Don’t go chasing waterfalls (or choppy yields)

"Don't go chasing waterfalls. Please stick to the rivers and the lakes that you're used to."

At first glance, the TLC song Waterfalls has nothing in common with income investing. But more than three decades after its release, the song may indeed contain a lesson that many investors would benefit from remembering.

Every market cycle seems to produce its own waterfall. A new income opportunity catches investors' attention because it starts paying more than everything else. Headlines focus on yields that look impossible to ignore – be it high yield bonds, private credit or REITs.

In these moments, investors proceed to ask the same question: why settle for 4% when something else is offering 8%? While it's a fair question, it may not be the right one.

The challenge for income investors has never been finding yield. Investors will always find opportunities offering more income. The challenge is understanding why that income exists, whether it is sustainable and whether it will still be there when they need it most.

The temptation of the tallest waterfall

Yield has an undeniable appeal – especially in a market like Australia. It is one of the few investment metrics that can be compared briefly, which helps explain why investors often gravitate towards it. Faced with two income opportunities, most people will naturally pay more attention to the one offering the larger payout.

But a higher yield can sometimes reflect risks that investors may not immediately appreciate. Credit risk is one example. An outsized yield may be compensation for lower liquidity, greater complexity or exposure to a less familiar part of the market. In that sense, yield is often treated as a verdict when it is just a clue.

That is particularly relevant today, when investors can access income from a far broader range of sources than in the past. Government bonds, floating-rate securities, corporate credit, mortgage-backed securities, subordinated debt, private credit and capital securities can all generate attractive income, but they do so for different reasons and with different risk-return characteristics.

Income is about more than a number

For investors who rely on portfolio income, the experience of receiving that income can matter almost as much as the amount itself.

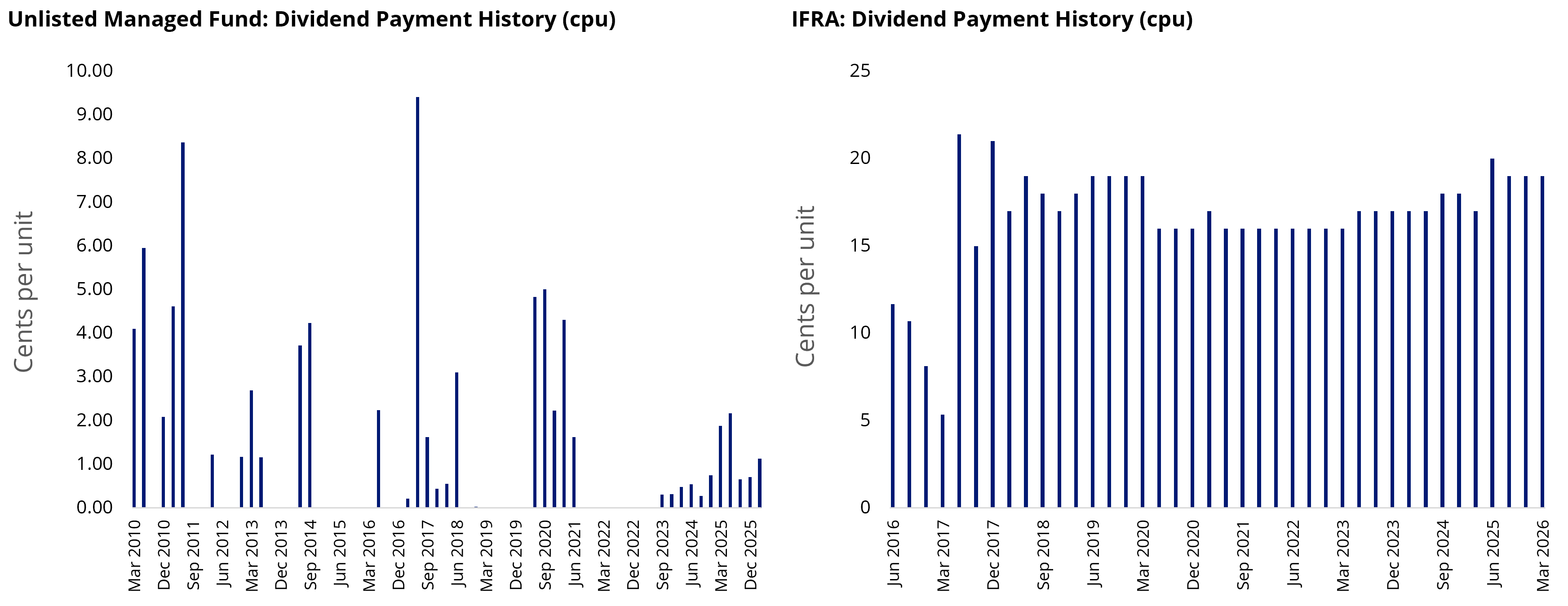

Consider the two distribution histories shown in Chart 1. The investment on the left occasionally delivers eye-catching income payments, but they are irregular and difficult to predict. The investment on the right rarely produces the same headline-grabbing spikes, yet it has delivered a far more consistent stream of income over time.

