Duration consideration

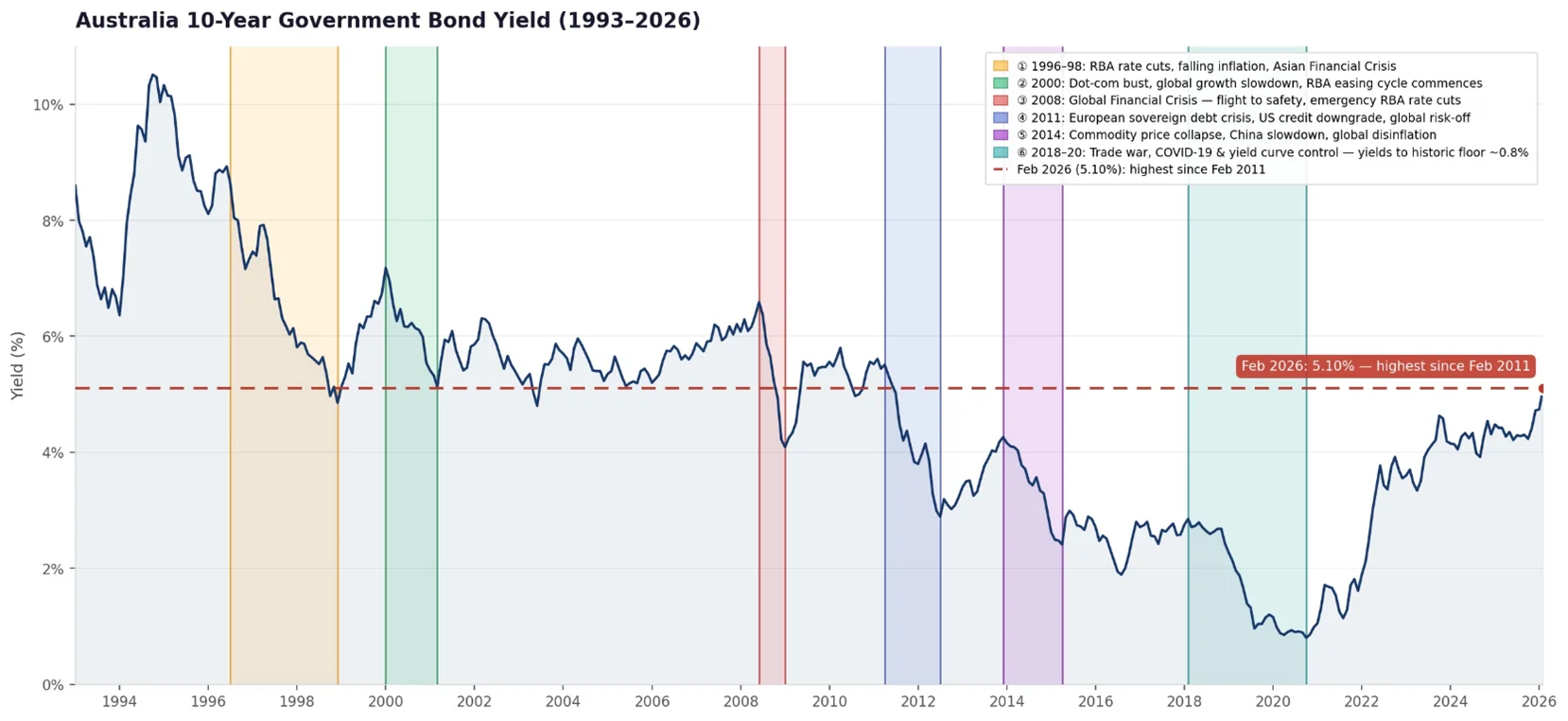

The Australian 10-year government bond yield has surged to a 15-year high.

The rise in yields has resulted in a fall in the price of fixed rate bonds.

Should RBA rate-hike expectations cool (currently estimated to be three more rate rises this year), or growth concerns come to the fore, yields could fall, and bond prices could rise.

Many savvy investors are considering adding duration to potentially take advantage of these higher yields.

The Australian 10-year government bond yield has surged to 5.04%, reaching a 15 year high. The move reflects mounting inflation concerns and rising expectations of future RBA rate hikes, following the oil price spike amid escalating Middle East tensions.

While recent hikes are justifiable, we believe markets may have gotten ahead of themselves by pricing in three more rate hikes by the end of the year. In our view, that outlook assumes oil prices remain higher for an extended period, which may not materialise.

Oil shocks linked to geopolitical events, in the past, have typically been temporary and often have the opposite effect on inflation as they lead to reduced commercial activity. Australian consumers are already feeling the impact at the petrol pump, and sentiment has deteriorated.

