Optimism: The market's greatest force multiplier

The “will they or won’t they” between the US and Iran has been the focus of markets this past quarter. So far, there have been as many promising starts as disheartening setbacks.

The market has optimistically reacted to each promising sign, it seems, with greater scale than a setback, if the setback was noted at all. Credit spreads continued to grind tighter, and while private credit remains an area of concern, high yield and corporate spreads are nearing all-time tights.

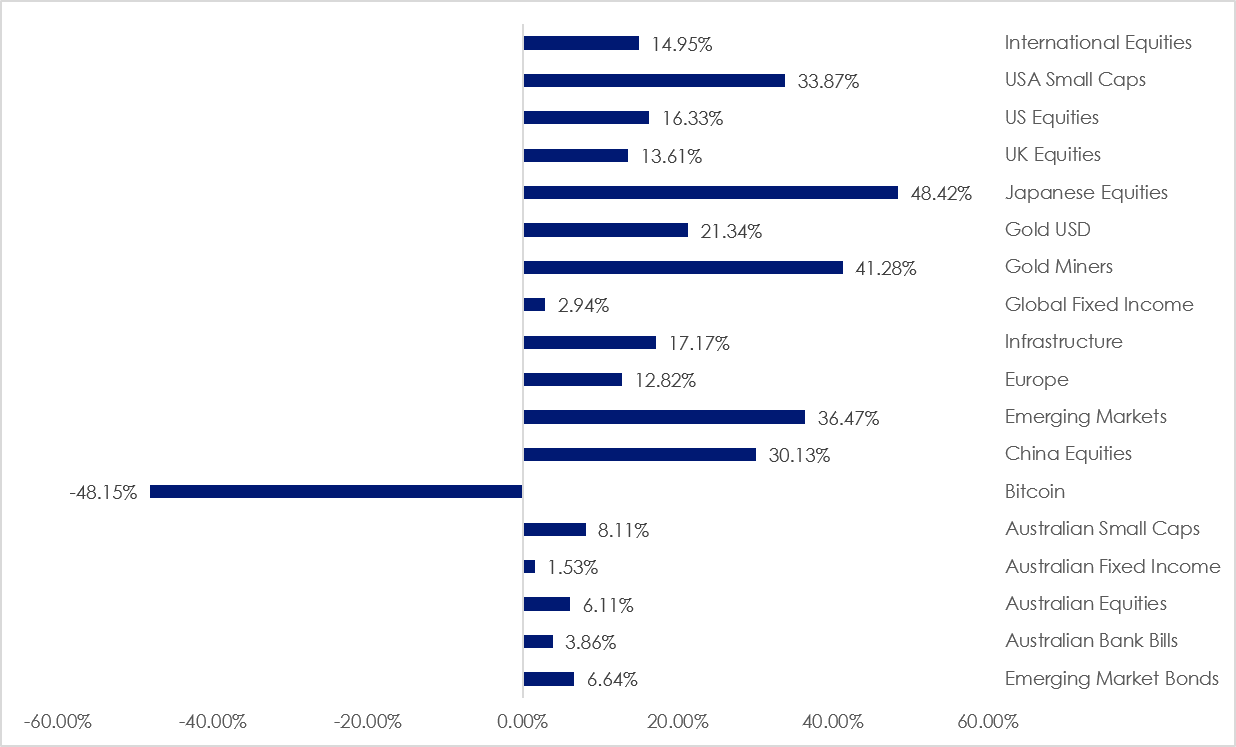

Over the quarter, many equity markets, including the US, hit record highs. Only emerging markets and Japanese equities outperformed US small- and large-cap equities over the quarter. From a sector perspective, internationally, IT, driven by semiconductors, has been the standout performer, followed by sectors traditionally associated with the value complex, financials and industrials. Locally, consumer discretionary rallied, while the local listed real estate sector benefited from a fall in long-end yields.

Investors, to use a baseball analogy, wonder, are we in the seventh inning, or the ninth? In other words, will the optimism continue or are we nearing the end of the cycle?

