When the chill sets in

The reward for taking risk has thinned. What does that mean for investors who have spent the past decade relying on broad market exposure?

Sydney experienced its first properly cold winter morning this week. While it’s not freezing by global (or even Hobart’s) standards, it’s certainly cold enough to change behaviour. The puffer jackets and trench coats appeared right on cue as workers commuted into town, while queues at city coffee shops were a little longer than usual.

The funny thing about winter is that it rarely arrives as a surprise. The calendar gives plenty of warning. Yet the first genuinely cold morning still feels different because it marks the moment the season stops being theoretical. People are no longer preparing for winter. They are living in it.

Markets occasionally experience something similar.

For much of the past 15 years, investors operated in a remarkably forgiving season. Through European debt scares, trade wars and a once-in-a-century pandemic, the investment conclusion remained remarkably similar. With cash paying next to nothing and government bonds offering little yield, stocks became the obvious destination for anyone seeking real returns. But now, the season may be changing.

For much of the past decade, investors were rewarded for simply investing and staying invested. But the next decade may prove different – rewarding intention and selectivity. The chart below suggests investors are receiving less compensation for taking equity risk than they have for much of the past two decades.

Chart 1: Australian and US Equity Risk Premia since 2000

Source: Bloomberg, VanEck. As at 29 May 2026, the most recent data available for S&P 500 ERP data. Past performance is not an indicator of future performance. You cannot invest directly in an index.

Why has the equity risk premium fallen?

The equity risk premium (ERP) is simply the difference between the return investors expect from shares and the return available on government bonds. The smaller the gap, the less compensation investors receive for taking equity risk.

Much of the recent decline reflects a world of higher interest rates. As bond yields have risen sharply, government bonds once again offer a meaningful return. At the same time, equity markets have remained resilient. The result is a narrower gap between expected equity returns and bond yields.

Why starting conditions matter

A declining ERP does not necessarily mean investors should take less risk. Markets can remain expensive for longer than expected, and periods of low risk premia have not always led to poor returns.

What it may signal is a shift in the backdrop that investors have become accustomed to.

A lower ERP means there may be less room for error if those assumptions prove wrong. When the reward for taking risk becomes less generous, the differences between sources of risk can start to matter more. Investors may be less able to rely on favourable market conditions to rescue poor diversification, excessive concentration or an expensive portfolio.

Figure 1: How equity risk premia affect returns (all else being equal)

For illustrative purposes only.

In that sense, a low ERP is perhaps less a warning about markets and more a reminder about portfolio construction. A chilly winter’s day would not stop someone leaving their house – but it should change what they wear. Likewise, a lower reward for taking risk does not mean investors should abandon equities. It shifts the focus away from whether investors should own them and towards how they own them.

Not all stocks are created equal

Investors often talk about equities as though they are a single source of return. They aren't. An investor owning a concentrated portfolio of large US growth companies is taking a very different set of risks to someone owning emerging markets, just as a quality investor is taking different risks to a value investor.

The distinction did not always matter. A generous equity risk premium can mask a multitude of sins. A thin one cannot.