In such an environment, the risk is not runaway inflation but a slowdown in demand. We think this limits how far the RBA can push rates higher this cycle.

This realisation could see bond yields start to grind lower, thus the current long-term yields could be a compelling entry point for bond investors.

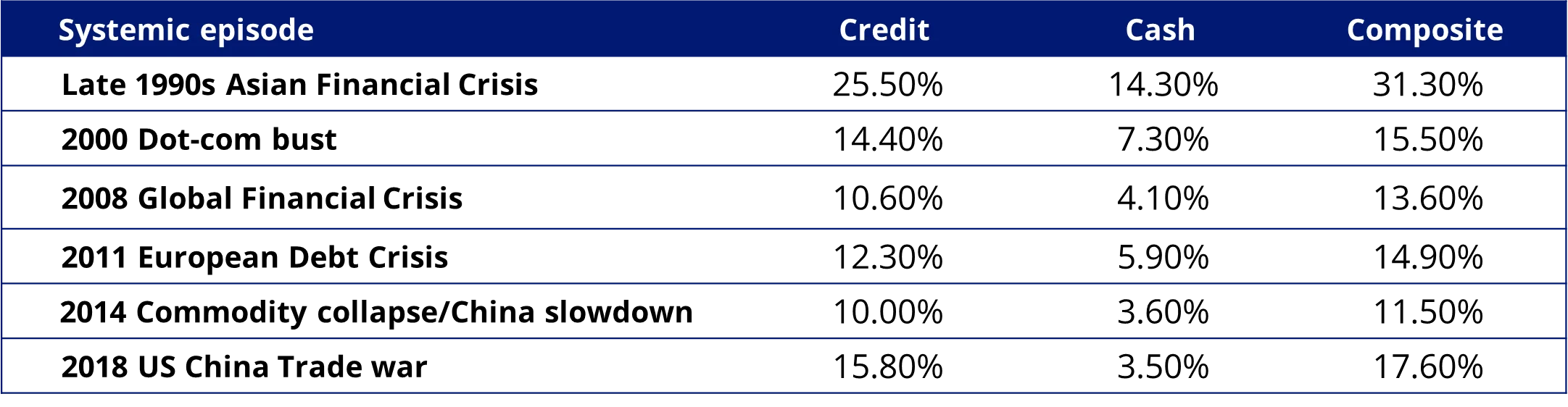

Additionally, if the conflict sparks a global systemic episode and economic growth concerns become front of mind, the Australian 10-year government bond yield could fall, as it did in past episodes. This includes the late 1990’s Asian Financial Crisis, the Dot-com bubble, the Global Financial Crisis, the European Debt Crisis, 2014's commodity price collapse/China slowdown and 2018's US and China Trade War.

Source: Bloomberg, VanEck.

During these periods, cash and fixed rate government and corporate bonds performed well despite credit spreads expanding.

Source: Bloomberg. Credit as Bloomberg AusBond Composite; Cash as Bank Bill Index; Composite as Ausbond Composite Index. Past performance is not indicative of future performance. Late 1990s Asian Financial Crisis: 31 Jul 1996 to 31 Dec 1998, 2000 Dot-com bust: 31 Jan 2000 to 31 Mar 2001, 2008 Global Financial Crisis: 30 Jun 2008 to 31 Jan 2009, 2011 European Debt Crisis: 30 Apr 2011 to 31 Jul 2012, 2014 Commodity collapse/China slowdown: 31 Dec 2013 to 30 Apr 2015, 2018 US China Trade war: 28 Feb 2018 to 31 Oct 2020.

