Is Australian Quality investing on sale?

Today, we think investors have a rare opportunity to invest in quality companies while they are at a discount.

Dividend yield is the weighted average of each portfolio security’s distributed income during the prior twelve months. This is not indicative of future dividend distributions of AQTY.

A compelling opportunity in Australian equities is emerging

The quality factor has had a rough few years, leading some investors to ask why it has underperformed and whether it still works at all.

It is an understandable question. When an investment style struggles for long enough, investors inevitably begin to wonder whether something has changed for good.

But the truth is that quality investing has always been cyclical. Periods of underperformance have historically been followed by periods in which investors place greater emphasis on profitability, earnings quality and valuation discipline. The more interesting question is whether today's market is creating one of those opportunities.

In Australia, there is growing evidence they might.

An unusual combination

Investors are accustomed to paying a premium for quality.

Companies with strong balance sheets, resilient earnings and high returns on capital tend to trade at higher valuations than the broader market. That has long been one of the implicit trade-offs of quality investing. Today, however, something unusual is happening in Australian equities.

As at 8 June 2026, the companies held in the VanEck Australian Quality Plus ETF (ASX: AQTY) exhibited higher return on equity, lower valuations and a higher dividend yield than the S&P/ASX 200. They also traded at lower valuations than the broader market.

Table 1: AQTY fundamentals versus the S&P/ASX 200

|

Metric |

AQTY |

S&P/ASX 200 |

|

ROE (%) |

14.43 |

13.72 |

|

Historical 3-Year Sales Growth (%) |

10.00 |

13.56 |

|

Dividend Yield (%) |

3.61% |

3.27% |

|

Price-to-Earnings (x) |

19.82 |

20.57 |

|

Price-to-Earnings using FY1 Est (x) |

15.87 |

17.44 |

|

Price-to-Book (x) |

2.29 |

2.42 |

|

Price-to-Sales (x) |

1.59 |

2.09 |

|

Price-to-Cash Flow (x) |

11.22 |

12.34 |

Source: FactSet, as at 8 June 2026.

