Why outstanding results won’t come from the same old playbook

The Australian share market has offered investors little to cheer in 2026, falling at the index level while other equity markets such as the S&P 500 continue to reach new highs.

While some sectors have held up, much of the market faces a difficult backdrop: households are adjusting to higher borrowing costs, inflation remains persistent, confidence is weak and geopolitical tensions remain in focus. For many investors, this market has become harder to navigate. But rather than a temporary frustration, we think it reflects a broader shift in the investment environment – one where investors may need to think differently about where returns come from.

It’s (still) hot in Australia

The Australian economy has been far more resilient for longer than many first expected.

Bar a small dip in 2025, inflation has been a persistent thorn in the RBA’s side for most of the 2020s.

The drivers of this growth also matter. A tight labour market, elevated migration (causing greater imbalance in the housing market) and rising price pressures for services are all reasons for why inflation has been so stubborn. But in recent years, activity has also been supported more by government spending than by a sustained lift in private sector demand. In contrast, business investment has been subdued and productivity growth has struggled to keep pace with global peers.

Chart 1: Government consumption (% GDP)

Source: Morgan Stanley Research, data as at 30 September 2025 due to data availability.

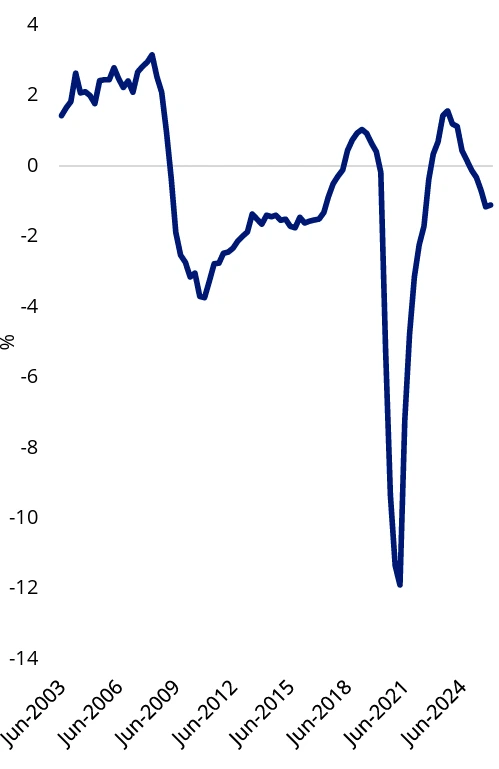

Chart 2: Australia budget balance (% GDP)

Source: Bloomberg, Data as at 31 December 2025 due to data availability.

This leaves the Reserve Bank with a difficult task. Interest rates need to remain elevated to contain inflation, even as higher borrowing costs weigh on households and businesses. That pressure is already visible. Consumers are still spending, but often more carefully than before. Historically, this combination has tended to coincide with a more fragile growth environment.

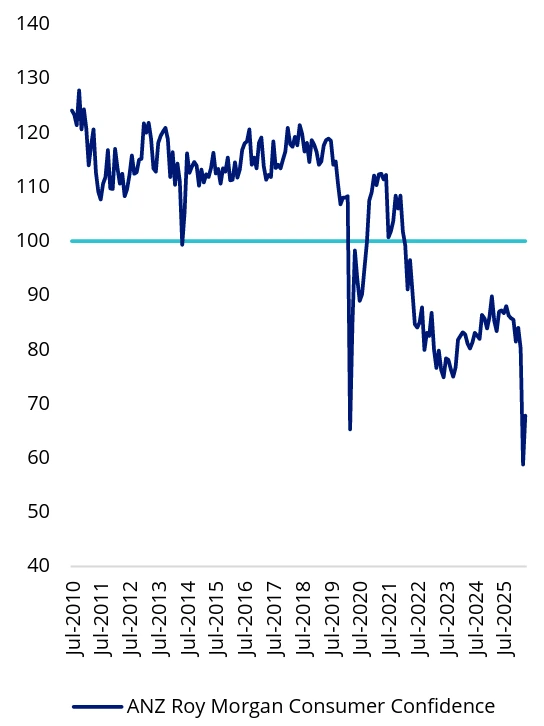

Chart 3: Consumer Confidence index

Source: Bloomberg, VanEck. Westpac-Melbourne Institute Consumer Confidence Index. Data as at 30 April 2026 due to data availability.