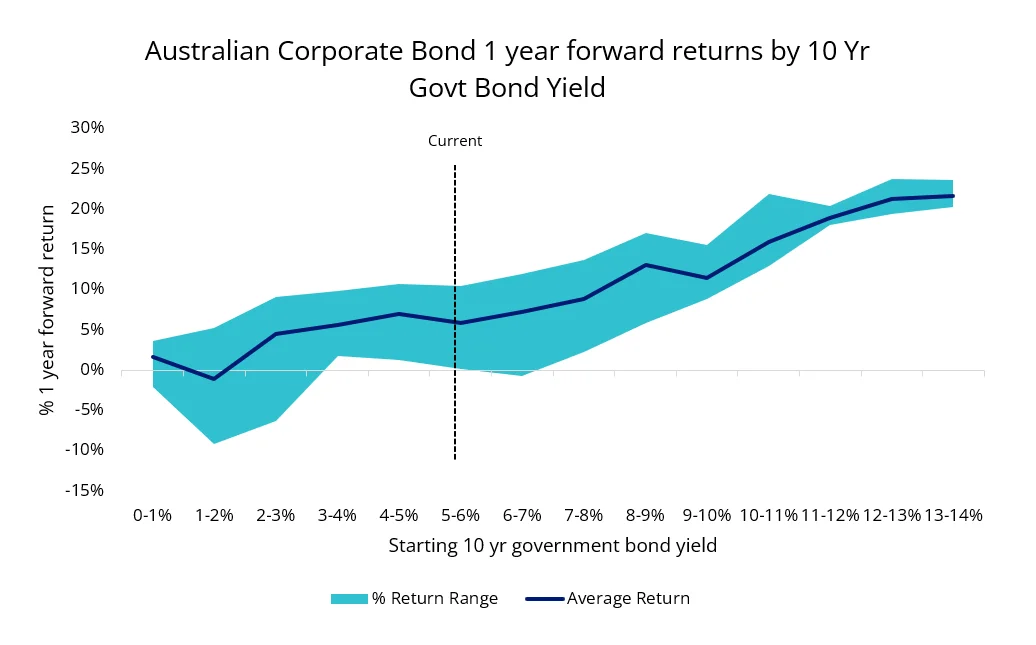

Higher yields have also improved the return-risk profile of fixed rate bonds. The chart below illustrates the estimated 1-year forward returns range of Australian fixed rate corporate bonds at various starting 10-year government bond yields. The key takeaway is a higher yield, increases the average return.

Source: Bloomberg, VanEck, Bloomberg AusBond Corporate Index. 30 September 1989 to 28 February 2026.

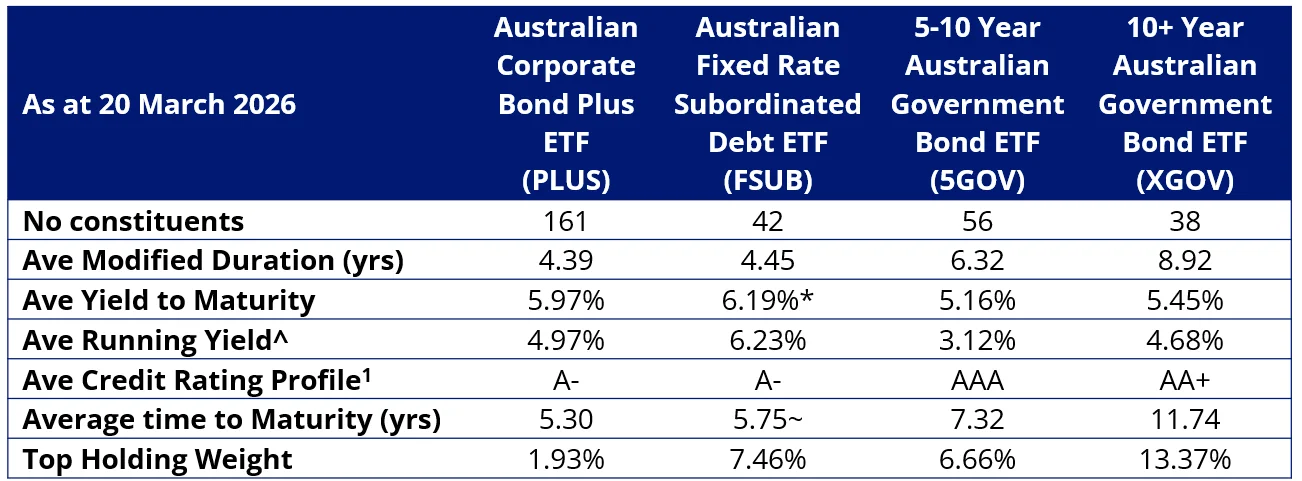

Accessing fixed rate bonds

VanEck offers four Australian fixed rate bond ETFs. Notably, our Australian Fixed Rate Subordinated Debt ETF (FSUB) is currently yielding above 6%.

VanEck Fixed Rate ETF metrics

Source: VanEck. *yield to worst; ~time to next call; ^yield measures are not Indicative of future dividend income from the funds.1Average credit rating is calculated taking the weighted average Bloomberg composite bond rating. If a bond issued by a national government is unrated, the Bloomberg issuer composite rating will be used. If no rating is available, the security will be not rated and excluded from the calculation.

Key risks: An investment in the ETFs carry risks associated with: interest rate movements, bond markets generally, subordinated debt (FSUB), issuer default, credit ratings, country and issuer concentration, liquidity, tracking an index and fund operations. See the PDS for more details.

Published: 30 March 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (‘VanEck’) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) listed on the ASX. This is general advice only and does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.