Value five years on

When VLUE launched five years ago, value was out of favour after growth’s post-GFC dominance. Today it is among ASX’s top international equity ETFs. Why are investors flocking to VLUE?

During the eventful March 2026, the VanEck MSCI International Value ETF (VLUE) celebrated its fifth anniversary on ASX.

We launched VLUE as an expansion of our factor suite of ETFs, which at the time included our MSCI International Quality ETF (QUAL). Factor-based investing involves identifying the dynamics of an investment that drive its return. Factor-based ETFs, a subset of smart beta, combine the best aspects of active and passive management by tracking indices with defined rules designed to deliver a targeted investment outcome, while retaining transparency, liquidity, and ease of trading for investors.

VLUE is one such ETF, and since its inception on ASX in March 2021, it has outperformed, noting as always that past performance is not indicative of future performance.

Table 1: VLUE performance as at 31 March 2026

Source: VanEck, Morningstar, Bloomberg. Results assume immediate reinvestment of all dividends and include management fees but exclude brokerage costs and taxes. Past performance is not indicative of future performance.

VLUE inception date is 8 March 2021, and a copy of the factsheet is here.

The MSCI World ex Australia Index (“MSCI World ex Aus”) is shown for comparison purposes as it is the widely recognised benchmark used to measure the performance of developed market large- and mid-cap companies, weighted by market capitalisation. VLUE’s index measures the performance of 250 international large- and mid-cap companies selected from the MSCI World ex Australia Index with high value scores relative to their peers at rebalance. Exclusions apply for weapons and tobacco. Consequently, VLUE’s index has fewer companies and different country and industry allocations than MSCI World ex Aus. Click here for more details.

What sets VLUE apart.

VLUE tracks the MSCI World ex Australia Enhanced Value Top 250 Select Index (VLUE Index), which we think is the most representative expression of the value factor available on ASX.

VLUE does not include small caps, which have diluted the returns of some other value exposures, and with only 250 high-conviction holdings, it avoids the watered-down approach of broader value indices that hold hundreds of stocks with varying degrees of value characteristics.

Because it is rules-based, it does not drift from its style, nor is there the key-man risk associated with active funds.

Additionally, some ‘value’ companies are cheap for a reason, and these could be ‘value traps’. MSCI analysis found that using forward earnings can help protect against ‘value traps’. Additionally, MSCI found that considering whole-firm valuation measures, such as enterprise value, can reduce concentration in leveraged companies.

Therefore, MSCI developed its Enhanced Value Indices, which apply three valuation ratio descriptors on a sector-relative basis:

- price-to-book value - Ratio of the price to the company’s book value, or what is on the balance sheet. The lower the price to book, the cheaper the company.

- price-to-forward earnings - A version of the ratio of price-to-earnings (P/E) that uses forecasted earnings for the P/E calculation. The forward earnings are the weighted average of the consensus of analysts’ predicted earnings. The lower the Forward P/E, the cheaper the company.

- enterprise value-to-cash flow from operations - The ratio of the entire economic value of a company to the cash it produces. When you divide EV by CFO, you're essentially calculating the number of years it would take to buy the entire business if you were able to use all the company's operating cash flow to buy all the outstanding stock and pay off all the outstanding debt. The lower the ratio, the faster a company can pay back the cost of its acquisition, or generate cash to reinvest in its business.

The use of forward earnings estimates can help mitigate the potential for investing in those companies whose valuation might appear favourable, but where earnings growth is low or even negative, causing book value to stagnate. This is what MSCI’s Enhanced Value approach aims to do.

Compared to a traditional value approach, MSCI’s enhanced value overcomes many of the criticisms of value because it puts less weight on price-to-book as a metric and moves away from backward-looking dividend yield altogether. It uses a whole-firm valuation measure in enterprise value that could reduce concentration in leveraged companies.

It also employs a sector-neutral approach that MSCI found mitigates some of the drawdown inherent with the value investing style.

VLUE’s sector neutrality has been pivotal to the fund’s recent performance. The 2025 value rally was broad-based and sector diversified. VLUE's design meant it participated across the full width of the value rotation, not just in one corner of it. I am able to provide attribution details upon request.

