Why the timing of SpaceX, OpenAI and Anthropic’s IPOs should make investors pause

While the SpaceX IPO has made history for its size, valuation and extraordinary demand, the most interesting aspect of the listing may be its timing.

For more than a decade, the world's most successful private companies have had little reason to enter public markets. Venture capital, private equity and sovereign wealth funds provided abundant funding, allowing businesses to stay private for longer and capture much of their growth away from public investors.

That appears to be changing. SpaceX has listed, while OpenAI and Anthropic are expected to follow. Together, they represent one of the largest transfers of private-market value into public markets in recent history.

And while the opportunities these companies present are no doubt attractive in the here and now, history suggests investors would also be right to raise eyebrows over the timing.

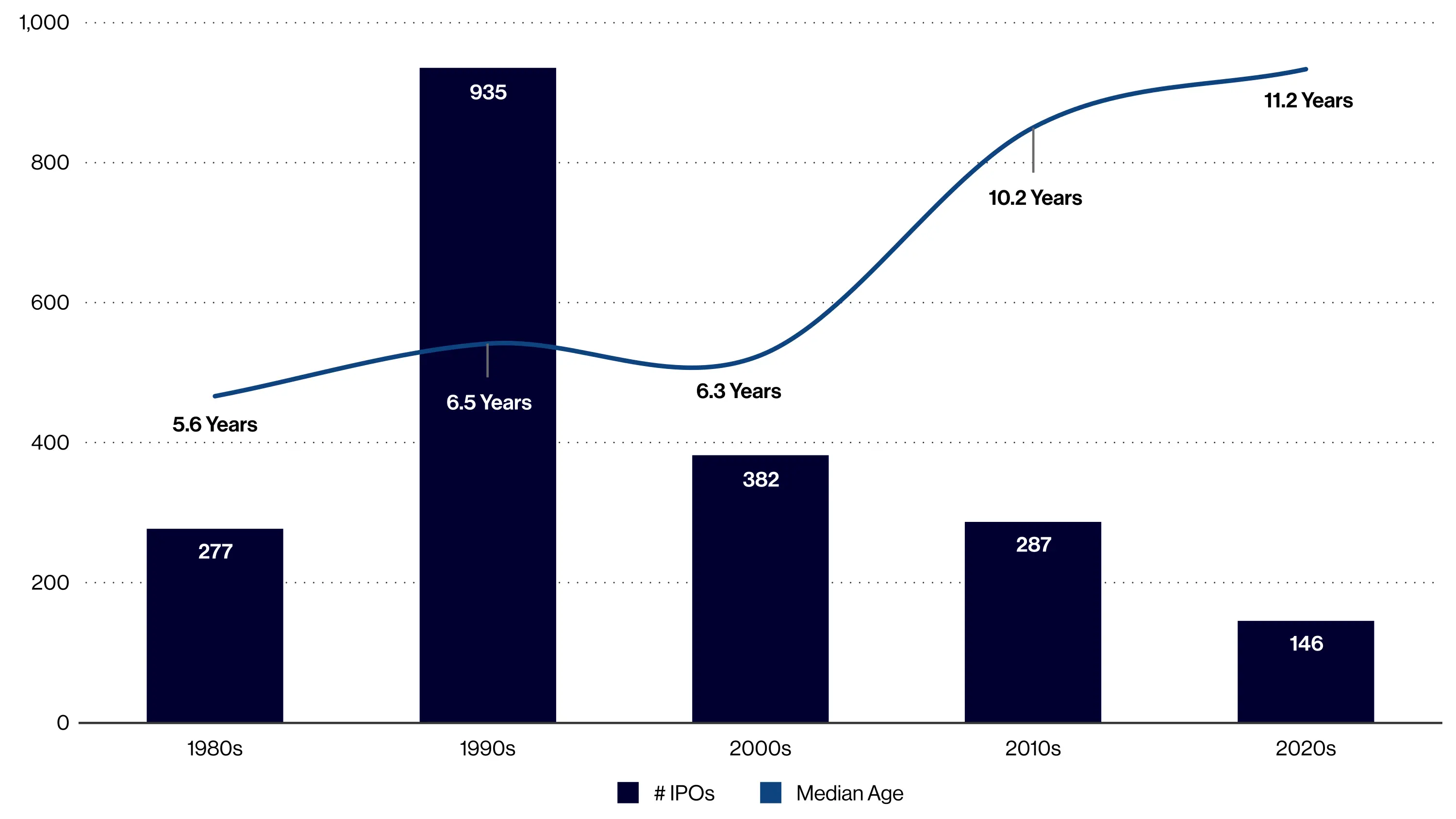

The great transfer

Over the past two decades, companies have remained private for longer and reached public markets at far higher valuations, allowing a growing share of wealth creation to occur before public investors could participate. Venture capital funds, sovereign wealth investors and private equity firms captured much of that value. And in the case of SpaceX specifically, its insiders and employees will receive handsome benefits.

