Gold has surged 130% in 5 years - but its biggest customers are still buying

Gold doesn’t need an introduction.

Over the past five years, the yellow metal has outperformed a range of major asset classes, including REITs, bonds and even the S&P 500. Australian investors have done even better, with a weaker Australian dollar helping drive the local gold price to record highs.

Given that backdrop, you might expect demand to be cooling. Instead, gold's largest buyers appear to be doing the opposite.

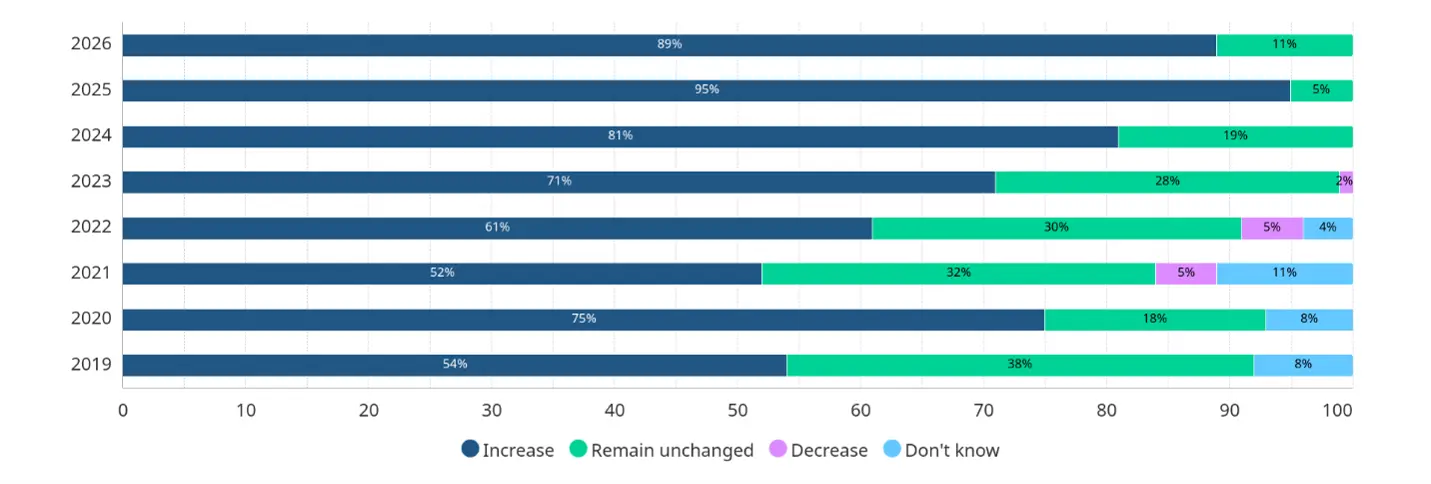

According to the latest World Gold Council survey, 89% of central bank/reserve manager respondents believe global central bank gold reserves will continue to grow.

Chart 1: 89% of respondents expect global official gold reserves to increase over the next year

So why are central banks still buying after one of the strongest runs in the metal's long history, and is there anything investors can glean from these moves?

Looking beyond the next market cycle

Central banks, like all investors, are fallible. They don't know where gold will trade next quarter any more than anyone else does. But while markets often focus on the next data print or headline, reserve managers are tasked with protecting national reserves over years and decades.

For institutions with that responsibility, gold offers something few reserve assets can: scarcity. Unlike a currency, it cannot simply be created by a policy decision. Unlike a company, it does not need earnings growth to justify its place in a portfolio. That scarcity helps explain why gold has remained a store of value through centuries of economic and political change.

The environment facing central banks today is very different to the one that existed a decade ago. Inflation has returned, geopolitical tensions have intensified and resilience has become a growing priority for reserve managers. Against that backdrop, nearly three-quarters of respondents to the World Gold Council's latest survey expect the US dollar's share of global reserves to decline over the next five years.

Chart 2: 74% of respondents expect the dollar's share of global reserves to decline, with gold seen as the primary beneficiary of that reallocation

That doesn't mean the US dollar is about to lose its position as the world's dominant reserve currency. There is currently no obvious replacement waiting in the wings. But it does suggest that reserve managers like central banks are becoming increasingly conscious of concentration risk within their reserve portfolios.

Gold also brings something else to the table. Unlike shares, which ultimately rely on corporate earnings, or bonds, which are heavily influenced by interest rates, gold tends to be driven by a different set of factors. As a result, it has historically behaved differently to traditional assets at various points in the market cycle, helping explain its enduring role as a portfolio diversifier.

Finally, gold is not controlled by a single country. That independence matters at a time when many developed economies are carrying historically high levels of public debt.

