Analysis: AQTY

The idea of investing in quality companies sounds intuitive. But it is easier said than done, because quality outcomes are not always easily achieved.

Australian investors have long sought active outcomes like higher dividends, outperformance and/or better diversification when investing in Australian equities.

The rise of ETFs has increased the opportunity set and further opened the Australian equity investing landscape.

Historically, outside of investing directly in stocks, there have been three popular approaches to investing in Australian equities:

- via an actively managed fund; or

- via a passive fund or ETF tracking a benchmark index; or

- via a smart beta ETF that tracks an index to achieve a targeted investment outcome.

Quality investing, which is associated with falling less in a downturn and recovering to previous highs more quickly, is an example of the targeted outcome that an ETF classified under the smart beta category might target. To date, finding Australian equity ETFs that achieve quality outcomes in a tight, concentrated market like Australia has been difficult.

A Morningstar article titled Where to find opportunity in an expensive market, earlier in the year, summed up this conundrum.

“Defining quality stocks in Australia is a little fuzzier,” the author explained, highlighting the markedly disparate returns between three Australian equity quality indices. “Why the big gaps in performance? Well, each of them filters different characteristics for quality stocks, and I’m not sure any of them get it close to right.”

This may be why many investors have also used actively managed funds for Australian equities. Often, an active manager will describe themselves by a targeted outcome, like value, growth or quality. The problem with these active funds, relative to passive approaches, is that performance has historically been uncertain, and costs are higher. In the past, sometimes the returns were consistent with a quality outcome, but they were often not.

Many people found this a poor bargain and so have given up on a targeted outcome and moved to lower-cost passive funds and ETFs that track traditional indices like the S&P/ASX 200. In these funds, returns could be thought of as the market average.

When it comes to Australian equity investing in a passive fund, the widely used benchmark is the S&P/ASX 200 Index; for ease of reading, let’s call it the Aussie Equity Index. This index has 200 companies, and not all of them are desirable from an investing point of view.

We think Australian equity investors should not give up on quality in Australia. We previously flagged a new quality approach to Australian equities – here.

It is this approach that VanEck now offers in Australian equities alongside our other Australian equity funds, and it is being used by savvy investors as a substitute for the other two popular approaches. The VanEck MSCI Australia Quality Plus ETF (AQTY) is the result of many years of analysis and consideration from the smart beta leaders in Australia: VanEck. We think it provides Australian investors with a way to achieve quality investment outcomes in their home market for the first time.

AQTY tracks the MSCI Australia IMI Quality Plus Index (AQTY Index), and it uses quality as an anchor for company inclusion while also considering factors such as value (to avoid overpaying) and low price variability (to reduce unexpected volatility) to help achieve its targeted outcome.

You can read more about the creation of the AQTY Index here.

We think AQTY provides a compelling alternative to ETFs that track the Aussie Equity Index and to other quality approaches, which Morningstar described as “not close to right”.

So, let’s walk through the difference between the index AQTY tracks and the Aussie Equity Index.

