Dollar weakness helps gold to all-time highs

Gold passes two important sign-posts

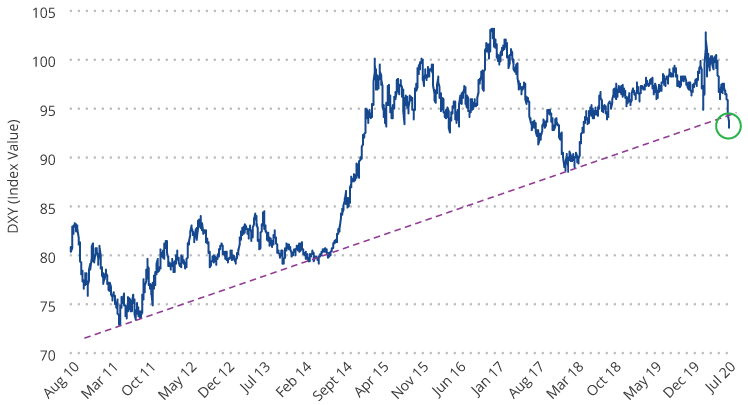

The gold bull market passed two important sign-posts in July. The strength of the market is impressive as it blew through US$1,800 and the all-time high of US$1,921. These prices had been major technical resistance points set a decade ago.The second significant signpost was the new US dollar weakness. The dollar's weakness is a hallmark of most gold bull markets, but in this cycle gold had so far been rising in a flat dollar environment. The chart below shows the US dollar index (DXY) has been in a bull market since 2011. However, the dollar declined through July, then fell precipitously at the end of the month, appearing to have broken its long-term trend. We may be seeing the beginnings of a bear market for the dollar. This enabled gold to test the US$2,000 per ounce milestone as it reached an intraday high of US$1,983 on July 31. Gold closed out July at US$1,975.86 per ounce for a US$194.90 (10.9%) monthly gain.

US dollar index breaking its near 10-year support trend (2011 to 2020)?

Source: VanEck, Bloomberg. Data as of July 31, 2020. Past performance is not a guarantee of future results.

Gold miners remain well positioned

Gold stocks moved higher as the vast majority of companies reporting second quarter results met or exceeded expectations. COVID-related costs were also reported, showing the industry has done an excellent job of dealing with operational issues in our view. For example, 1.7 million ounce producer Agnico-Eagle was among those hardest hit by pandemic lock downs. Its costs for temporary mine suspensions totaled US$22 million, whereas the cash provided from operations totaled US$162 million. Based on the company’s second quarter 2020 financial results, Agnico-Eagle expects COVID protocols to cost US$6 per ounce, which raises their cash costs by less than 1%. For the month, the NYSE Gold Miners Index gained 13.0%.

$2,000 gold is about more than just the pandemic

Gold tested the US$2,000 per ounce level sooner than we had anticipated and we believe there is more than the pandemic to overcome at this point.

- Slower Recovery – In July, two Federal Reserve (Fed) presidents, a Fed governor, and its Chairman all warned of a long, slow road to economic recovery. Initial jobless claims have stagnated for eight weeks at around 1.4 to 1.5 million. Contrast this with the GFC (global financial crisis), where initial jobless claims declined steadily to 587,000 in the same time frame, 17 weeks after the recession peak. JPMorgan said it was preparing for an unemployment rate that remains in double digits well into the next year and a slower recovery in gross domestic product (GDP) than the bank’s economists assumed three months ago.

- Deficits, Debt & Defaults – The US budget deficit totaled US$863 billion in June, as much as the entire gap in 2019. With the new stimulus bill now being considered in Congress, the annual deficit could exceed US$4.7 trillion. This is on top of record peace-time deficits before the pandemic.

Corporate debt is also at record levels and many households are feeling financial stress. Ultra low interest rates over the past two decades have encouraged the accumulation of unproductive government and private debt. It fuels the rise of giant firms, while “zombie” companies (companies with earnings less than their debt service costs) have proliferated. This is at the expense of start-ups, innovation and creative destruction. The result is low levels of productivity, causing recoveries to become weaker and weaker. The Wall Street Journal reports the largest US banks have set aside US$28 billion to cover losses as consumers and businesses start to default on their loans.

What could drive gold prices even higher?

The pandemic created a deflationary shock to the economy and the massive accumulation of debt since the GFC creates a drag on productivity that could guarantee a low growth economy for decades to come. Negative real rates, persistent risks to economic well-being, and the weak dollar are drivers that we believe could push gold to trend to US$3,400 per ounce in the coming years. This might be a conservative forecast considering the 180% rise gold experienced from the depths of the GFC (see our gold price projection here). Several scenarios could see gold prices moving higher from there:

- Systemic collapse as debt issuance overwhelms the financial markets.

- An inflationary cycle brought on by either: a) trillions of US dollars, euros, yen and yuan being pumped into the global financial system, b) governments enabling inflation to ease the debt burden, c) implementation of modern monetary theory or other forms of money printing to fund government spending without issuing debt.

- US dollar crisis – America is dealing with deficits, divisive politics, social unrest and deteriorating international relations on a scale rarely seen in history. While other countries may have similar problems, they do not oversee the world’s reserve currency. The US is held to a higher standard and a crisis of confidence could weigh heavily on the dollar.

Some might balk at such bold forecasts. However, we believe the various drivers of gold are rarely aligned as they are today. We also consider gold’s relative size in the financial markets. There have been 200,000 tonnes of gold mined in the history of the world and virtually all of it is potentially available to the market. A gold price of US$2,000 per ounce yields a market value of US$12.9 trillion. Compare this with global stock, bond and currency markets, each of which totals roughly US$100 trillion or more. A relatively small shift in funds from these markets may fuel the gold price for a long time.

In addition, the market value of the global gold industry as of end-July is approximately US$530 billion. The market value of Alphabet Inc. as of the same time, alone, is US$1 trillion. Gold mining is a relatively tiny sector that, in addition to carrying earnings leverage to the gold price, carries a scarcity factor when market demand is high.

Published: 06 August 2020

IMPORTANT DISCLOSURES

Issued by VanEck Investments Limited ABN 22 146 596 116 AFSL 416755 (‘VanEck’) as the responsible entity and issuer of units in the VanEck Vectors ETFs traded on ASX. This is general information only about financial products and not personal financial advice. It does not take into account any person’s individual objectives, financial situation or needs. Before making an investment decision, you should read the relevant PDS and with the assistance of a financial adviser consider if it is appropriate for your circumstances. PDSs are available at www.vaneck.com.au or by calling 1300 68 38 37. All investments carry some level of risk. Investing in international markets has specific risks that are in addition to the typical risks associated with investing in the Australian market. These include currency/foreign exchange fluctuations, ASX trading time differences and changes in foreign regulatory and tax regulations. See the PDS for details.

No member of VanEck group of companies gives any guarantee or assurance as to the repayment of capital, the payment of income, the performance, or any particular rate of return of any VanEck funds. Past performance is not a reliable indicator of future performance.