This tax time, wise investors are asking a different question

This year, tax time feels different to the usual exercise.

Normally, investors collate their annual tax statements every July, calculate gains and losses, lodge returns and move on. But the proposed tax reforms in this year’s Federal Budget have triggered the most significant debate about investment taxation in a generation.

The headlines have focused on the replacement of the 50% capital gains tax (CGT) discount with indexation and the introduction of a 30% minimum tax on capital gains, and what those changes might mean for property, shares and long-term wealth creation.

Budget 2026: What ETF investors need to know

Before exploring the implications, it is worth revisiting what has been proposed.

- The 50% CGT discount would be replaced by indexation.

- A 30% minimum tax on capital gains now applies.

- Superannuation remains largely outside the reforms.

- Investments held in personal names and trusts have always faced a different tax framework from those held in superannuation. But now, that difference is exacerbated in favour of superannuation.

- The proposals focus on the taxation of investors rather than investment products.

Investor reaction to Budget 2026

When we asked more than 1,400 investors what they thought of the Budget, the headline finding was predictable: they overwhelmingly disliked the proposed reforms. More interesting was what they intended to do next. Almost half now view superannuation as the preferred path to long-term wealth, suggesting investors are reassessing not only what they own, but the structures through which they build wealth.

Table 1: Long-term wealth path after the Budget

| Answer choices | Response rate |

| Superannuation is now the most tax-efficient vehicle and deserves a bigger allocation | 44.89% |

| Diversified strategy is now the clearest path | 17.99% |

| The tax regime is now sufficiently uncertain that I am holding more cash | 10.91% |

| ETFs and shares that offer high income with minimal growth | 10.17% |

Source: VanEck Federal Budget Survey, May 2026.

Recent negotiations over SMSF borrowing arrangements have reinforced that point. The debate has evolved from a discussion about how wealth is taxed into a discussion about how wealth is held.