The shift has been dramatic. In the 1980s, the median venture-backed technology company went public after 5.6 years. By the 2020s, that figure had doubled to 11.2 years, allowing a growing share of value creation to occur before public investors could participate.

VC-backed tech IPOs: Volume and median age by decade

Source: Jay R. Ritter, Director – The IPO Initiative; University of Florida. March 17, 2026. Cited - here

As a result, public stock markets shifted from funding innovation to providing liquidity for those who had funded it earlier. As our CEO Arian Neiron recently observed, "the market always prices the current product, not the future platform". The challenge for public investors is that by the time those platforms finally reach public markets, much of that future potential may already be reflected in the price.

For years, investors have watched companies such as SpaceX, OpenAI and Anthropic accumulate extraordinary valuations while remaining largely inaccessible. Their listings offer public investors exposure to businesses that generated much of their value behind closed doors.

SpaceX raised US$75 billion in the largest IPO in history, with demand reportedly exceeding the shares available by more than four times. At the offering price, the company was valued at roughly US$1.8 trillion. The scale of the demand is almost as remarkable as the valuation itself.

At that valuation, investors would be paying roughly 100 times annual revenue for a company that generated US$18.67 billion in sales last year but did not make a profit. Yet despite the IPO being multiple times oversubscribed, Morningstar analysts have already argued that SpaceX should be worth less than half of this US$1.8 trillion figure.

And while this may come across as a vote of confidence in a company's prospects, that interpretation is only half the story.

Every IPO creates an opportunity to buy, but it also allows early investors to lock in their gains. That means the challenge for new investors is two-fold: assessing the quality of the company on offer and determining why it is being offered now.

The US$200 billion+ question

The anticipated listings of SpaceX, OpenAI and Anthropic are arriving alongside an unprecedented race to build artificial-intelligence infrastructure.

Alphabet, a company that has historically funded growth from its own cash flows, recently raised nearly US$85 billion to fund data-centre expansion. Across the industry, capital is being deployed at extraordinary speed in pursuit of technologies whose ultimate commercial potential remains uncertain.

Between SpaceX's IPO, Alphabet's equity raising and the anticipated listings of OpenAI and Anthropic, investors may soon be asked to commit more than US$200 billion to companies linked directly to the AI and space themes.

After all, capital is not created by an IPO – it is redirected towards one.

The table below contains a number of familiar names. Many became category leaders and generated enormous wealth for long-term shareholders. Yet investors who bought them at listing often experienced brutal drawdowns before the story played out.