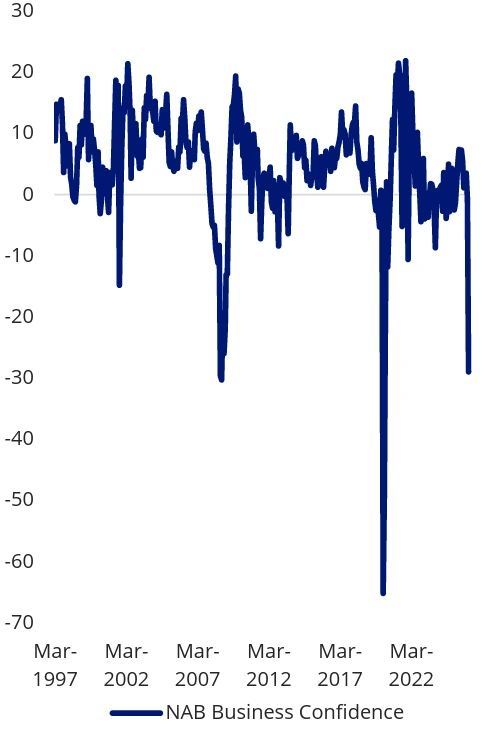

Chart 4: Business Confidence Index (percentage balance)

Source: Bloomberg, VanEck. NAB Business Confidence and Business Conditions indices. Data as at 30 March 2026 due to data availability.

The recent February reporting season also offered a useful snapshot of how Australian companies are navigating this environment.

At a high level, more companies beat earnings expectations than missed them. But beneath the surface, businesses tied closely to household spending and lower interest rates were often punished heavily (especially when results disappointed). By contrast, sectors linked more closely to the real economy, such as materials and utilities, proved more resilient as investors favoured companies with stronger pricing power and less sensitivity to borrowing costs. Mid-sized companies also stood out, delivering some of the strongest earnings surprises and upgrades across the market.

The geopolitical wild card

Geopolitical events often create the kind of volatility that tests investor patience. The conflict in the Middle East has added another layer of uncertainty for investors. The region is central to global energy supply, and any prolonged disruption could keep oil prices elevated for longer, reinforcing inflation pressures at a time when central banks are still trying to contain them.

