The case for emerging markets after the US-Iran deal

Falling oil prices may remove a key headwind for emerging markets, but today's opportunity extends far beyond commodities.

Reports that the United States and Iran have reached a framework agreement that would reopen the Strait of Hormuz and extend the ceasefire have prompted a buying spree in equities and a fall to multi-month lows in the Brent Crude price. The framework reportedly includes provisions that would allow Iran to resume oil exports immediately, a development that could increase global supply and help explain the market's reaction.

While the situation remains fluid and details remain scarce, markets have reacted in a way that suggests a sustained reduction in energy market tensions could mean lower inflation and, in turn, support a rebound in global growth.

All this would be welcome news for Australian investors, but it may be even better news for emerging markets investors. This is because oil shocks have historically created challenges for many emerging market economies, a pattern that has repeated across multiple energy crises over recent decades.

Higher energy prices are rarely welcome news for countries that rely on imported oil. But focusing only on oil risks missing how much emerging markets have changed over the past decade.

Oil and the US dollar

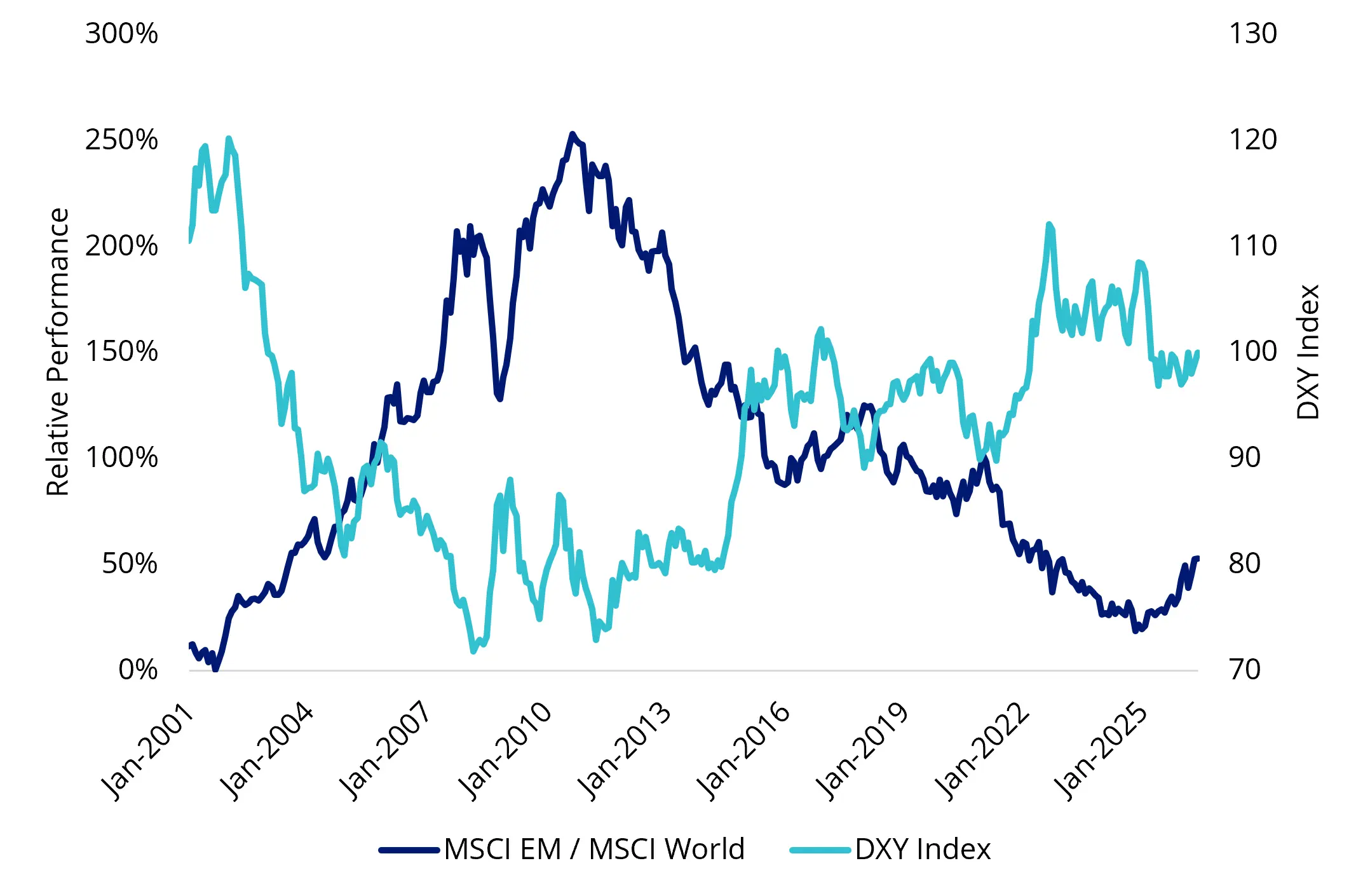

The US dollar is another reason emerging markets investors are paying attention. Historically, periods of US dollar weakness have often coincided with stronger relative performance from emerging markets. If oil prices continue to fall, investors may begin to focus on another important driver of emerging market returns: the US dollar.

Chart 1: US Dollar Index (DXY) versus MSCI Emerging Markets relative performance