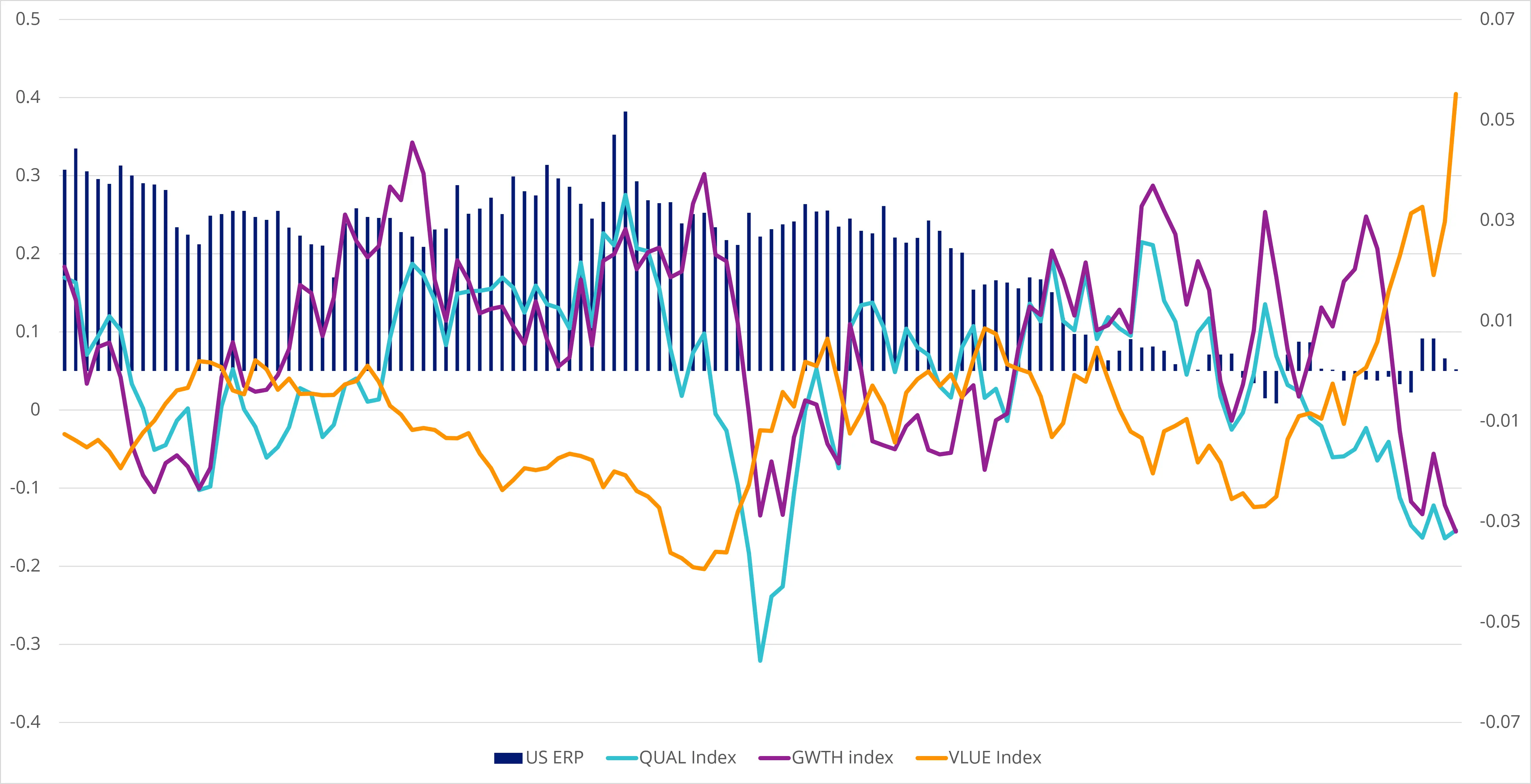

The chart below shows how different investment styles have behaved as the reward for taking risk has become more scarce. While no single approach consistently outperformed, outcomes diverged significantly, increasing the importance of portfolio construction.

Chart 2: Performance of different investment strategies during different ERP regimes, 31 January 2016 to 29 May 2026

Source: Bloomberg, VanEck. As at 29 May 2026. QUAL Index is MSCI World ex Australia Quality Index. VLUE Index is MSCI World ex Australia Enhanced Value Top 250 Select Index. GWTH Index is MSCI World ex Australia Growth Select Index. Past performance is not an indicator of future performance. You cannot invest directly in an index.

Of course, the equity risk premium is only one lens through which to view markets. No single metric can determine which investment style will outperform. What the equity risk premium can do is provide a useful indication of how generously investors are being compensated for taking risk.

Different approaches produced different outcomes

Some investors respond by focusing on valuation. Value investing begins with a simple premise: the price you pay matters. As future returns become harder won, investors often become more discerning about what they are willing to pay for growth – a dynamic that may help explain the recent resurgence of value strategies. Investors seeking a systematic approach to value may wish to consider the VanEck MSCI International Value ETF (ASX: VLUE).

Growth investors apply a different lens. Rather than focusing on what is cheap today, they focus on companies capable of delivering strong earnings growth tomorrow. When those expectations are met, growth can continue to reward investors handsomely. Investors seeking exposure to companies with strong growth characteristics may wish to consider the VanEck MSCI International Growth ETF (ASX: GWTH).

Quality investors take a different path. If future returns are likely to be scarcer, then the durability of earnings and strength of balance sheets become increasingly important. Put simply, when investors have less room for error, they tend to place a higher value on certainty. Investors can access the highest quality stocks in the world through the VanEck MSCI International Quality ETF (ASX: QUAL).

The common thread is not that one approach is always superior. Different market environments have rewarded different investment styles. The first cold morning of winter does not tell us whether we will need a raincoat or a puffer jacket next week. It simply reminds us that conditions have changed.

Portfolios face a similar challenge

If the ERP is anything to go by, future success will depend less on taking any risk and more on being deliberate about which risks are worth taking.

Investors may find themselves looking for returns from a broader range of sources. That could mean looking beyond the dominant parts of the equity market towards value, quality, equal-weight or emerging market exposures. It could also mean complementing equities with asset classes such as fixed income, gold or private assets. The objective is not to predict the next winner, but to avoid relying on a single source of return.

For much of the past 15 years, investors were encouraged to ask one question: "How much equity exposure should I have?"

A lower ERP may encourage a different one: "Where exactly are my returns coming from?"

Key risks

An investment in the fund carries risks associated with: financial markets generally, individual company management, industry sectors, ASX trading time differences, foreign currency, sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the PDS and TMD for details.

GWTH, VLUE and QUAL are likely to be appropriate for a consumer who is seeking capital growth, is intending to use the product as a major, core, minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

Published: 04 June 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.