We think value could remain the go-to international equity market exposure, though, should market participants start to (finally) worry about low growth, the quality complex could rise back to the surface and come back into favour.

Locally, monetary and fiscal policy have been weighing on investor sentiment. Fiscal policy remains loose, with deficits forecast as far as the eye can see according to May’s Federal budget, which also included a shift in the tax regime that is expected to have implications for investors. The RBA, while holding at its most recent meeting, retains its tightening bias. According to its most recent statement, it remains ready to fight inflation, which remains above trend.

The Fed is also maintaining a hawkish stance, not that you would know what the new Fed Chair, Kevin Warsh, predicts, as he did not provide a dot on the dot plot, though he encouraged his committee colleagues to do so. It was the first time, since the Fed first published dot plots in 2012, that a Fed Chair had withheld their forecast.

This creates uncertainty. Combined with the geopolitical stops and starts, inflation, posturing and tariffs, it makes for an unpredictable future. Markets traditionally don’t like uncertainty, but, as we have pointed out in previous ViewPoints:

“Uncertainty actually is the friend of the buyer of long-term values.” Warren Buffett

Mainstream asset class returns for FY26

Source: 1 July 2025 to 30 June 2026, returns in Australian dollars. Gold Miners is NYSE Arca Gold Miners Index, US Equities is S&P 500 Index, International Equities is MSCI World ex Australia Index, European Equities is MSCI Europe Index, UK Equities is FTSE 100 Index, Australian Equities is S&P/ASX 200 Accumulation Index, Australian Small Caps is S&P/ASX Small Ordinaries Index, Gold is Gold Spot US$/oz, US Small Caps is Russell 2000 Index, China Equities is CSI 300 Index, Global Fixed Income is Bloomberg Global Aggregate Bond Hedged AUD Index, Australian Bank Bills is Bloomberg AusBond Bank Bill Index, Australian Fixed Income is Bloomberg AusBond Composite 0+ yrs Index, EM Fixed Income is 50% J.P. Morgan Emerging Market Bond Index Global Diversified Hedged AUD and 50% J.P. Morgan Government Bond-Emerging Market Index Global Diversified, EM Equities is MSCI Emerging Markets Index, Japanese Equities is Nikkei 225 Index. Global Listed Infrastructure is FTSE Developed Core Infrastructure 50/50 Hedged into Australian Dollars Index, Bitcoin is The MarketVector™ Bitcoin Benchmark Rate. Past performance is not indicative of future performance.

The seventh inning, the ninth, or is it nirvana?

Of all the moving pieces in the global investment environment, the outlook is increasingly dependent on just one: the outlook for AI.

Traditional macro appears to have taken a back-seat. The world has seemingly shrugged off the ongoing inflation effects and growth drag of the Iran conflict, or it could be that maybe markets are bored with on-again, off-again peace processes and have given up.

Visibility on the outcome of the conflict and what has been agreed remains cloudy.

But a whopping swing in US monetary policy expectations has likewise seen a smallish, rather optimistic reaction. At least, after four years of inflation persistently diverging (upwards) from target, rate expectations now accord with actual textbook policy prescriptions, noting some caveats shared below.

At the start of the year, the market was pricing in between two and three rate cuts in 2026. It is, at the time of writing, pricing in what consensus believes to be more responsible, one and a half rate rises.

But other imponderables remain, including:

- gathering debt loads;

- trade and fiscal imbalances; and

- illiquid, non-transparent investment sectors.

But the biggest of them all is the burgeoning AI sector and its ability to sustain, and then repay, its enormous, ever-growing capital appetite.

The question is whether AI can profitably repay its bets over the near-to-medium term. That would be a gargantuan task.

So, this naturally leads to the question: Is it time to hop off yet? Is it the seventh inning or the ninth? Maybe Baron Rothschild gets the last word: “I never buy at the bottom and I always sell too soon”.

You can read more about this subject in the latest edition of VanEck Viewpoint. Click here to download the PDF.

Published: 06 July 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.