Source: Bloomberg, VanEck. As at 16 June 2026. Past performance is not indicative of future performance. You cannot invest in an index.

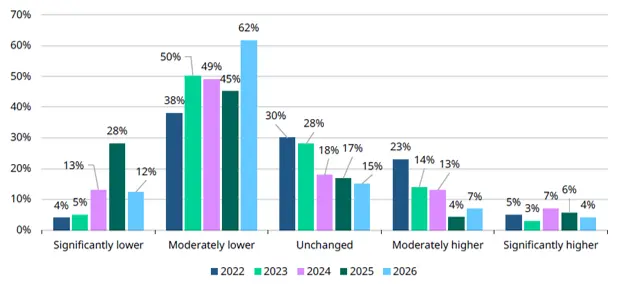

One sign of this is the growing expectation among central banks that the US dollar's share of global reserves will continue to fall. As the chart below shows, an increasing number of central banks expect the US dollar's share of global reserves to decline over the coming five years.

Chart 2: Expected US dollar share of global reserves in five years

Source: YouGov, World Gold Council

While reserve allocations are only one component of global capital flows, expectations of continued diversification suggest some investors are positioning for a world in which the US dollar's dominance becomes less pronounced. If that were to occur, it could provide an additional structural tailwind for emerging market equities.

Oil matters but it is no longer the whole story

Today's emerging markets look very different to the asset class many investors remember. Some of the world's most important technology, manufacturing and industrial companies are now listed in emerging markets, creating sources of growth that have little to do with commodity prices.

Taiwan, for instance, is home to several of the world's leading advanced semiconductor manufacturers. South Korea, classified by some as an emerging market, is a global leader in memory chips and electronics. India continues to benefit from favourable demographics and rising domestic consumption. Elsewhere, economies such as Thailand may benefit if energy costs continue to fall, while commodity producers such as Brazil continue to offer exposure to long-term demand for resources and industrialisation.

