Why selectivity is key in emerging markets investing

Equity markets have been optimistic since Easter, propelling many markets to record highs.

This optimism has propelled emerging markets to outperform developed markets, despite ongoing geopolitical tensions. Year-to-date, the MSCI Emerging Markets Index, has returned 13.43%, compared to the 0.61% rise of the MSCI World ex Australia Index (1 Jan 2026 to 14 May 2026, source: Morningstar Direct).

Emerging markets make up around 12% of MSCI’s All Country World Index, yet most Australians do not have proportionate international equity exposure to this asset class, fearing volatility and geopolitics.

While many investors, in the past, have been wary of emerging markets, we think they are maturing, and many of the long-term trends such as demographics, technology and the rising middle class have rewired emerging markets and are creating new opportunities.

Being selective in EM could be the right wiring for economies that are re-wiring

Emerging markets are known to be inefficient and under-researched. Investing in them can also be difficult for many investors, in addition to being expensive; many may be restricted, or have idiosyncrasies with trading, regulations and taxes. But returns are potentially attractive, so they should not be overlooked. Emerging markets can be an important diversification tool in a global equity portfolio, by including diverse economies at different stages of the economic cycle and capturing companies that are global leaders in the fields in which they compete.

Beyond the oil crisis

We think there are a number of tailwinds that continue to support the outperformance of emerging markets and EMKT. Because emerging markets have changed over many years, the source of tailwinds is beyond the potential weakness of the US dollar (though that is one we cannot ignore). Other tailwinds include semiconductor optimism, growth in economies such as South Korea and Taiwan, and valuations.

Semiconductors are rewiring EM performance

Driven by surging demand for data centre components, semiconductor companies have significantly outperformed global equities in 2026. Emerging markets chipmakers, including TSMC, SK Hynix and Samsung Electronics, have led the rally, gaining 59.2% year-to-date as of 11 May 2026, despite US-Iran war volatility. As of 30 April 2026, VanEck’s MSCI Multifactor Emerging Markets Equity ETF (EMKT) has a 22.8% exposure to semiconductor names, an overweight of 11.5% and 1.6% compared to the MSCI Emerging Markets Index and the MSCI World ex Australia Index, respectively.

Chart 1: Year to date performance of semiconductor indices

Source: Bloomberg. 12 May 2026. Returns in Australian dollars. Results assume immediate reinvestment of all dividends and exclude costs associated with investing and taxes. You cannot invest directly in an index. Past performance is not indicative of future performance.

The recent earnings season in the US indicates, we think, further upside for this theme, painting an upbeat outlook for emerging market semiconductor names too. In a strong reporting season, roughly 81.4% of companies have beaten earnings estimates, well above the 10-year average of 76.3%. The semiconductor sector was a standout with almost all companies reporting both earnings and revenue beats alongside bullish forward guidance, and US hyperscalers comfortably exceeded analysts’ estimates for AI capex.

This was reflected in emerging markets; among Asian semiconductor firms that reported recently, TSMC and SK Hynix have also delivered strong beats with significant gains post earnings.

Chart 2: International Semiconductor 1-day post-earnings return vs Earnings surprise

Source: Bloomberg. As of 11 May 2026. INTL is not included for the scale of the chart. EPS surprise over 1300%, 1-day return% 23.6% in US dollars.

The majority of advanced semiconductor manufacturing capacity resides in emerging markets, specifically Taiwan and Korea. Taiwan produces the majority of the world’s most advanced chips and is also the leader in advanced packaging, which is the final assembly step that stitches multiple chips together for AI systems. South Korea, through Samsung and SK Hynix, dominates memory chip supply for AI servers. That structural position is why we see emerging markets leading the rally we have seen year to date.

Chart 3: Advanced semiconductor market share by country

Source: World Population Review. 31 December 2025.

US dollar weakness

Beyond their dominance in semiconductors, another structural tailwind for emerging markets is the fact that many emerging economies are net exporters.

They could benefit from a prolonged US dollar downcycle through stronger local currencies, easier financial conditions and improved capital flows. Over time, this could support investment, consumption and external balances, helping to support higher forecast GDP and corporate earnings. The chart below highlights that emerging markets have historically outperformed developed markets when the US dollar weakens. This is represented by the DXY index, which tracks the performance of a basket of foreign currencies relative to the US dollar.

Chart 4: Emerging market equities relative performance versus US Dollar Index (DXY Index)

Source: Bloomberg as at 30 April 2026. You cannot invest in an index. Past performance is not indicative of future performance.