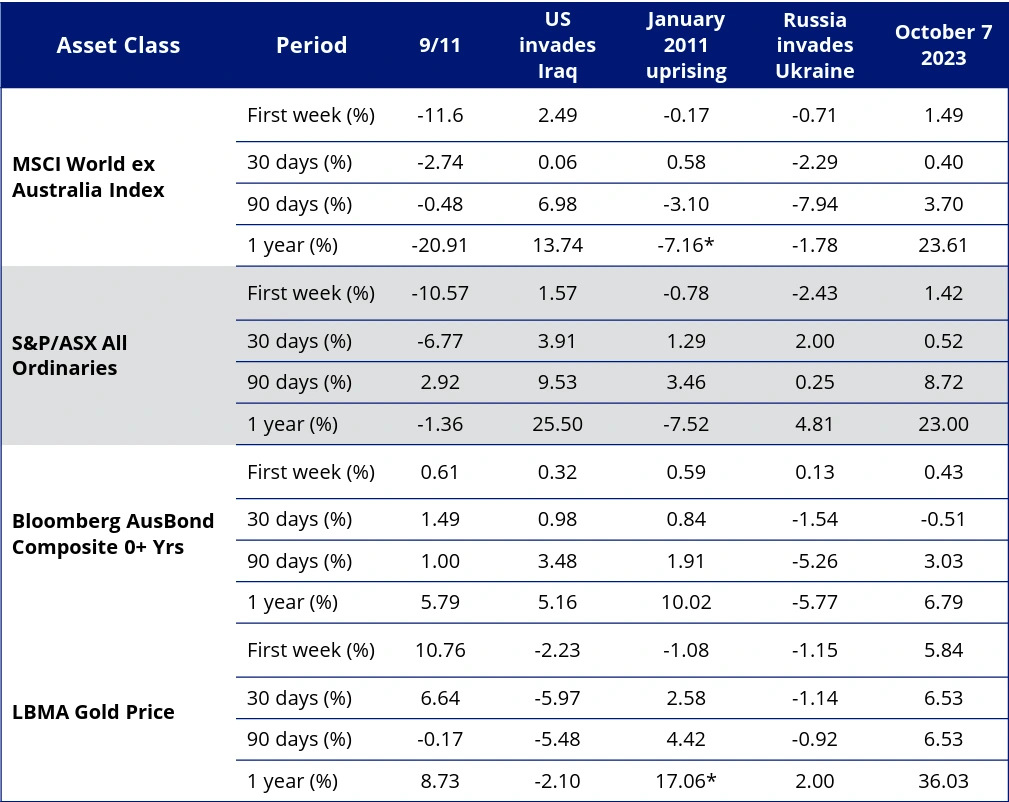

History suggests geopolitical shocks can move markets sharply in the short term, but the long-term impact varies by event and market. Australian shares fell heavily after events such as 9/11, yet in several other geopolitical crises the market recovered strongly in the months that followed.

Table 1: Performance impact of major geopolitical events since 2000

Source: VanEck, Morningstar *captures the period of the European debt crisis. You cannot invest in an index. Past performance is not indicative of future performance.

The above table also demonstrates that individual investors cannot and should not attempt to time geopolitical events alongside their investment strategy. Rather, it pays to stay invested through the volatility and acknowledge that during times of geopolitical shock, owning portfolio diversifiers like gold can be valuable. Investors who have not already added a gold allocation could consider VanEck Gold Bullion ETF (ASX: NUGG) for Australian-sourced bullion exposure or VanEck Gold Miners ETF (ASX: GDX) for a global gold miners approach.

Investor implications

For investors, the message is becoming clearer. The economic backdrop is likely to remain uneven for some time, meaning this is no longer a market where simply owning the index will guarantee strong results. In this environment, where investors look for returns will matter more than simply remaining invested.

We are cautious on sectors where valuations remain elevated, and earnings appear more vulnerable to structural disruption or weaker consumer spending. The conditions that supported years of bank-led market leadership are beginning to change, and we may be seeing the early stages of a broader shift in how the Australian market rewards investors.

By contrast, parts of the materials sector appear better positioned. Several favourable industry trends are beginning to align with improving company fundamentals, while the sector has historically performed well during periods of higher inflation and rising interest rates. Investors seeking targeted exposure to Australian materials companies may consider VanEck Australian Resources ETF (ASX: MVR).

We also see opportunities among select businesses with strong pricing power and durable market positions. More broadly, however, the Australian share market remains heavily concentrated in financials and materials when weighted by company size. For investors seeking broader diversification, an equal-weight approach such as VanEck Australian Equal Weight ETF (ASX: MVW) may offer a more balanced way to access the market. Historically, equal-weight strategies have also performed well during previous interest-rate hiking cycles.

Read more in the VanEck Portfolio Compass: Australian Equities Outlook 2026 here.

Key risks

An investment in NUGG or GDX carries investment risk. These risks vary depending on the fund and may include gold pricing risk, currency risk, custody risk, Australian sourced gold bullion risk, ASX trading time differences, financial markets generally, individual company management, industry sectors, country or sector concentration, political, regulatory and tax risks, fund operations and tracking an index. See the PDSs and TMDs for details on risks.

An investment in MVW or MVR carries risks associated with: financial markets generally, individual company management, industry sectors, stock and sector concentration, fund operations and tracking an index. See the PDSs and TMDs for details.

NUGG is likely to be appropriate for a consumer who is seeking capital growth, is intending to use the product as a minor or satellite allocation within a portfolio, has no investment timeframe, and has a high or very high risk/return profile.

GDX is likely to be appropriate for a consumer who is seeking capital growth, is intending to use the product as a minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a very high risk/return profile.

MVW is likely to be appropriate for a consumer who is seeking capital growth and a regular income distribution, is intending to use the product as a core, minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

MVR is likely to be appropriate for a consumer who is seeking capital growth and a regular income distribution, is intending to use the product as a minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

Published: 22 May 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.