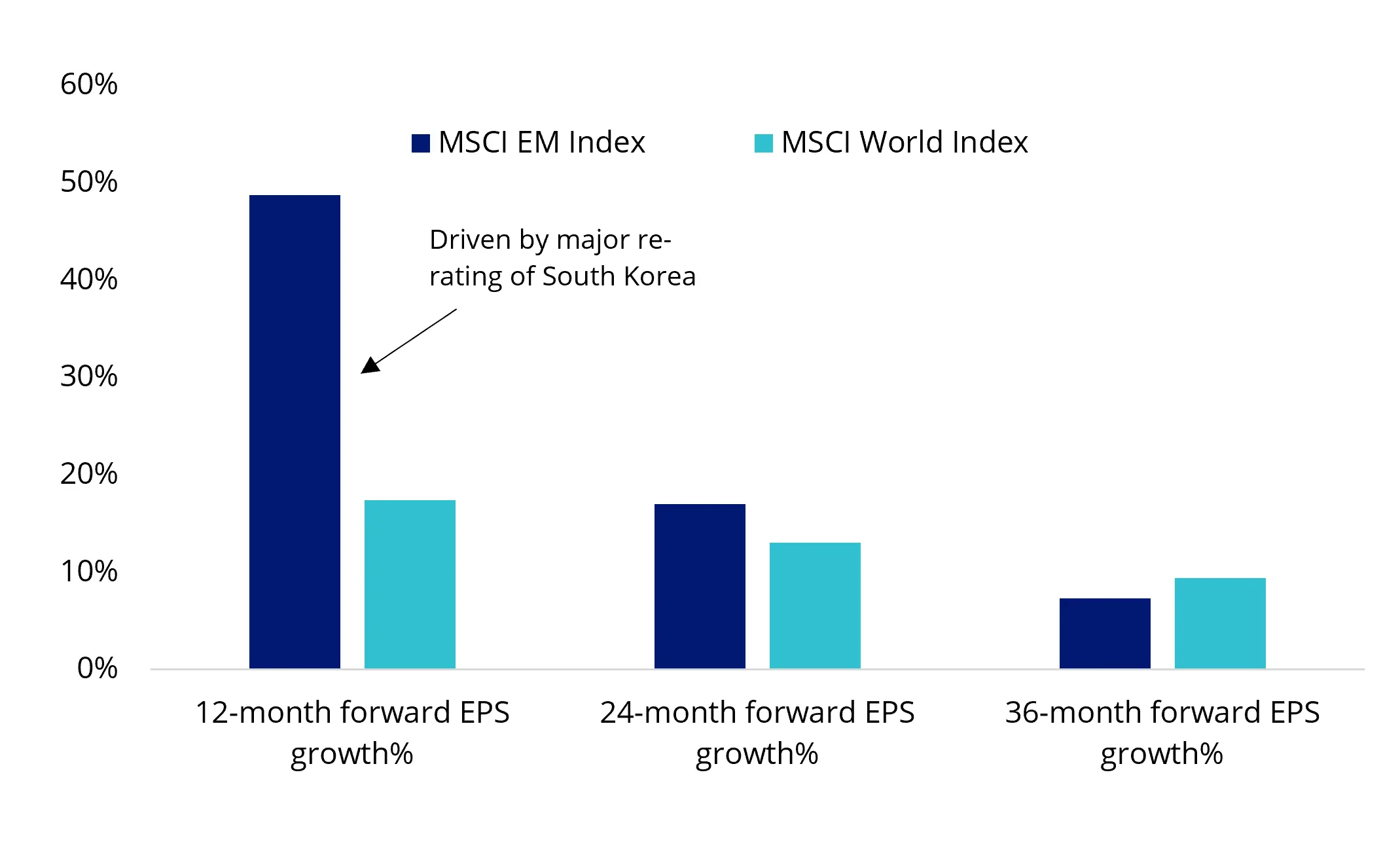

Put simply, emerging markets are not a monolithic trade. The outlook for emerging markets continues to be supported by stronger earnings growth than developed markets, suggesting the investment case extends beyond any single commodity cycle.

Chart 3: Growth outlook upbeat despite oil shock

Source: VanEck. Bloomberg. EPS data as of 3 June 2026. You cannot invest in an index.

Why EMKT is positioned differently

This diversity of opportunity is reflected in EMKT. Instead of trying to predict which country, sector or theme will outperform next, EMKT tracks the MSCI Emerging Markets Multi-Factor Select Index, which systematically selects companies based on four proven factors:

- Value;

- Momentum;

- Low Size; and

- Quality.

