What have the Romans ever done for us?

Reg of the People’s Front of Judea, played by John Cleese, asks this rhetorical question in The Life of Brian. The gag becomes the immediate responses from his fellow revolutionaries highlighting the positive aspects of Roman occupation. They helpfully point out that the hated invaders had brought them sanitation (remember what the city used to be like), roads (the roads go without saying), wine (we’d really miss the wine if the Roman’s left) and the aqueduct. Today we refer to these basic amenities as infrastructure (yes, not the wine). Two thousand years later investing in infrastructure is no longer restricted to governments. Infrastructure securities are becoming more popular with all types of investors.

According to the Online Etymology Dictionary, the word ‘infrastructure’ has been used in English since 1887 and is derived from the addition of the Latin prefix ’infra’, meaning ’below’, to ’structure’. According to the European Union Infrastructure is the backbone of development and social welfare. Roads and railways allow workers and goods to move faster and enable people to get access to public services; telecommunications allow them to communicate and learn; water supply systems enable drinking water and sanitation.

In Roman times infrastructure mainly consisted of roads and canals. The more advanced settlements had aqueducts and some had sewers. Rome itself had the Colosseum for entertainment, the Basilica for public administration and the Horreum for mass storage of grain and other consumables. These were provided by the government and paid for by taxes. These expensive, long lived assets were built to facilitate the operation of society and they enabled the prosperity of the economy.

Throughout history infrastructure has been the foundation of economic growth and the complexities and demand for infrastructure is increasing. Since the industrial revolution humans have migrated from rural to urban areas. Our population is growing especially in cities. According to the UN in 1979 there were only three cities with a population over 10 million. In 2015 there were 23. Today we transact more and more with international trading partners. Demand for mobile telecommunications, lightning quick internet speeds, airports and transport continues to grow.

These changes as well as dynamic regulatory and commercial environments have made it difficult for governments to match the demands of their constituents. This has led to the privatisation of public assets and the necessity for private enterprise to create infrastructure which in turn has led to the development and growth of infrastructure securities.

Infrastructure securities are listed on exchanges around the world and include the builders of roads, railways and bridges, toll road operators, telecommunication providers, satellite operators, companies involved in the storage and transportation of oil and gas reserves and airport operators to name just a few.

Infrastructure securities benefit from a number of key investment advantages being:

- High barriers to entry: There are limited places where a rail can be laid or a bridge can be built. The benefit of no competition, even if pricing is regulated, is significant as it results in a more stable income stream for investors compared to the earnings volatility of other equity investments.

- Protection from inflation: Unlike other income generating investments such as fixed income, investors in infrastructure securities also benefit from the link to inflation which is derived from:

- regulated income which has annual CPI-based adjustments, as is often the case with airports or toll roads, or

- CPI-based increases on consumer prices, such as with utility companies.

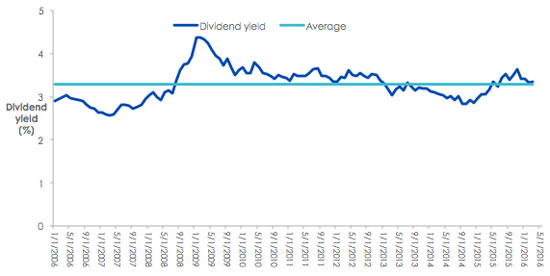

- Dependable income: Chart 1 shows the 10 year average dividend income of 3.3% from inflation linked infrastructure securities.

Chart 1

Source: FTSE from 1 January 2006 to 30 April 2016.

- Low correlation to other asset classes: Infrastructure securities have demonstrated a low correlation to other asset classes providing diversification benefits for investors wishing to complement their existing asset classes. The table below shows the correlation of global infrastructure compared to other asset classes.

Table - Correlation of infrastructure to other asset classes

Source Morningstar Direct, Five year correlation 1 May 2011 - 30 April 2016. Results are calculated monthly and assume immediate reinvestment of all dividends. You cannot invest in an index. Past performance is not a reliable indicator of future performance.

