Gold pullback: Why the long-term investment case remains intact

Key Takeaways:

- Gold's recent pullback reflects shifting macro conditions, while the long-term outlook for gold remains intact.

- Persistent inflation, geopolitical risks and lower real interest rates could continue to support gold prices.

- Gold stocks remain well positioned, supported by strong cash flow, healthy margins and attractive valuations.

A volatile start to 2026

Gold price volatility increased in the first half of 2026. Intraday, gold traded as high as US$5,595 on January 29. On June 30, it traded at its year-to-date low of US$3,943 but managed to close just above the US$4,000 mark – ending the month at US$4,008.02 per ounce. Gold declined 14.14% in the month of June and 7.21% year-to-date. Gold stocks lagged the precious metal, as expected during a period of declining bullion prices. The NYSE ARCA Gold Miners Index (AUD) fell 12.12% in June and is down 14.54% year to date.

Gold pulls back as markets shift toward risk assets

After reaching new all-time highs of nearly US$5,600 per ounce in early January, gold prices have come under pressure from a stronger US dollar and expectations for higher interest rates since the beginning of the war with Iran. The dominant macro narrative has become self-reinforcing: higher oil prices keep inflation expectations elevated, elevated inflation expectations keep the Federal Reserve on hold, a Fed on hold keeps real yields elevated and elevated real yields support the US dollar, which weighs on gold.

As a result, many commodity analysts have reduced their gold price outlooks for 2026. However, even after those downward revisions, Bloomberg data continues to reflect a generally constructive outlook for gold over the next several years. Analysts at Goldman Sachs, Citigroup and Deutsche Bank continue to expect further upside in gold – though we remind investors that forecasts are not intended as a prediction of future results nor is past performance a guarantee of future results.

At the end of June, the apparent end of the conflict in the Middle East further eroded gold’s safe haven appeal, as markets have shifted toward a risk-on environment and equity markets trade near recently established highs. Gold is now trading around US$4,000 per ounce, representing an approximately 25% pullback from its January highs. However, gold stocks remain the best-performing asset class over the past year, and gold continues to outperform most other major asset classes.