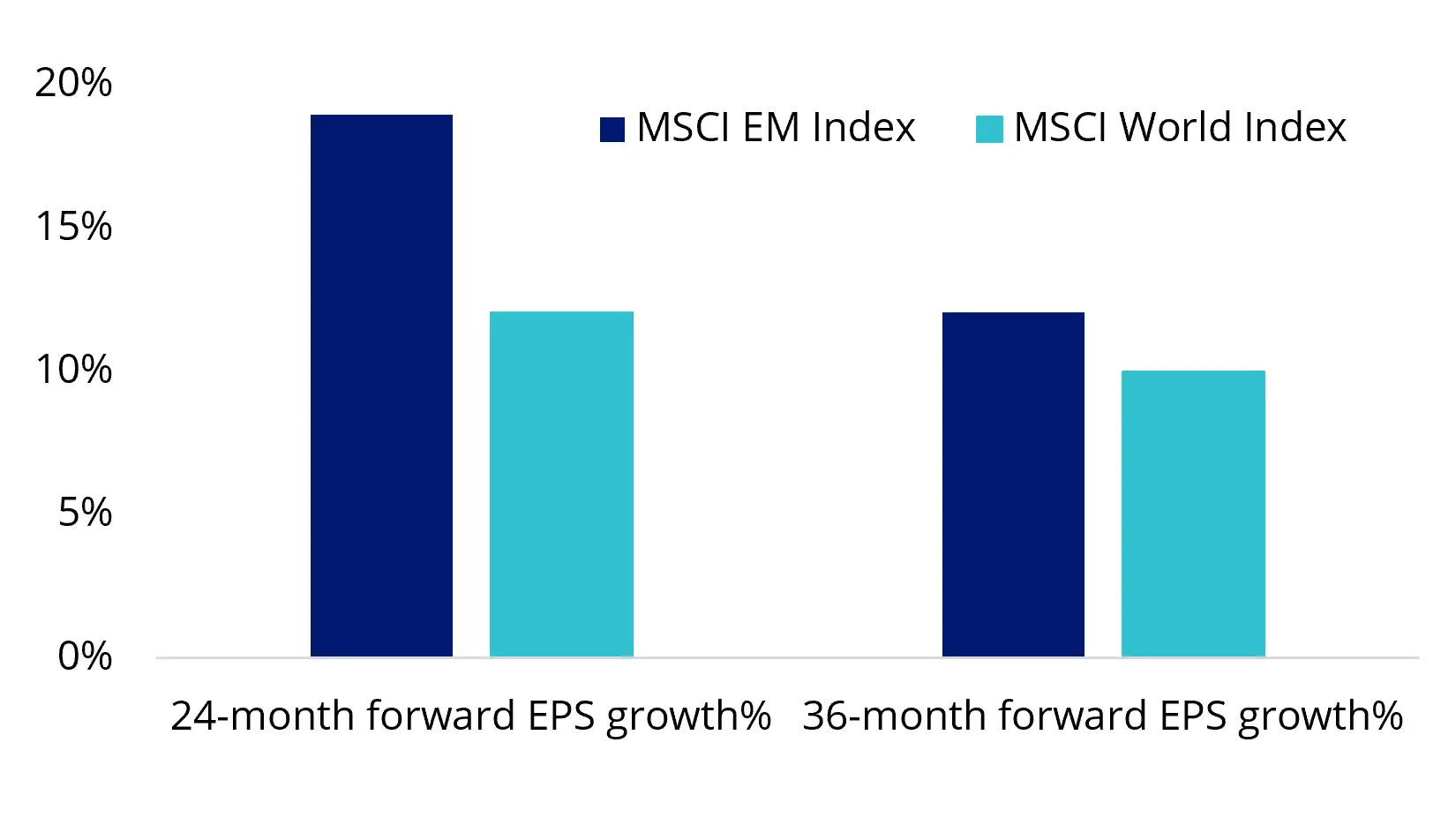

Emerging markets and earnings growth

Emerging market equities, we think, offer growth at a reasonable price. From a valuation standpoint, in the context of global equities, emerging markets look to be compelling. On both price-to-book and price-to-earnings measures, emerging market companies are far lower than developed markets, with the multi-factor, EMKT Index, showing an edge. Earnings outlook also appears to be upbeat for emerging markets, outpacing developed peers into the next three years.