Indices used Cash - RBA target cash rate, International Bonds - Barclays Global Aggregate Bond Index A$ Hedged, Australian Bonds - Bloomberg AusBond Composite 0+ years, Infrastructure - FTSE Index, International Equities - MSCI World ex Australia Index , Australian Equities - S&P/ASX 200 Accumulation Index, Commodities - S&P GSCI Commodities Index

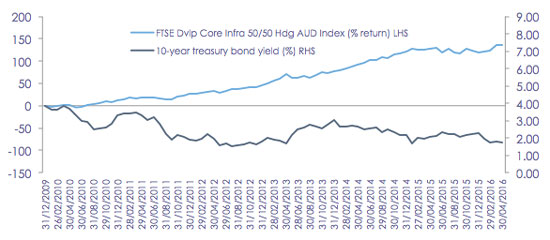

- Benefiting from the current global interest rate environment: In an environment in which interest rates in the world’s developed economies are at historic lows investors have been forced to allocate assets to riskier investments in a search for yield. Global listed infrastructure has become popular as it provides investors with an opportunity to access companies with high dividend yields, good capital growth and low volatility of returns. Chart 2 shows the performance of the FTSE Developed Core Infrastructure 50/50 Hedged into Australian Dollars Index in comparison to the US 10-year Treasury bond yield.

Chart 2

Source: FTSE, Morningstar Direct from 31 December 2009 to 30 April 2016.

Accessing global infrastructure securities has recently become easier for Australian investors with the launch of the first global infrastructure ETF (exchange traded fund) on the ASX. VanEck Vectors FTSE Global Infrastructure (Hedged) ETF (ASX code: IFRA) tracks the FTSE Developed Core Infrastructure 50/50 Hedged into Australian Dollars Index and provides investors with access to a portfolio of 154 of the world’s largest infrastructure securities in a single trade on ASX.

If you would like more information on IFRA please contact our ETF specialists on 02 8038 3300 or email us at [email protected]

IMPORTANT NOTICE: This information is issued by VanEck Investments Limited ABN 22 146 596 116 AFSL 416755 (‘VanEck’) as responsible entity and issuer of the VanEck Vectors FTSE Global Infrastructure ETF (‘Fund’). This is general information only and not financial advice. It is intended for use by financial services professionals only. It does not take into account any person’s individual objectives, financial situation or needs. Before making an investment decision in relation to the Fund, you should read the PDS and with the assistance of a financial adviser consider if it is appropriate for your circumstances. The PDS is available at www.vaneck.com.au or by calling 1300 68 38 37. The Fund is subject to investment risk, including possible loss of capital invested. Past performance is not a reliable indicator of future performance. No member of the VanEck group of companies gives any guarantee or assurance as to the repayment of capital, the payment of income, the performance, or any particular rate of return from the Fund.

IFRA invests in international markets. An investment in IFRA has specific and heightened risks that are in addition to the typical risks associated with investing in the Australian market. These include currency risks from foreign exchange fluctuations, ASX trading time differences and changes in foreign laws and regulations including taxation.

The Fund is not in any way sponsored, endorsed, sold or promoted by FTSE International Limited or the London Stock Exchange Group companies (‘LSEG’) (together the ‘Licensor Parties’) and none of the Licensor Parties make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to (i) the results to be obtained from the use of the FTSE Developed Core Infrastructure 50/50 Hedged into Australian Dollars Index (with net dividends reinvested) (‘Index’) upon which the Fund is based, (ii) the figure at which the Index is said to stand at any particular time on any particular day or otherwise, or (iii) the suitability of the Index for the purpose to which it is being put in connection with the Fund. None of the Licensor Parties have provided or will provide any financial or investment advice or recommendation in relation to the Reference Index to VanEck or to its clients. The Reference Index is calculated by FTSE or its agent. None of the Licensor Parties shall be (a) liable (whether in negligence or otherwise) to any person for any error in the Reference Index or (b) under any obligation to advise any person of any error therein. All rights in the Reference Index vest in FTSE. “FTSE®” is a trade mark of LSEG and is used by FTSE and VanEck under licence.

Published: 09 August 2018