Why income and valuations matters again

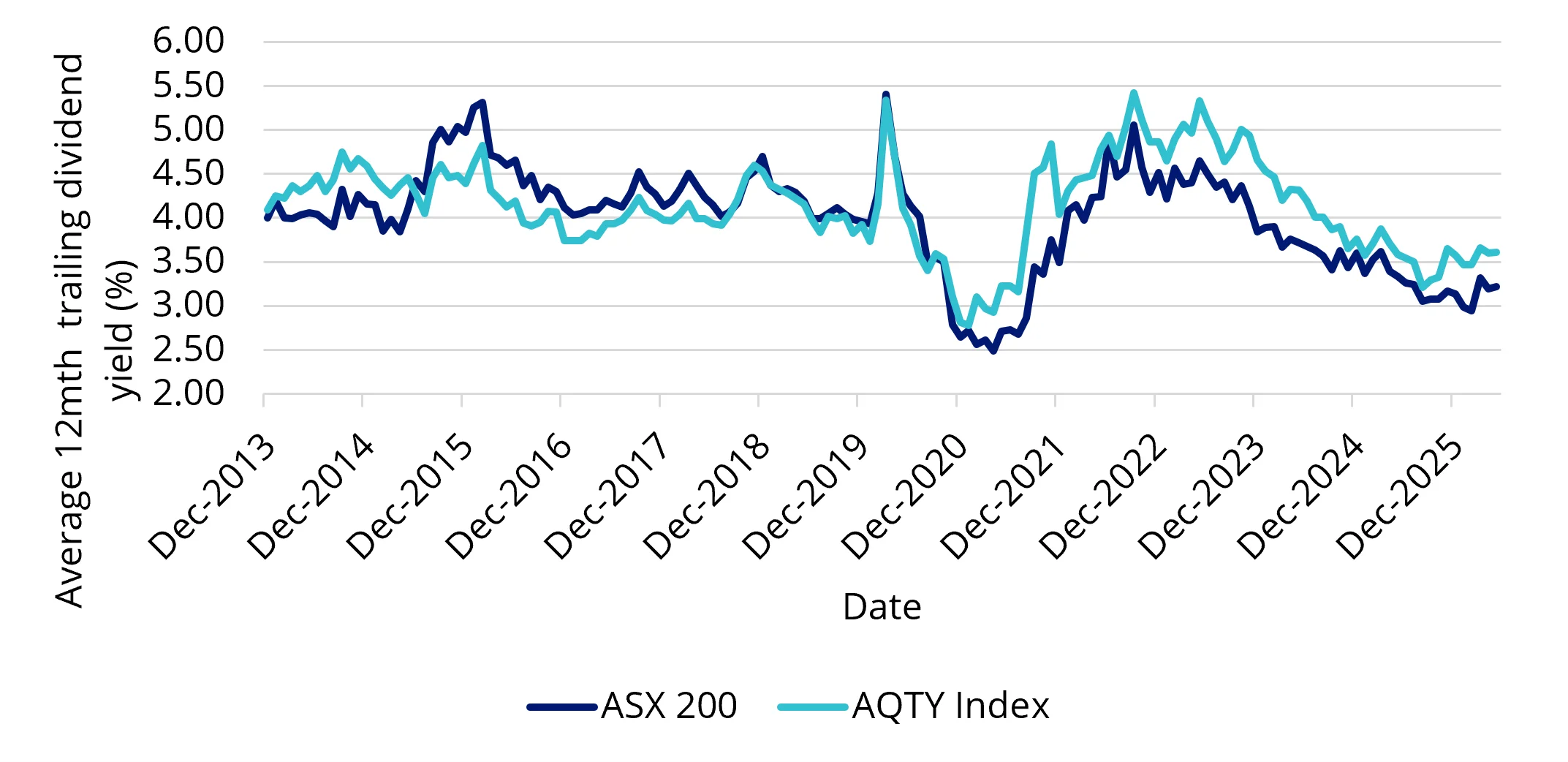

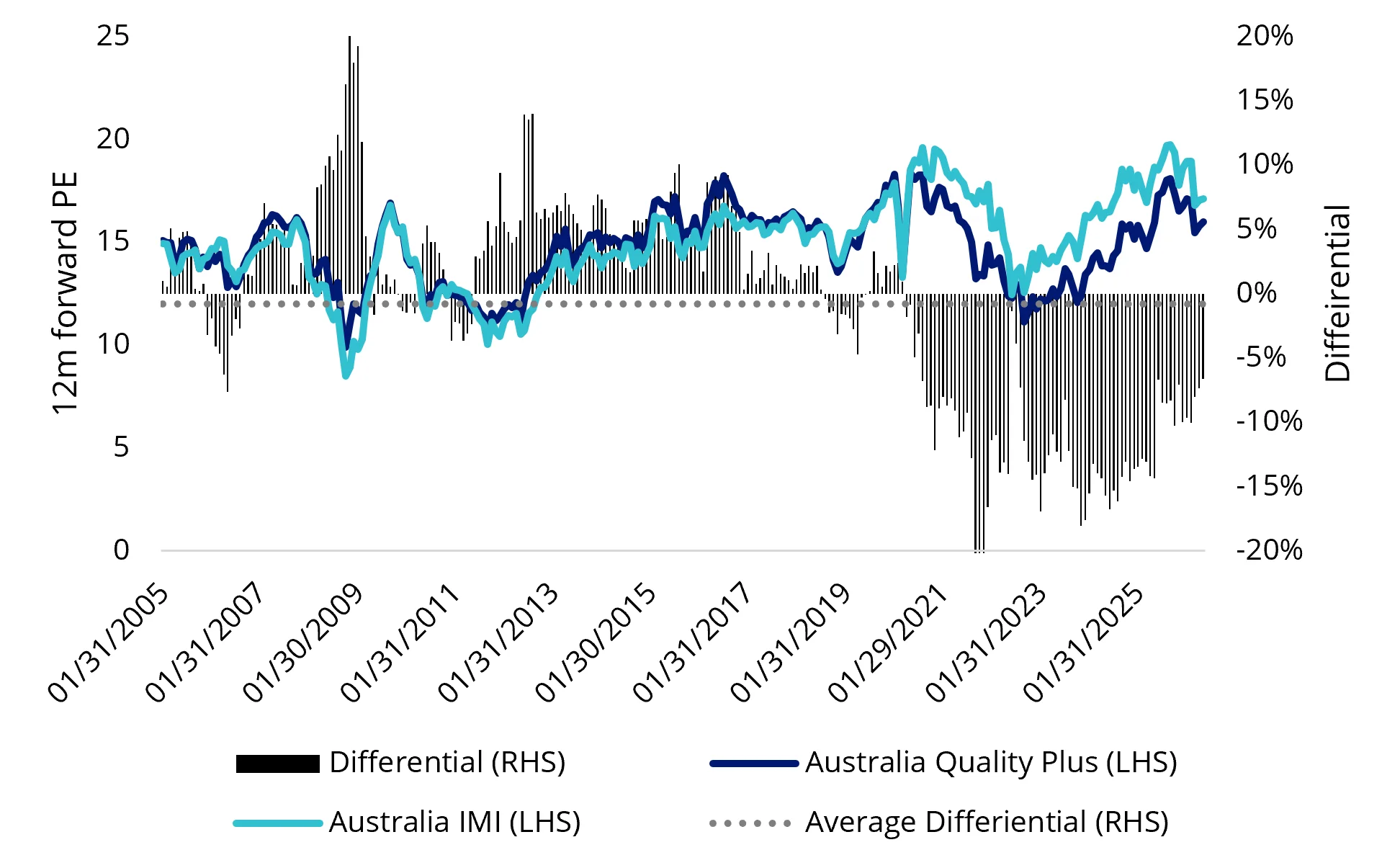

As at 8 June 2026, the companies held in AQTY offered a dividend yield of 3.61%, higher than the S&P/ASX 200. More importantly, this is not simply a point-in-time observation. Since December 2020, the AQTY Index has exhibited a higher average trailing dividend yield than the S&P/ASX 200. And it has been cheaper over that time, based on price-to-12-month forward earnings.

