors for edge devices and IoT |

53.61 |

|

Intsig Information |

Application Software |

The maker of CamScanner whose AI-powered optical character recognition technology is used by hundreds of millions globally |

46.50 |

|

Actions Technology |

Semiconductors |

A developer of AI SoC chips for wearables and IoT |

28.79 |

|

Beijing Hyperstrong Technology |

Heavy Electrical Equipment |

The maker of AI-powered battery energy storage systems |

23.79 |

Source: VanEck, FactSet. Actions Technology forward P/E estimate provided by Bloomberg. As at 14 May 2026. Not a recommendation to act.

AI-Adjacent – "picks and shovels" companies building the physical infrastructure that the AI revolution runs on.

|

Company |

Subsector |

AI Rationale |

Forward P/E |

|

Delton Technology Guangzhou |

Electronic Components |

A manufacturer of electronic components for connectivity |

42.25 |

|

Suzhou Hengmingda Electronic Technology |

Electronic Manufacturing Services |

An electronic manufacturing service provider for semiconductor equipment |

27.27 |

|

Shennan Circuits |

Electronic Components |

A top-tier producer of high-density PCBs and integrated circuit substrates used in AI servers. |

42.00 |

|

Suzhou Tfc Optical Communication |

Communications Equipment |

A manufacturer of optical communication components for data centres |

63.91 |

|

Zhongji Innolight |

Communications Equipment |

One of the world's leading optical transceiver manufacturers and a key supplier to Nvidia's AI data centre ecosystem (800G and 1.6T modules). |

33.17 |

Source: VanEck, Factset. As at 14 May 2026. Not a recommendation to act.

AI-Enabled – companies that are integrating AI into existing consumer-facing products and services. Several of these consumer-linked AI plays trade at single-digit or low-teens forward P/E ratios – a valuation that is arguably undemanding for AI exposure.

|

Company |

Subsector |

AI Rationale |

Forward P/E |

|

Hithink Royalflush Information Network |

Financial Exchanges & Data |

An AI-driven fintech platform (financial data analytics, robo-advisory) |

40.91 |

|

Hisense Visual Technology |

Consumer Electronics |

AI-powered smart TVs and display technology |

12.01 |

|

G-Bits Network Technology Xiamen |

Interactive Home Entertainment |

AI in online gaming |

15.18 |

|

Guangdong TCL Smart Home Appliances |

Household Appliances |

AI-enabled smart home appliances |

8.59 |

|

Shenzhen Crastal Technology |

Household Appliances |

Smart home/IoT appliances |

24.91 |

Source: VanEck, FactSet. As at 14 May 2026. Not a recommendation to act.

The valuation gap: AI exposure without the premium

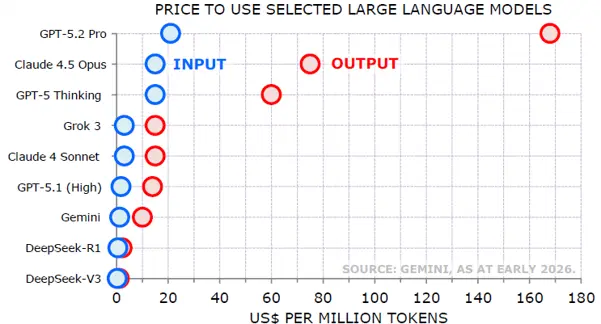

One of the most notable features of China's AI-linked companies is the valuation disconnect with their US counterparts. In the US, AI beneficiaries command eye-watering multiples, with many software companies trading at well above 100x like Palantir (107.9x) and Cloudfare (184.5x) at the time of writing. In contrast, critical AI supply chain companies listed in China are available at 20–35x forward earnings while consumer companies integrating AI into their products trade for as little as 8–15x, according to Bloomberg consensus estimates.

Several factors help explain this gap. China's AI ecosystem is at an earlier stage of commercialisation, meaning markets are still pricing in execution risk. However, structural tailwinds are building. AI was a centrepiece of China's 2025 National People's Congress, signalling sustained policy support. Crucially, China's open-source model ecosystem is dramatically lowering adoption costs. For instance, DeepSeek's models are open-source and largely free - posing an economic challenge to US firms that have kept their systems proprietary and will now have to justify hundreds of billions of dollars in infrastructure spending.

Source: Gemini, 2026.

There are several ways for investors to gain exposure to China’s growing AI opportunity:

- The VanEck China New Economy ETF (CNEW) invests in 120 fundamentally sound and attractively valued companies with growth prospects in China's New Economy, targeting technology, healthcare, and consumer staples and consumer discretionary sectors. More than 20% of CNEW’s exposure is toward companies that work in either technology hardware or semiconductor production.

- The VanEck FTSE China A50 ETF (CETF) invests in a diversified portfolio comprising the 50 largest companies in the mainland (A-shares) Chinese market. More than 20% of CETF’s exposure is toward technology companies such as Zhongji Innolight.

Key risks:

An investment in the ETF carries risks associated with: ASX trading time differences, China, financial markets generally, individual company management, industry sectors, foreign currency, sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the PDS and TMD for more details.

CNEW and CETF are likely to be appropriate for a consumer who is seeking capital growth, is intending to use the product as a minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a very high risk/return profile.

Published: 19 May 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.