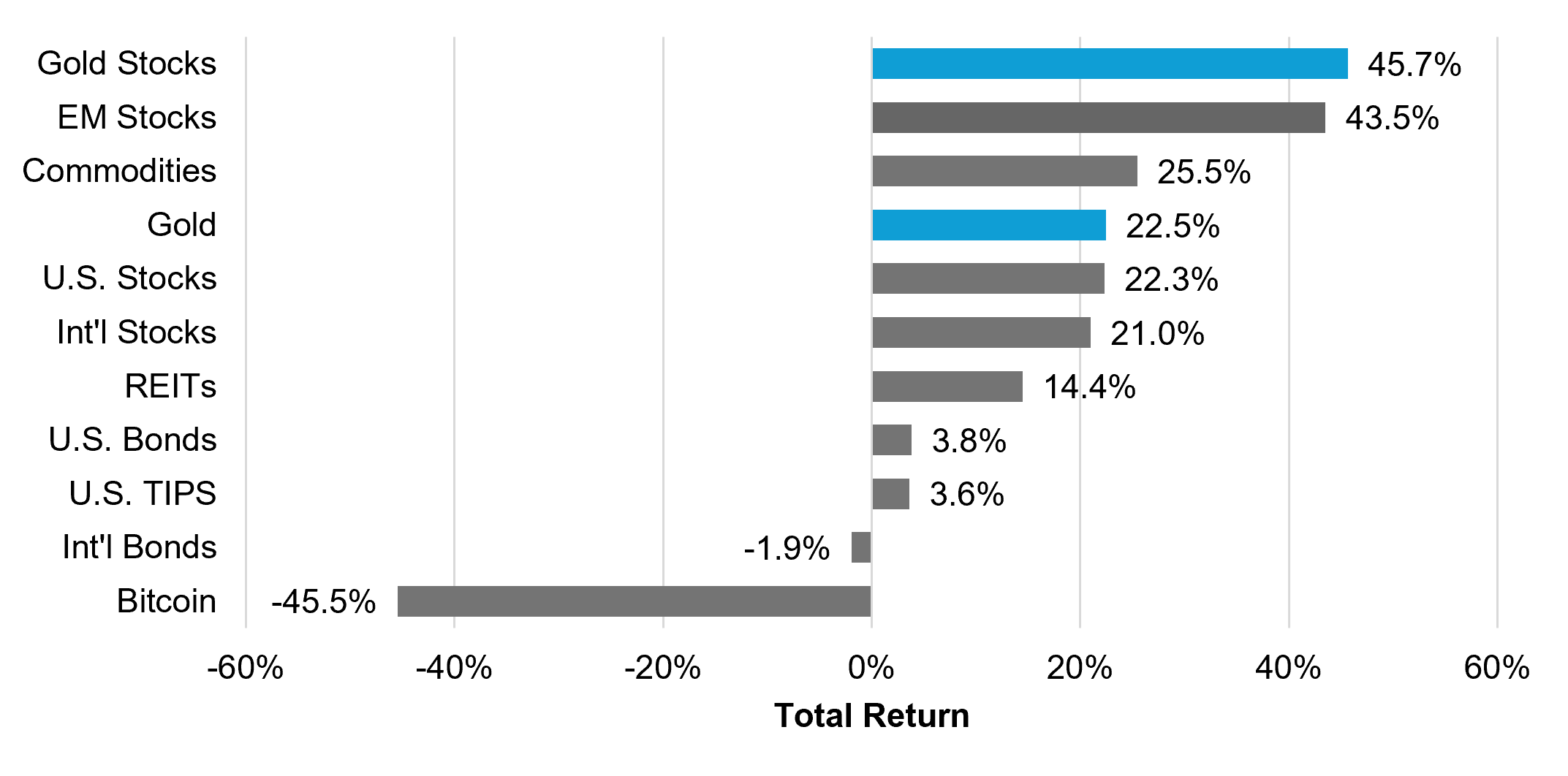

Chart 1: Gold assets continue to hold their ground

Source: Morningstar. Data as of June 2026. “Gold Stocks” represented by MV Global Gold Miners Index (MVGDXTR) (net of fees). "Gold" is represented by the LBMA Gold Price. “U.S. Stocks” represented by the S&P 500 Index. “EM Stocks” represented by MSCI Emerging Markets Index. “REITs” represented by FTSE NAREIT All Equity REITs Index. “International (Int’l) Stocks” represented by MSCI AC World ex USA Index. “Commodities” represented by Bloomberg Commodity Index. “U.S. TIPS” represented by Bloomberg U.S. TIPS (1-3 Year) Index. “U.S. Bonds” represented by Bloomberg U.S. Aggregate Bond Index. “International (Int’l) Bonds” represented by Bloomberg Global Aggregate ex US Index. "Bitcoin" represented by the price of bitcoin (BTC). Digital asset investments are subject to significant risk and may not be suitable for all investors. Past performance is not indicative of future results. Index performance is not representative of fund performance. It is not possible to directly invest in an index.

Looking beyond short-term volatility

Gold price volatility and the recent pullback may be weighing on investors. However, in our view, it is important to look past near-term noise. The continued strength in equity markets suggests a degree of optimism that could be tested. We believe investors may wish to reassess the risks associated with heightened geopolitical tensions, the prolonged effects of the Middle East conflict on the global economy and the outlook for inflation.

Why gold could continue to benefit

A prolonged environment where the Fed keeps rates on hold could contribute to lower (or even negative) real rates over time, a backdrop that has historically been among the most favourable for gold. In that scenario, gold has often played a prominent role as a diversifier and potential hedge for investors seeking portfolio protection and diversification. Gold stocks, in our view, may also be considered as part of a diversified allocation.

Even Fed hikes have not always been a negative for gold. According to World Gold Council data, which covered 44 Fed hikes from March 1997 through July 2023, gold delivered a positive surprise on rate hike days more than 50% of the time.

Central banks continue to support demand

Central bank gold statistics for May, also published by the World Gold Council, show that central banks remain committed to gold. Net monthly buying remains near record levels while 89% of central bankers surveyed expect global gold reserves to increase in the next 12 months.

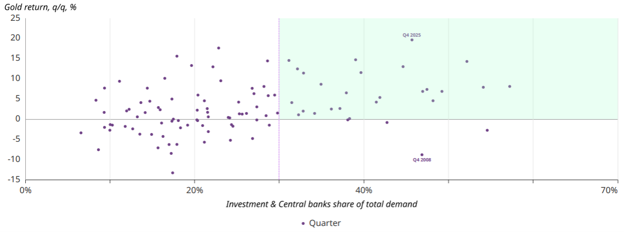

Strong, regionally diversified central bank buying and resilient investment demand from Asia continue to underpin gold demand at current levels. A return of Western investor participation, like what happened in 2025, could provide additional support and may contribute to further upside in the gold market. Gold has historically performed well during periods when central bank activity and investment together account for more than 30% of total demand.

Chart 2: There’s a strong link between gold returns and buying from investors and central banks

Source: World Gold Council. Data as of June 2026.

Why gold stocks may still offer opportunity

Gold stocks have historically outperformed the metal itself in rising gold price environments. However, investors may not need to wait for the next leg higher in gold to begin increasing exposure. At current prices, these companies are already generating record cash flow, as Q1 2026 earnings made abundantly clear. Gold has traded at an average price of approximately US$4,700 per ounce so far in 2026. With all-in sustaining costs for the sector estimated to average below US$2,000 per ounce in 2026, margins remain very strong even at US$4,000 gold. This gives companies the ability to finance growth, pay dividends and repurchase shares. Gold stocks continue to trade at valuations that remain low relative to historical levels, while the sector appears to be in strong financial and operational health by historical standards. Current equity prices appear to reflect more conservative assumptions than those implied by prevailing gold prices.

If investors rotate capital away from sectors with much richer valuations, particularly against a backdrop of rising pullback risk, gold stocks could be beneficiaries.

Published: 16 July 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.