Chart 1: Average 12-month trailing dividend yield: S&P/ASX 200 vs AQTY Index

Source: VanEck, MSCI, FactSet as at 31 May 2026. Past performance of the AQTY Index is not indicative of the future performance of AQTY. You cannot invest in an index.

Chart 2: 12-month forward earnings comparison: ASX 200 vs AQTY Index

Source: VanEck, MSCI, 1 January 2005 to 31 May 2026.

That is noteworthy because it adds another dimension to an already compelling combination of characteristics. Investors are currently receiving stronger profitability and lower valuation multiples than the broader market (currently, a 6% discount based on price-to-12-month forward earnings), while also benefiting from a modest yield advantage.

The timing is also interesting. Following the recent Federal Budget and renewed debate around capital gains tax, investors and advisers are paying closer attention to where returns come from, not simply how large they are. In that environment, a portfolio that combines quality, valuation discipline and a history of competitive income generation may be particularly relevant.

Taken together, those characteristics reinforce what is already an unusual proposition in Australian equities.

The Australian market's blind spot

To understand why quality looks so attractive at the moment, it helps to understand the structure of the Australian share market.

Australia is one of the most concentrated developed equity markets in the world. As we have discussed previously, about half of the S&P/ASX 200 is represented by just ten companies, while Financials and Materials account for more than half of the benchmark.

This concentration has important implications for investors. Market-cap weighted indices allocate more capital to companies simply because they have become larger. They do not ask whether those companies are attractive on a valuation basis, whether their earnings are resilient or whether a stock’s inclusion would improve portfolio diversification.

As a result, many investors end up with portfolios that are more concentrated than they realise. At the same time, high-quality businesses outside that group can become overlooked, even when their fundamentals remain strong. This helps explain why quality stocks can exhibit stronger business characteristics and lower valuations than the broader market at the same time.

The challenge is that identifying those opportunities is not always straightforward. In a market like Australia’s, where so much of the index is occupied by so few companies, the same concentration that creates opportunities for quality businesses can also create challenges for traditional quality strategies.

Why quality needs to be done differently

Quality investing behaves differently in Australia. The same structural features that shape the broader market can also influence the outcomes delivered by traditional quality strategies. During favourable parts of the commodity cycle, resource companies can score highly on conventional quality measures, resulting in portfolios that look very different from what investors typically expect from a quality strategy.

The issue is not that the quality factor is broken. It is that Australia's market structure creates unique challenges that simple quality screens do not always overcome. It is this insight that sits at the heart of AQTY.

Rather than relying solely on traditional quality measures, the MSCI Australia IMI Quality Plus Index (AQTY Index) combines quality with enhanced value, low volatility and a momentum overlay. Quality remains at the heart of the portfolio, with an emphasis on businesses that have consistently demonstrated an ability to generate profits, grow earnings and manage their balance sheets responsibly. Value introduces valuation discipline. Low volatility helps offset some of the cyclical risks that have historically challenged quality investing in Australia. Finally, momentum helps identify companies whose fundamentals are improving while filtering out potential deterioration.

Together, these characteristics create a more complete definition of quality and a portfolio that is designed to work within the realities of the Australian market rather than against them.

Key points:

- Quality, outcome engineered: In Australia, quality is often assumed through banks and large defensives. This portfolio is built for the realities of a narrow, cyclical market and deliberately engineered to moderate sector tilts, so the outcome reflects portfolio construction, not index bias.

- Defensive when it matters, not just in theory: Quality is often advocated as a defensive exposure. But in Australia, it can still fall alongside the market. By incorporating price stability and valuation discipline, the portfolio is designed to cushion the downside when markets weaken, without giving up the upside when they recover.

- A more balanced source of performance: Returns are driven by multiple complementary signals that blend quality with valuation and stability rather than relying on a single factor regime. This reduces dependence on any environment and aims to deliver more consistent risk-adjusted outcomes through cycles.

As at 8 June 2026, the companies held in VanEck’s Australian Quality Plus ETF (AQTY) exhibited higher return on equity and a higher dividend yield than the S&P/ASX 200, while trading at lower valuations across virtually every major measure.

AQTY's dividend yield currently exceeds that of the S&P/ASX 200 and has historically been competitive with the benchmark, adding another dimension to the investment case.

For investors seeking a high quality Australian equity allocation without paying the traditional quality premium, AQTY may warrant consideration.

You can also read our new paper The Narrow Market, Untangled which explains the theory behind AQTY’s philosophy. You can access that here.

Key risks

An investment in the ETF carries risks associated with financial markets generally, individual company management, industry sectors, fund operations and tracking an index. See the PDS and TMD for more details.

AQTY is likely to be appropriate for a consumer who is seeking capital growth and a regular income distribution, is intending to use the product as a minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

Published: 16 June 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.