We have written about factor investing, and we have many resources available, including a microsite on value investing – here

Five years ago, investing in international value required patience and a willingness to look different from the crowd. Many had declared value investing dead. It wasn't. VLUE's five-year track record, built through a pandemic, a rate shock, and an AI-driven market, reflects exactly what disciplined value investing looks like.

Looking ahead, if inflation proves persistent, market leadership continues to broaden beyond US mega caps, or global manufacturing conditions improve, we believe the case for VLUE remains as compelling as ever.

You can read more about value investing - here.

We think VLUE provides a compelling alternative to active funds and ETFs that track traditional indices or similar reproductions of these, even after you consider fees.

In celebration of VLUE’s fifth birthday, let's compare it to the widely used international equity benchmark, the MSCI World ex Australia Index (‘International Equity Index’).

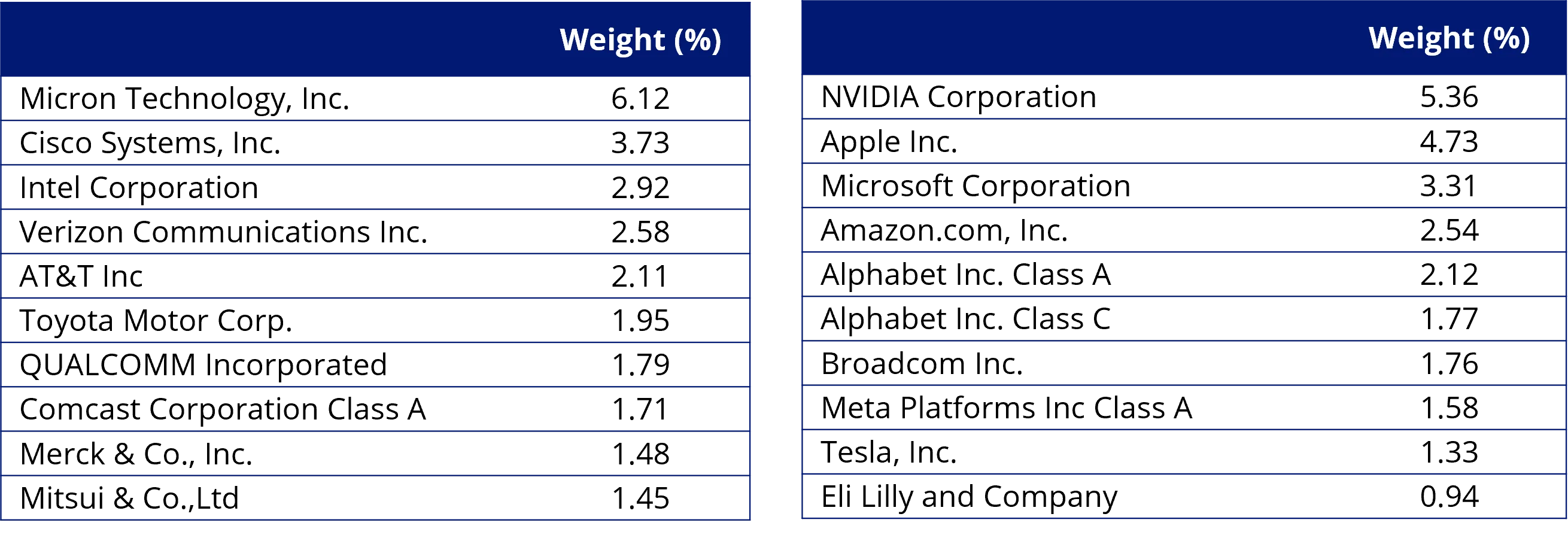

VLUE vs International Equity Index - top 10 holdings

Below you can see the top 10 companies. The top 10 holdings in both lists are companies that investors can relate to in their day-to-day lives – to see all the holdings in VLUE and their weightings click here. There are no companies that appear in the top 10 of VLUE and the International Equity Index.