Chart 1 and 2: The difference between variable and consistent income streams

[LHS] Source: Fund Manager website accessed 3 June 2026. Past performance is not a reliable indicator of future performance. [RHS] Source: VanEck. IFRA inception date is 29 April 2016. Past performance is not a reliable indicator of future performance. IFRA dividend payment history (cpu) is not a guarantee of future dividends payable from IFRA.

For retirees, self-funded investors and anyone relying on portfolio income to help meet ongoing expenses, consistency can have value of its own. A smoother income stream can make budgeting easier, provide greater confidence when planning future spending and reduce the temptation to react to short-term changes in distributions.

This is why experienced income investors tend to look beyond the headline yield. The amount of income matters, but so does its reliability.

Not all income behaves the same way

One of the biggest misconceptions about income investing is that income is a single asset class. Different sources of income respond differently to changes in interest rates, economic growth and market conditions. Understanding those differences can help investors build more resilient portfolios and avoid becoming overly reliant on a single source of cash flow.

|

Income source |

Potential advantages |

Often performs best when... |

Potential trade-offs |

|

Government bonds |

Historically defensive; can provide diversification during periods of economic stress |

Economic growth slows, risk appetite falls or interest rates decline |

Typically offer lower yields than other income assets |

|

Corporate bonds |

Additional yield potential and exposure to company earnings power |

Economic conditions are stable and corporate fundamentals remain healthy |

Greater sensitivity to credit conditions |

|

Floating-rate securities |

Income can rise as interest rates increase; typically lower interest-rate sensitivity |

Interest rates are rising or expected to remain elevated |

Income may decline when rates fall |

|

Subordinated debt & capital securities |

Higher income potential and access to different parts of the capital structure |

Investors are comfortable taking additional credit risk for potentially higher income |

Greater complexity and higher risk than senior debt |

|

Mortgage-backed securities |

Diversified exposure to pools of residential mortgages |

Housing markets remain resilient and credit conditions are supportive |

Sensitive to housing and credit market dynamics |

|

Private credit |

Attractive income potential and lower correlation with public markets |

Investors are seeking enhanced income and can tolerate less liquidity |

Reduced liquidity and less frequent pricing transparency |

|

Global credit opportunities |

Access to a broader opportunity set across regions and sectors |

Relative value opportunities exist outside domestic markets |

Additional currency, market and economic risks |

For educational purposes only.

Fixed versus floating: two tools, two different jobs

While both can play an important role in an income portfolio, they are designed to solve different problems.

Fixed-rate securities provide certainty. Investors know what income they are likely to receive, which can be attractive when rates are expected to fall or when predictable cash flows are a priority. Floating-rate securities are built for a different environment. Because their income payments reset periodically, they can adapt more readily when interest rates move higher.

Neither approach is inherently superior. Rather, they reflect one of the central themes of income investing: different market conditions call for different tools. The challenge is not finding the "best" income source but understanding which one is best suited to the environment and the role it needs to play within a portfolio.

Building income that keeps flowing

Today's investors have access to a far broader range of income opportunities than previous generations. Within VanEck Australia's income range alone, investors can access everything from defensive government bonds and corporate credit to floating-rate securities, subordinated debt, mortgage-backed securities, capital securities, private credit and global income strategies.

Each serves a different purpose. Government bond ETFs such as 1GOV, 5GOV and XGOV can help provide core stability during periods of uncertainty. Floating-rate exposures such as FLOT may appeal to investors seeking income that can adapt as interest rates change, while corporate bond strategies such as PLUS can provide access to a broader range of income opportunities. Investors seeking specialist exposures can also access areas such as subordinated debt, mortgage-backed securities, capital securities, private credit and global income strategies.

The objective is not to predict which income source will perform best next year. It is to build a portfolio capable of generating sustainable income through a wide range of market conditions. Because in the end, the goal is not to find the tallest waterfall. It's to find one that keeps flowing consistently.

Key risks

An investment in the VanEck Australian Floating Rate ETF (FLOT), VanEck 1-5 Year Australian Government Bond ETF (1GOV), VanEck 5-10 Year Australian Government Bond ETF (5GOV), VanEck 10+ Year Australian Government Bond ETF (XGOV) and VanEck Australian Corporate Bond Plus ETF (PLUS) carries risks associated with bond markets generally, interest rate movements, issuer default, credit ratings, liquidity, fund operations and tracking an index. Certain funds may also be exposed to country and issuer concentration risk. See the relevant PDS and TMD for each fund for more details.

Published: 04 June 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.