The technical picture

Central banks are not the only signal worth watching. The chart below tracks money flowing into and out of gold ETFs. What’s interesting is that some of the largest periods of investor selling over the past decade have occurred close to important turning points for the gold price. The latest reading suggests we may be witnessing another such episode.

Chart 3: The technical stars may be aligning for gold

Direct exposure to gold

For investors seeking exposure to the precious metal, physical gold remains the most direct option. The VanEck Gold Bullion ETF (ASX: NUGG) provides exposure to physical gold bullion while removing many of the practical challenges associated with buying, storing and insuring bullion directly. Investors also have the option of converting their holdings into physical gold through NUGG's redemption facility, all for a management fee of 0.25% p.a. Since its inception in December 2022, NUGG has delivered a 28.21% p.a. return to investors (as at 31 May 2026).

Can miners capitalise?

For investors, gold miners offer another way to access the gold theme. Unlike bullion, which depends entirely on the gold price, mining companies can potentially generate both income and capital growth.

Yet despite gold trading near record highs, many mining companies continue to trade below their long-term historical relationship with the gold price. The gap has narrowed as gold prices have risen and mining fundamentals have improved, but investors continue to assign a discount to the sector relative to bullion itself. Should miners continue delivering strong earnings and cash flow, investors may benefit from both sources of return.

Chart 4: The valuation discount between gold miners and gold bullion has narrowed in recent years

It should be said that the discount exists for good reasons. Mining companies are businesses and, as the table below shows, come with operational, geological and capital allocation risks. But with gold prices remaining near record highs and many producers generating strong cash flows, the persistent gap between bullion and miners remains one of the more interesting relationships in the gold market today.

Differences between gold miners and bullion

| Gold bullion | Gold miners | |

| Insurance costs | Gold must be insured, as it can be stolen. | None |

| Storage costs | Gold bullion should be vaulted in a safe location. | None |

| Correlation to currencies | High - The value of gold is priced in US dollars. This means monetary, fiscal, and, as we are finding out now, trading and defence policies contribute to the fluctuation in currencies and, therefore, the price of gold. | Low to medium, as gold miners can hedge their cash flows, thus mitigating the risks of currency movements. |

| Supply constrained / exploration | Mine output is dropping, and ore grades are getting lower and lower. | Some miners are mining existing deposits. Some also explore and they may find gold, or there may be no gold. It might also be uneconomical to mine the discovered deposit. This is a risk of owning miners. It is worth noting that the rate of finding new gold deposits has been falling, therefore supply of new gold is finite supporting the share price of miners currently mining high grade gold. |

| Artificial ownership risks | High – There is more ‘paper’ gold than physical gold and these artificial securities, owned by banks and hedge funds, can distort the price of physical gold. | Low |

| Income | No | Miners pay dividends to investors |

| Management risks | Not applicable | Like owning any publicly traded company, the quality of management is a risk of owning gold miners. |

| Correlation to equity markets | Low | Higher than bullion, especially during an equity market downturn. |

| Regulatory risks | No | Miners are subject to the rules and regulations of the country of the location of their mines and of the country they are listed in. |

| Geopolitical risks | The price of gold may rise if investors are uncertain about geopolitical issues affecting global markets. | The price of gold miners may rise if investors are uncertain, however, they may also fall, especially if the geopolitical risk directly affects the gold miner or its mines. |

This distinction also means bullion and miners can complement each other within the same portfolio, with one providing exposure to the metal itself and the other to the businesses extracting it. The VanEck Gold Miners ETF (ASX: GDX) provides exposure to global mining companies whose fortunes depend on both the gold price and their ability to convert favourable conditions into earnings and cash flow. It also gives Australian investors access to opportunities beyond the domestic gold sector. Over the past five years, GDX has delivered a total return of 21.56% p.a. (as at 31 May 2026).

|

VanEck Gold Bullion ETF (ASX: NUGG) |

VanEck Gold Miners ETF (ASX: GDX) |

|

|

A signal worth watching

Gold has already had a remarkable run, yet central banks continue to accumulate it. That doesn't tell us where the gold price will be next quarter, but it does suggest that some of the world's largest and longest-term investors still see an important role for gold in their reserve portfolios. Whether investors agree or not, it's a signal that's difficult to ignore.

Key risks

An investment in NUGG or GDX carries investment risk. These risks vary depending on the fund and may include gold pricing risk, currency risk, custody risk, Australian origin gold bullion risk, ASX trading time differences, financial markets generally, individual company management, industry sectors, country or sector concentration, political, regulatory and tax risks, fund operations and tracking an index. See the PDSs and TMDs for details on risks.

Published: 25 June 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.