Table 2 and 3: Top 10 holdings VLUE and top 10 MSCI World ex Australia Index

Source: FactSet, VanEck, MSCI, as at 31 March 2026. Not a recommendation to act.

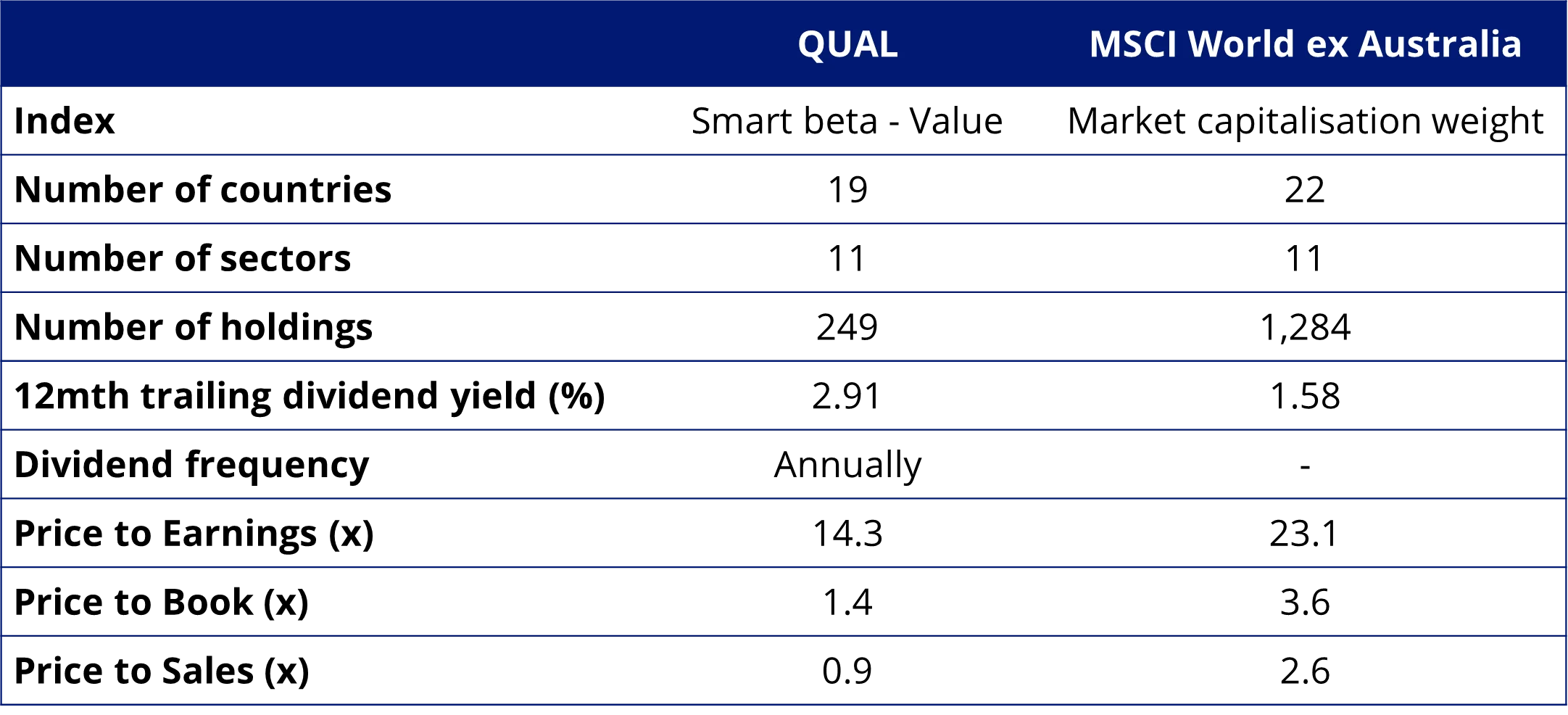

VLUE vs International Equity Index – Fundamentals

Table 4: Statistics and fundamentals

Source: VanEck, MSCI, FactSet, as at 31 March 2026. You cannot invest directly in an index.

As expected, VLUE has a lower price to earnings, lower price to book and lower price to sales.