Hypothetical performance

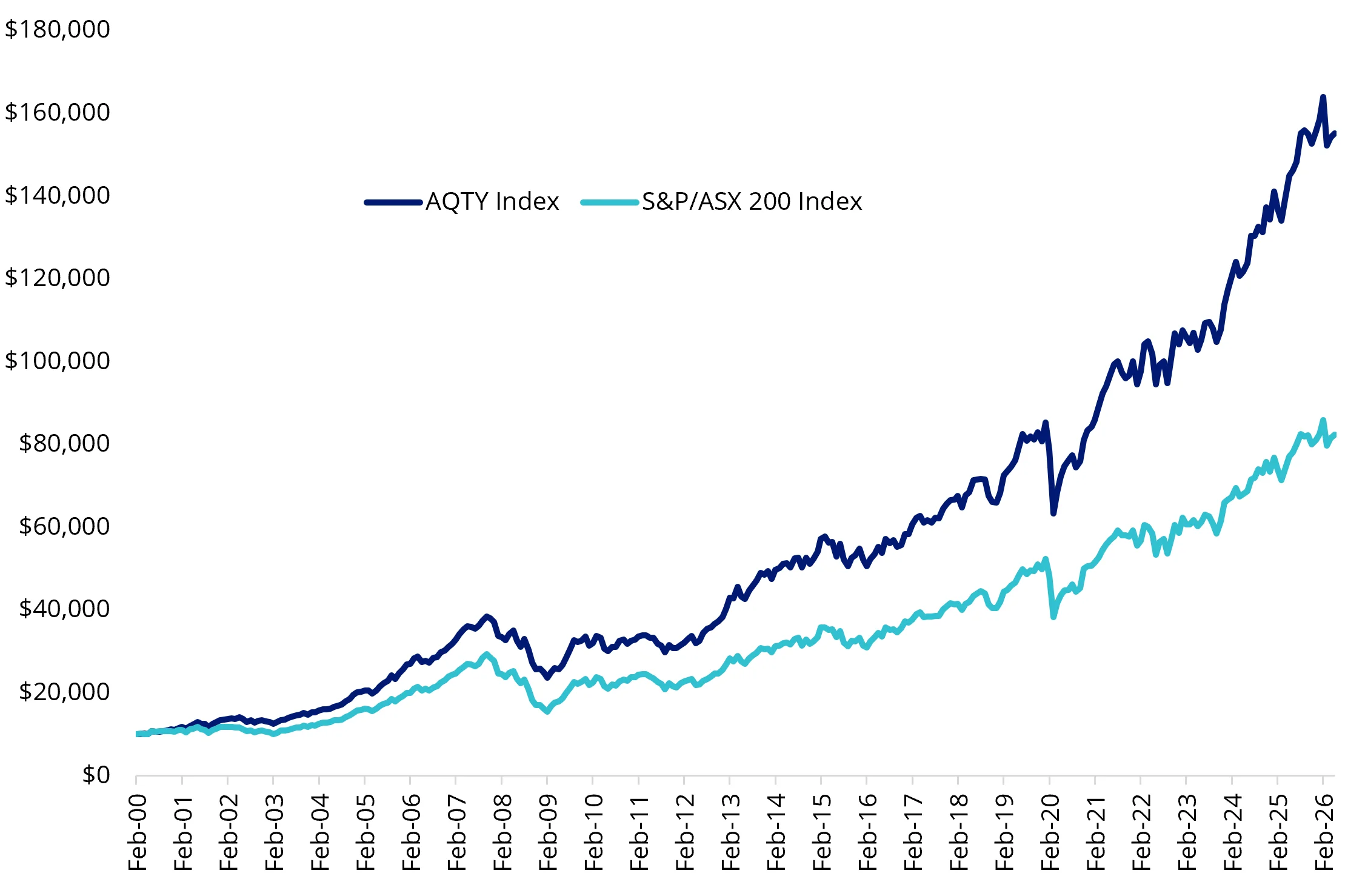

In our research paper, The narrow market, untangled, we analysed and presented performance data of the AQTY Index and the Aussie Equity index. The AQTY Index has a data series that extends back to 29 February 2000, though data before the live index launch in May 2026 is simulated. An updated hypothetical growth of $10,000, AQTY Index vs S&P/ASX 200 chart and trailing returns table from the paper are presented below, noting that the observation is based on simulated as well as live data, and should not be relied on as an indicator of future.