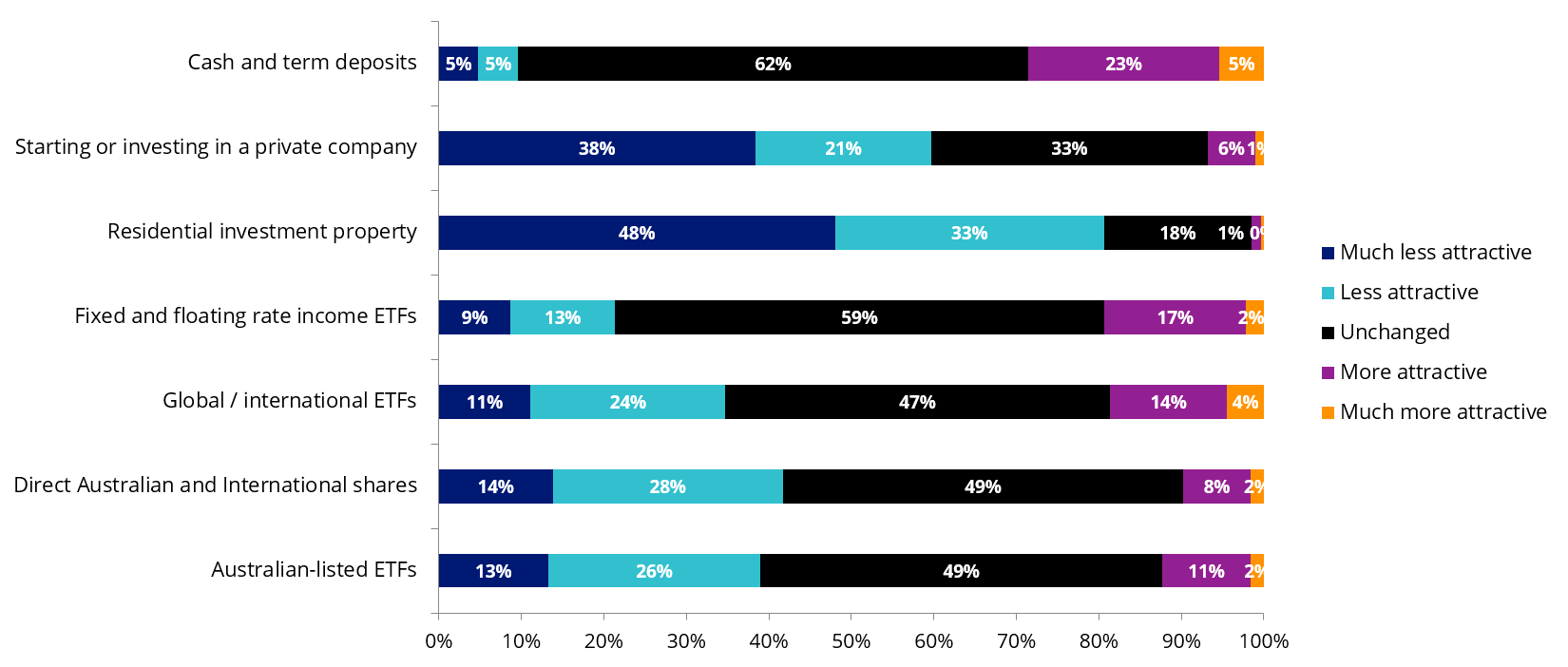

Chart 1: Five-year wealth accumulation preferences

Source: VanEck Federal Budget Survey, May 2026.

For decades, portfolio construction has largely been framed as a question of asset allocation. How much should be invested in shares, bonds, property or cash? Should investors favour Australian or international markets? Is growth preferable to income?

While those questions remain important, the Budget has introduced another one: what should you own and how should you own it.

The tax time question many investors have overlooked

Historically, ownership structure has often been viewed as an administrative consideration rather than an investment one. But the proposed reforms have brought that distinction into sharper focus.

Consider two investors holding the same ETF portfolio. One owns it in their own name, while the other holds it through superannuation. The investment exposure remains identical, but the tax treatment may not. An investor holding the portfolio in their own name now faces a different tax framework from one holding the same exposure through superannuation.

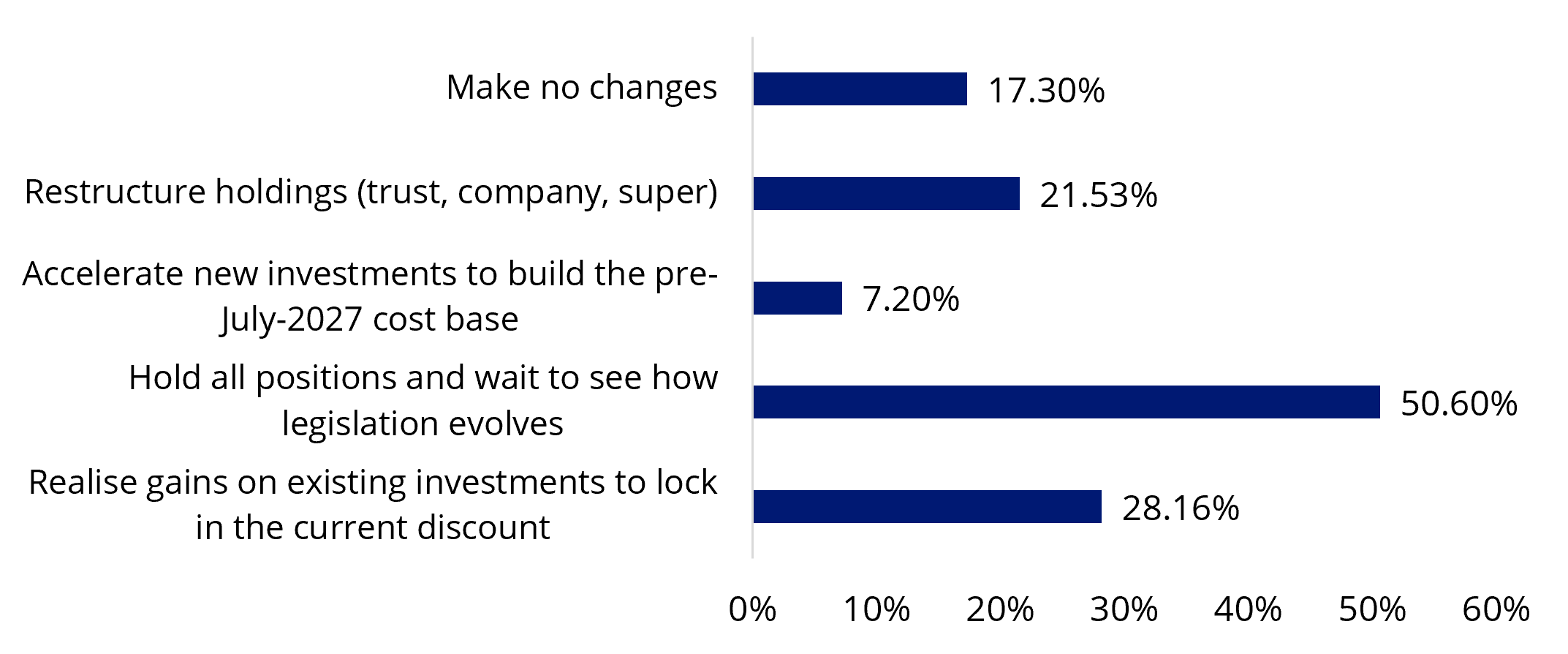

In response to the Budget, we conducted a survey of our investor base at a time when the reforms were still proposals and slogans. While more than half of respondents said they intended to wait for legislative clarity before making significant changes, more than one in five were already considering restructuring holdings.