The objective is to maximise exposure to these factors while maintaining broad emerging markets diversification. Today, that process has led to significant exposure to companies such as Taiwan Semiconductor Manufacturing Company (TSMC), Samsung Electronics, SK Hynix and Kia Corporation, reflecting the growing importance of technology, advanced manufacturing and industrial development within emerging markets.

That approach has historically translated into strong outcomes for investors.

No longer just a commodities story

The recent decline in oil prices may remove one of the most important headwinds facing emerging market equities.

Yet the opportunity today extends beyond any single macroeconomic variable.

For investors, this distinction is important. The investment case for emerging markets no longer rests solely on commodities or the direction of oil prices. It rests on innovation, industrial capability, rising incomes and economic development across some of the world's fastest-growing economies. EMKT was designed to capture that opportunity.

Key points:

- EMKT provides investors with a diversified portfolio of emerging markets equities, included on the basis of:i. value;ii. low size;iii. momentum; andiv. quality.

- EMKT has demonstrated outperformance against the MSCI Emerging Markets Index since its inception, though, as we always note, this is by no means indicative of future performance.

- Access emerging markets equities for a significantly lower cost than comparable active management strategies at a management fee of 0.69% p.a.

- With one trade, EMKT currently provides access to 22 emerging market countries.

Key risks:

All investments carry risk. An investment in EMKT carries risks associated with ASX trading time differences, emerging markets, financial markets generally, individual company management, industry sectors, foreign currency, country or sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the PDS and TMD for details.

EMKT is likely to be appropriate for a consumer who is seeking capital growth, is intending to use the product as a core, minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.For large trade execution, please contact our capital markets desk on 02 8038 3317 or call me for more insight about how EMKT can assist in achieving your client’s investment outcomes.

Published: 23 June 2026

IMPORTANT NOTICE – FOR FINANCIAL SERVICES PROFESSIONALS ONLY. NOT TO BE DISTRIBUTED TO RETAIL INVESTORS.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.

EMKT is indexed to a MSCI index. EMKT is not sponsored, endorsed, or promoted by MSCI, and MSCI bears no liability with respect to EMKT or the MSCI Index. The PDS contains a more detailed description of the limited relationship MSCI has with VanEck and EMKT.

The rating issued July 2025 is published by Lonsec Research Pty Ltd ABN 11 151 658 561 AFSL 421 445 (Lonsec). Ratings are general advice only, and have been prepared without taking account of your objectives, financial situation or needs. Consider your personal circumstances, read the product disclosure statement and seek independent financial advice before investing. The rating is not a recommendation to purchase, sell or hold any product. Past performance information is not indicative of future performance. Ratings are subject to change without notice and Lonsec assumes no obligation to update. Lonsec uses objective criteria and receives a fee from the Fund Manager. Visit lonsec.com.au for ratings information and to access the full report. © 2026 Lonsec. All rights reserved.

The Zenith Investment Partners ("Zenith") Australian Financial Services License No. 226872 rating (assigned October 2025) referred to in this document is limited to "General Advice" (as defined by the Corporations Act 2001) for wholesale clients only. This advice has been prepared without taking into account the objectives, financial situation or needs of any individual. It is not a specific recommendation to purchase, sell or hold the relevant product. Investors should seek independent financial advice before making an investment decision and should consider the appropriateness of this advice in light of their own objectives, financial situation and needs. Investors should obtain a copy of, and consider the PDS or offer document before making any decision and refer to the full Zenith Product Assessment available on the Zenith website. Zenith usually charges the product issuer, fund manager or a related party to conduct Product Assessments. Full details regarding Zenith's methodology, ratings definitions and regulatory compliance are available on our Product Assessment's and at http://www.zenithpartners.com.au/RegulatoryGuidelines