Chart 5 & 6: Index 12-month forward price to earnings and Index Price to book

Source for Charts 5 and 6: MSCI. From 30 June 2003 to 30 April 2026. EMKT Index is the MSCI Emerging Markets Multi-Factor Select Index. Past performance is not indicative of future performance. You cannot invest in an index.

Chart 7: EPS growth: Emerging Markets versus Developed Markets

Source: VanEck. Bloomberg. EPS data as of 30 April 2026.

Being selective

We think being selective in emerging markets equities is important.

The VanEck MSCI Multifactor Emerging Markets Equity ETF (ASX: EMKT) has outperformed the MSCI Emerging Markets Index across every trailing time period, including by 7.79% so far this year (21.22% versus 13.43%), as at 14 May 2026. As always, past performance is not a reliable indicator of future performance.

Table 1: Performance as at 14 May 2026

|

|

MTD |

1 Month (%) |

3 Months (%) |

6 Months (%) |

YTD |

1 year (%) |

3 Years (% p.a.) |

5 Years (% p.a.) |

7 Years (% p.a.) |

Since EMKT inception date# (% p.a.) |

|

EMKT |

10.58 |

13.32 |

12.78 |

20.48 |

21.22 |

42.95 |

26.05 |

16.15 |

14.44 |

10.95 |

|

MSCI Emerging Markets Index |

6.78 |

8.55 |

8.38 |

13.18 |

13.43 |

33.29 |

20.33 |

9.78 |

9.81 |

8.28 |

|

Difference |

+3.80 |

+4.77 |

+4.40 |

+7.30 |

+7.79 |

+9.66 |

+5.72 |

+6.37 |

+4.63 |

+2.67 |

Source: VanEck, Morningstar Direct

#EMKT inception date is 10 April 2018 and a copy of the factsheet is here.

Performance is calculated net of management fees, calculated daily but does not include brokerage costs or buy/sell spreads of investing in EMKT. Past performance is not indicative of future performance.

The MSCI Emerging Markets Index (“MSCI EMI”) is shown for comparison purposes as it is the widely recognised benchmark used to measure the performance of emerging markets large- and mid-cap companies, weighted by market capitalisation. EMKT’s index measures the performance of emerging markets companies selected on the basis of their exposure to value, momentum, low size and quality factors, while maintaining a total risk profile similar to that of the MSCI EMI, at rebalance. EMKT’s index has fewer companies and different country and industry allocations than MSCI EMI. Click here for more details

EMKT’s performance, to the end of last month, puts it in the top quartile of active peers over one, three, five, seven years and since the ETF’s inception, despite charging significantly lower fee than most active managers.

Chart 8: Performance relative to active manager peer group

Source: Morningstar Direct. Past performance is not indicative of future performance. Results are calculated to the last business day of the month and assume immediate reinvestment of distributions. Results are net of management fees and other costs incurred in the fund, but before brokerage fees and bid/ask spreads. Returns for periods longer than one year are annualised. Peer group Equity Region Emerging Markets funds invest in companies listed in emerging markets from around the globe. Emerging market securities typically account for at least 75% of the portfolio.

The efficacy of this approach was supported by the 2024 research paper, titled Factor-in emerging markets. According to the research paper, EMKT’s multi-factor methodology “is an all-seasons approach that has historically outperformed the benchmark over the long term. The bottom-up approach and selection of four factors quality, value, momentum and low size were found to be the most optimal for maximizing Sharpe and information ratios.”

Key points:

- EMKT provides investors with a diversified portfolio of emerging markets equities, included on the basis of:

- value;

- low size;

- momentum; and

- quality.

- EMKT has demonstrated outperformance since its inception against the MSCI Emerging Markets Index, noting as we always do, this is by no means indicative of future performance.

- Access emerging markets equities for a significantly lower cost than comparable active management strategies at a management fee of 0.69% p.a.

- With one trade, EMKT currently provides access to 18 emerging market countries.

Key risks:

All investments carry risk. An investment in EMKT carries risks associated with ASX trading time differences, emerging markets, financial markets generally, individual company management, industry sectors, foreign currency, country or sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the PDS and TMD for details.

EMKT is likely to be appropriate for a consumer who is seeking capital growth, is intending to use the product as a core, minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

Published: 21 May 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.

EMKT is indexed to a MSCI index. EMKT is not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to EMKT or the MSCI Index. The PDS contains a more detailed description of the limited relationship MSCI has with VanEck and EMKT.