Chart 1: Hypothetical growth of $10,000, AQTY Index vs S&P/ASX 200

Table 1: Trailing performance to 31 May 2026

|

Trailing period |

AQTY Index (% p.a.) |

S&P/ASX 200 (% p.a.) |

Difference |

|

1 Year |

7.13 |

6.89 |

+0.24 |

|

3 Years |

14.67 |

11.02 |

+3.65 |

|

5 Years |

10.52 |

8.10 |

+2.41 |

|

10 Years |

10.88 |

9.10 |

+1.78 |

|

15 Years |

10.80 |

8.58 |

+2.22 |

Source Chart 1 & Table 1: VanEck The narrow market, untangled pp10-11, MSCI, S&P, Morningstar Direct, 29 Feb 2000 to 31 March 2026. AQTY Index is the MSCI Australia IMI Quality Plus Index. You cannot invest in an index. Past performance is not indicative of future performance of the index or of AQTY. Results are calculated to the last business day of the month and assume immediate reinvestment of dividends.

AQTY vs S&P/ASX 200 Index – Fundamentals

Table 2: Statistics and fundamentals

|

|

AQTY Index |

S&P/ASX 200 |

|

Index strategy |

Smart beta |

Market capitalisation weight |

|

Number of sectors |

11 |

11 |

|

Number of holdings |

50 |

200 |

|

ROE (%) |

14.68 |

13.81 |

|

Long-term forward EPS Growth (%) |

8.17 |

7.81 |

|

Price/Earnings* |

20.13 |

20.99 |

|

Dividend Yield (%)* |

3.55 |

3.20 |

|

Price/Book* |

2.32 |

2.47 |

|

Price/Sales* |

1.61 |

2.14 |

Weighted average *Weighted harmonic average

Source: VanEck, Factset, as at 23 June 2026. Not a recommendation to act. You cannot invest in an index. Data used before May 2026 is simulated. Dividend yield is not guaranteed. Past performance is not indicative of future performance.

As you would expect from a quality index, AQTY Index has higher return on equity (ROE), higher long-term forward earnings per share (EPS) growth as well as a lower average price to book, price to sales and price to earnings ratio than the S&P/ASX 200.

AQTY Index vs S&P/ASX 200 Index - Sectors

AQTY Index is currently underweight real estate and health care, but overweight energy compared to the S&P/ASX 200. When you look at it on a subsector level, you can see it as overweight sub sectors such as consumer discretionary distribution & retail, and commercial & professional services.

Chart 2: GICS sector weight differential: AQTY Index v S&P/ASX 200 Index Chart 3: GICS sub-sector weight differential: AQTY Index v S&P/ASX 200 Index

Source: VanEck, FactSet; as at 23 June 2026. AQTY Index is represented by MSCI Australia IMI Quality Plus Index Calculated by subtracting S&P/ASX 200 Index from respective AQTY Index sector and sub-sector weights; positive differentials indicate greater AQTY Index weight in the sector and sub-sector. You cannot invest in an index. Future weightings may differ.

AQTY was made available to Australian investors on 1 June 2026. In Australia, quality is often assumed through banks and large defensives. But the outcomes of trying to apply a quality investing approach to the Aussie equity index often tend to not reflect the theory. This portfolio, however, is built for the realities of a narrow, cyclical market, and it has been deliberately engineered to moderate sector tilts. The outcome therefore reflects portfolio construction, not index bias.

The above analysis is not a recommendation. Please speak to your financial adviser or stock broker.

Key risks

An investment AQTY carries risks associated with: ASX trading time differences, financial markets generally, individual company management, industry sectors, country or sector concentration, political, regulatory and tax risks, fund operations and tracking an index. See the PDS and TMD for details.

AQTY is likely to be appropriate for a consumer who is seeking capital growth and a regular income distribution, is intending to use the product as a minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

Published: 26 June 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.

VanEck MSCI Australian Quality Plus ETF (AQTY) is indexed to a MSCI index. AQTY is not sponsored, endorsed or promoted by MSCI, and MSCI bears no liability with respect to AQTY or the MSCI Index. The PDSs contain a more detailed description of the limited relationship MSCI has with VanEck and the Fund.

© 2026 Van Eck Associates Corporation. All rights reserved.