Chart 2: Likely actions before 1 July 2027

Source: VanEck Federal Budget Survey, May 2026.

Is the growth versus income debate missing the point?

Much of the post-Budget analysis has framed the reforms as a battle between growth and income investing. The early wisdom has suggested that if capital gains become less attractive from a tax perspective, investors will naturally favour income producing assets such as the established banks and mature mining companies. But the reality is likely to be more nuanced.

As VanEck’s Arian Neiron recently argued in The Australian, tax changes of this magnitude can influence how markets price risk, resilience and shareholder return. He went on to suggest the reforms could accelerate a broader repricing of assets and that companies capable of compounding capital through the cycle, maintaining strong balance sheets and generating durable cash flows may become increasingly attractive.

The same principle may also apply to investment structures. As investors place greater emphasis on after-tax outcomes, ownership structure is becoming a more prominent part of portfolio construction. As investors place greater emphasis on after-tax outcomes, ownership structure is becoming a more prominent part of portfolio construction. Investors are paying closer attention to where assets are held, not just which assets they hold.

The tax advantages of investing in ETFs won’t change

One of the ironies of the current debate is that investors have become fixated on the proposed CGT changes while overlooking the tax mechanics that influence their portfolios every year.

When an equity ETF delivers exceptionally strong performance, it is because the value of the underlying shares has increased significantly. To continue tracking its index, the ETF must rebalance its portfolio as the index changes. In doing so, it may realise capital gains on appreciated holdings, which are then reflected in investors' annual tax statements.

That highlights an important principle: strong long-term performance and taxable capital gains often go hand in hand. Investors should not be surprised to see capital gains distributed after a particularly strong year.

Long before the Budget, ETF investors were already benefiting from structures designed to improve tax certainty and transparency. Many Australian ETF issuers, including VanEck, operate under AMIT1, while TOFA2influences how certain gains, losses and income streams are recognised for tax purposes.

These frameworks rarely attract attention, yet they can have a meaningful impact on after-tax outcomes. Importantly, as VanEck has argued before, the benefit depends not simply on using them, but on how effectively they are implemented in practice.

What else investors should not do

The Budget reforms have prompted many investors to reconsider how they build wealth. That is sensible. But there is a difference between being tax-aware and becoming tax-driven.

Being tax-aware means understanding how taxes affect investment outcomes and incorporating that knowledge into portfolio decisions. Being tax-driven means tax considerations would override investment fundamentals, whether that means abandoning a sound strategy, concentrating portfolios in a single structure or making decisions based primarily on tax outcomes rather than long-term objectives.

Tax matters, but it is only one component of long-term wealth creation. Investors still need to balance risk, return, diversification and time horizon. The reforms may change the after-tax outcome of some decisions, but they do not change the principles that have historically driven successful investing. The most successful investors are unlikely to be those who react most aggressively to the new rules. They are more likely to be those who understand the implications, adapt where appropriate and don’t make rash, wholesale portfolio changes as a result.

After all, paying tax on an investment usually means it has generated a gain. The challenge is not avoiding tax altogether but ensuring you keep as much of those gains as possible over time.

A different way to think about tax time

Tax time is usually about looking backwards. This year, it has prompted many investors to look forwards. The proposed reforms have reignited debate about capital gains tax, but they have also highlighted a broader truth: after-tax outcomes matter. That helps explain why so many investors are reassessing not only what they own, but how they own it.

Footnotes:

1: AMIT (Attribution Managed Investment Trust) is a tax system for Australian managed funds and ETFs. It means investors are taxed on the income the fund allocates to them for the financial year, rather than the actual cash payout they receive. You can read more about AMIT here.

2: TOFA is an Australian tax framework that changes how large funds calculate gains and losses on complex financial instruments, such as foreign currency hedges. The resulting tax calculations are passed through to you and will be automatically reflected on your annual investor tax statement. You can read more about TOFA here.

Published: 03 July 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.