|

Company |

1 week |

1 month |

3 months |

6 months |

12 months |

Year 1 max drawdown |

|

|

17% |

-18% |

-45% |

-42% |

-31% |

-54% |

|

|

0% |

0% |

11% |

-32% |

-10% |

-58% |

|

Alibaba |

-4% |

-6% |

18% |

-9% |

-30% |

-49% |

|

Shopify |

7% |

38% |

14% |

9% |

2% |

-52% |

|

Block |

-9% |

-6% |

-24% |

-28% |

-7% |

-44% |

|

Twilio |

27% |

42% |

125% |

20% |

3% |

-66% |

|

Snap |

-7% |

-8% |

-13% |

-39% |

-26% |

-56% |

|

Okta |

4% |

1% |

0% |

18% |

64% |

-20% |

|

MongoDB |

-3% |

-7% |

-9% |

20% |

103% |

-26% |

|

Dropbox |

10% |

2% |

18% |

-7% |

-24% |

-54% |

|

Spotify |

4% |

14% |

13% |

21% |

-3% |

-46% |

|

Lyft |

-5% |

-23% |

-16% |

-46% |

-65% |

-79% |

|

Zoom |

5% |

45% |

54% |

9% |

142% |

-40% |

|

|

18% |

9% |

6% |

5% |

-28% |

-70% |

|

Uber |

1% |

3% |

-4% |

-34% |

-21% |

-68% |

|

CrowdStrike |

33% |

22% |

19% |

-18% |

64% |

-67% |

|

Cloudflare |

10% |

-13% |

0% |

6% |

90% |

-32% |

|

Datadog |

-14% |

-16% |

1% |

-15% |

128% |

-42% |

|

Snowflake |

-14% |

-5% |

30% |

-9% |

27% |

-52% |

|

Palantir |

5% |

13% |

164% |

132% |

153% |

-53% |

|

DoorDash |

-17% |

-19% |

-28% |

-28% |

-13% |

-47% |

|

Airbnb |

2% |

3% |

37% |

0% |

25% |

-39% |

|

Affirm |

9% |

44% |

-29% |

-40% |

-26% |

-65% |

|

Roblox |

10% |

2% |

31% |

22% |

-40% |

-69% |

|

Coupang |

-11% |

-7% |

-23% |

-36% |

-65% |

-64% |

|

Coinbase |

-5% |

-19% |

-30% |

-24% |

-55% |

-57% |

|

Robinhood |

46% |

35% |

2% |

-64% |

-74% |

-90% |

|

Rivian |

45% |

15% |

-36% |

-77% |

-67% |

-88% |

|

Arm Holdings |

-18% |

-20% |

11% |

106% |

132% |

-43% |

|

CoreWeave |

20% |

5% |

300% |

217% |

87% |

-65% |

|

Median |

3% |

1% |

4% |

-9% |

-9% |

-54% |

|

Average |

4% |

4% |

20% |

1% |

14% |

-55% |

|

% Positive |

57% |

57% |

57% |

43% |

43% |

n/a |

Source: Truist, Puru Saxena. Twitter is no longer publicly listed while Arm Holdings was delisted in 2016 then re-listed in 2023.

The price of belief

Whether SpaceX's valuation ultimately proves justified is almost beside the point.

Valuation multiples are, in large part, expressions of expectation. The higher the multiple, the greater the belief embedded within it. At 100 times revenue, investors are hoping that the US$350 billion global space industry will become, as Morgan Stanley estimates, a US$1 trillion industry by 2040. Such valuations leave little room for the future to arrive differently than expected.

History provides parallels for this moment. Research by Jay Ritter of the University of Florida shows that, across more than 9,000 operating-company IPOs between 1975 and 2021, 38.5% lost more than half their value within three years of their first day of trading, while nearly 60% generated negative three-year returns.

Table 1: Nearly 60% of IPOs generated negative returns within three years

|

Share price performance three years after IPO |

From the first close |

From the offer price |

||

|

Number of IPOs |

Percentage |

Number of IPOs |

Percentage |

|

|

Lost more than 50% |

3,537 |

38.5% |

3,215 |

35.0% |

|

Lost between 0% and 50% |

1,979 |

21.5% |

1,939 |

21.1% |

|

Gained between 0% and 50% |

1,333 |

14.5% |

1,351 |

14.7% |

|

Gained between 50% and 100% |

873 |

9.5% |

910 |

9.9% |

|

Gained between 100% and 200% |

759 |

8.3% |

880 |

9.6% |

|

Gained between 200% and 500% |

552 |

6.0% |

679 |

7.4% |

|

Gained between 500% and 1,000% |

123 |

1.3% |

159 |

1.7% |

|

Gained between 1,000% and 2,000% |

27 |

0.3% |

45 |

0.5% |

|

Gained between 2,000% and 3,000% |

6 |

0.1% |

10 |

0.1% |

|

Gained more than 3,000% |

6 |

0.1% |

7 |

0.1% |

|

Total (1975–2021) |

9,195 |

100.0% |

9,195 |

100.0% |

Source: Jay Ritter, University of Florida. Distribution of three-year buy-and-hold returns for 9,195 US operating-company IPOs (1975–2021), measured from the first closing price and offer price.

These figures do not suggest that IPOs are poor investments or that transformative companies cannot emerge from them. They can and do. Rather, the numbers highlight that IPOs are often exercises in valuation leverage. The companies may be exceptional, but the prices attached to them frequently embed lofty expectations.

This will be the challenge with SpaceX. At one level, it is being valued on rockets, satellites and launch contracts. At another, it is being valued on a future in which the global space economy expands dramatically, launch costs continue to fall, and the company retains a dominant position in an industry that barely exists today. Does every investor in the SpaceX IPO genuinely expect all three to occur in a timely manner without any hiccups?

Timing matters

SpaceX, OpenAI and Anthropic may ultimately justify every dollar of enthusiasm currently attached to them. They are, after all, visionary companies.

But the more interesting question over why so many of the world's most valuable private companies appear to have reached the same conclusion at roughly the same time remains. History suggests that companies come to market when conditions are very favourable, not weak.

Investors should pay attention not only to what is being sold, but also to when and why. The timing of an IPO does not tell us what happens next. It does, however, tell us something about the market conditions that made the offering possible.

Published: 19 June 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.