VLUE through the economic seasons

Over the past 5 years, it has been challenging for investors to navigate economic conditions and prevailing markets. A lot has changed, and the world has been through a lot. Now, there has been much speculation whether the war in Iran will lead to inflation, higher rates and a global slowdown. In response to inflation, the RBA has already hiked rates twice this year.

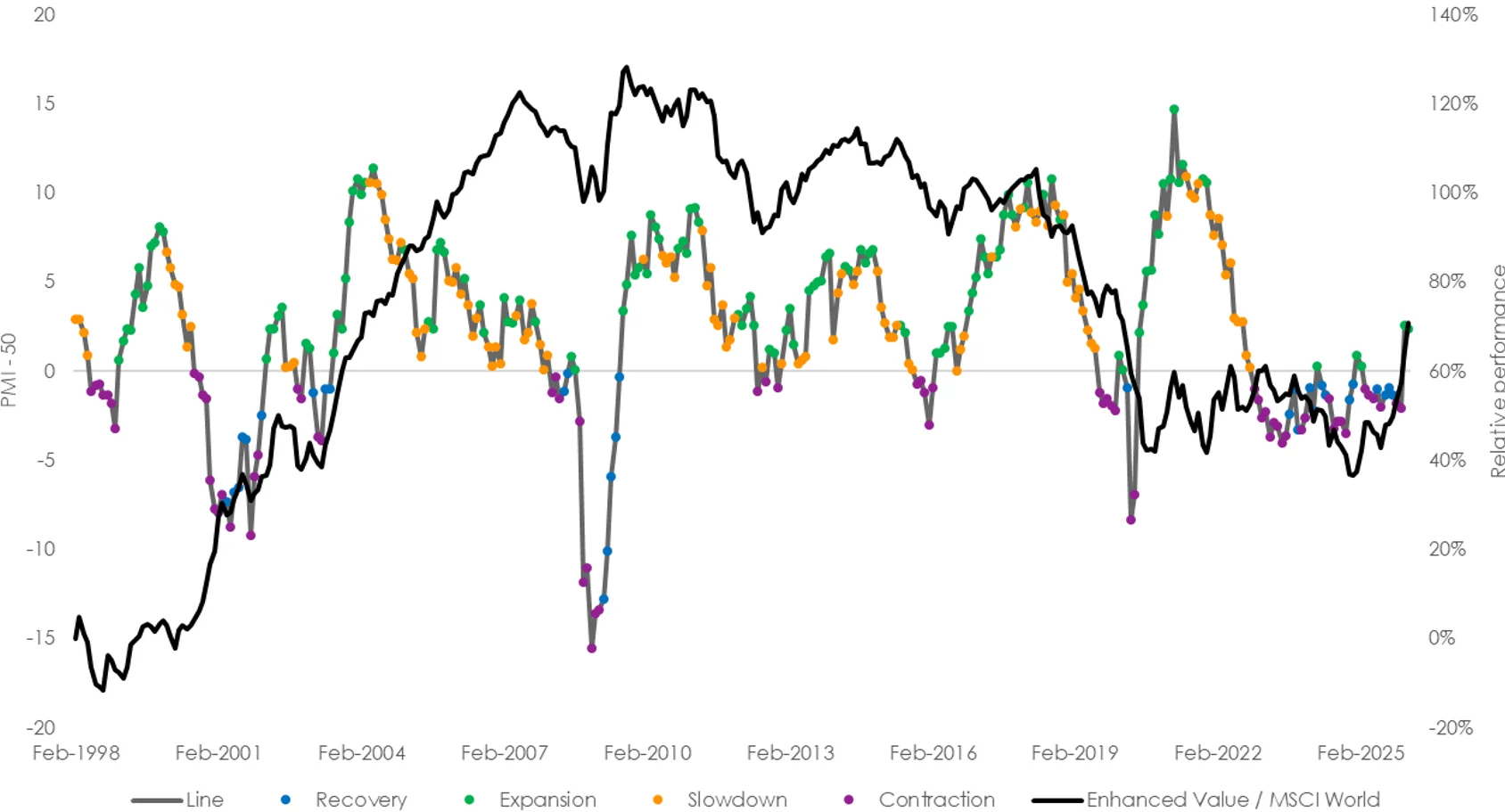

To illustrate how the value factor may perform in the current economic environment, in Chart 1 below, we overlay the manufacturing activity (a proxy for economic activity) with the relative performance of value (MSCI World Enhanced Value Index/MSCI World Index) as represented by the black line. When the black line is rising, value is outperforming. In the chart below, each economic ‘season’ is represented by a colour: recovery (blue), expansion (green), slowdown (orange) and contraction (purple).

Chart 2: US ISM Manufacturing PMI Index and relative MSCI World Enhanced Value performance

Source: Bloomberg, MSCI, 31 March 2026. Past performance is not indicative of future performance. Enhanced Value and MSCI World represented by the MSCI World Enhanced Value Index and MSCI World Index, respectively.

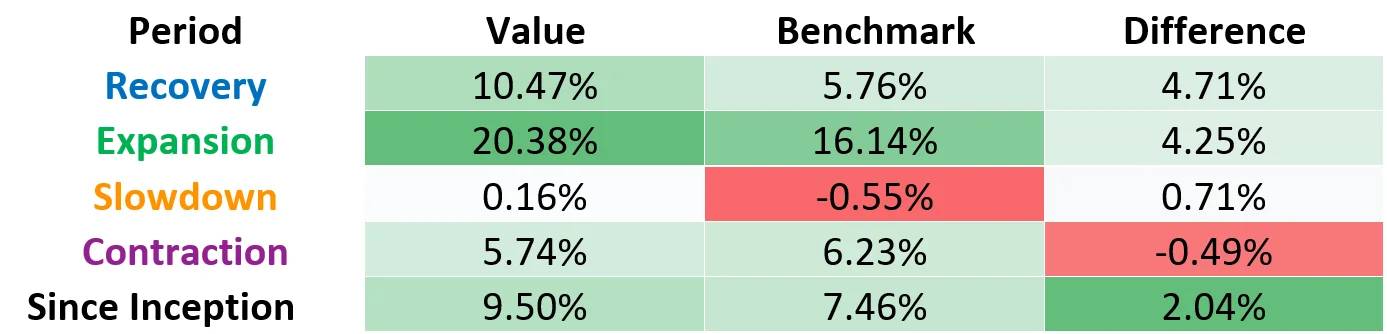

The black line illustrates that value had periods of outperformance (pre-GFC) and underperformance (post-GFC), and that these tend to correlate with the economic cycle. The table below represents the returns of the value factor through the cycle.

Table 5: Value factor performance during different economic regimes

Source: Bloomberg, MSCI, 31 March 2026. Past performance is not indicative of future performance. Value and Benchmark are represented by the MSCI World Enhanced Value Index and MSCI World Index, respectively.

You can see that value historically outperformed most during a recovery and subsequent expansion. You can see, on the right side of the chart, there is a cluster of blue dots on the PMI line, and these correspond to value’s recent outperformance, and the most recent reading was a green dot (expansion). It is typical, in expansionary periods, that inflation is high. Should this continue, there is potential value will continue to outperform. While we always point out that past performance cannot be relied upon for future performance.

We’ve highlighted Value’s recent rally here and here.

HVLU is an Australian-dollar hedged version of VLUE, so you can now also manage your desired currency exposure.

Past performance is not indicative of future performance. The above is not a recommendation. Please speak to your financial adviser or stock broker.

Key risks

An investment in our international value ETF carries risks associated with: ASX trading time differences, financial markets generally, individual company management, industry sectors, foreign currency, country or sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the VanEck MSCI International Value ETF PDS and TMD for more details.

VLUE is likely to be appropriate for a consumer who is seeking capital growth, is intending to use the product as a major, core, minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

Published: 02 April 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.

VLUE is indexed to a MSCI index. VLUE is not sponsored, endorsed or promoted by MSCI, and MSCI bears no liability with respect to VLUE or the MSCI Index. The PDS contains a more detailed description of the limited relationship MSCI has with VanEck and VLUE.