This investment style has beaten the market

The international equities universe offers a wide range of investing opportunities but one of the most forgotten yet longstanding approaches is ‘value’ investing.

Inflation has re-emerged as a key risk for markets. Oil market volatility, geopolitical uncertainty and high levels of government debt are contributing to a higher-for-longer inflation environment. The international equities universe offers a wide range of investing opportunities but one of the most forgotten yet longstanding approaches is ‘value’ investing.

Investors have been rotating away from high-priced growth stocks and focusing on tangible cash flows, robust balance sheets, and reasonable valuations – companies known as “value” companies.

In May, the VanEck MSCI International Value ETF (ASX: VLUE) returned +15.08%, outperforming the MSCI World ex Australia Index by 10.55%. Since the beginning of the year to 31 May 2026, VLUE returned +25.26%, outperforming the benchmark by 22.88%.

While past performance is not indicative of future performance, we believe the conditions supporting VLUE’s recent outperformance remain firmly in place. For investors seeking international equity exposure beyond expensive growth companies, VLUE offers a disciplined way to access attractively valued global businesses well positioned for the current market environment.

What is value investing?

Value investing is a disciplined approach that looks for companies trading at attractive prices relative to their fundamentals, such as earnings, book value and cash flow.

The premise is that markets do not always price companies rationally. Sometimes fundamentally sound businesses fall out of favour as investors chase more popular themes or higher-growth companies. A value investor looks for the gap between what a company may be worth and what the market is currently willing to pay.

While this seems an intuitively straightforward path to investment success and history supports that argument, taking the right 'value' approach is important.

The opposite of value investing is ‘growth investing’ - paying a premium today for companies expected to grow fast in the future. Think high-flying US tech stocks. Both approaches have their place, but when growth valuations become stretched, value tends to take the lead. That is what has been happening.

Three reasons value may have further to run

1. Inflation pressure likely to stay elevated

Historically, value companies have tended to be better placed in periods where inflation and interest rates remain elevated. The ongoing oil crisis, alongside other factors such as historically high global government debt, could sustain inflationary pressures. While markets have priced in a quick resolution to the US-Iran conflict, oil prices remain up around 56% from six months ago. Elevated oil and commodity prices have typically been a leading indicator of higher inflation.

2. US economic growth outlook still resilient

Despite a number of growing pains including mounting fiscal debt, tariff disruption, a shrinking labour force following immigration policy pivot and an ongoing war with Iran, the US economy still looks resilient with consensus forecast real growth at ~2% for 2026 and 2027.

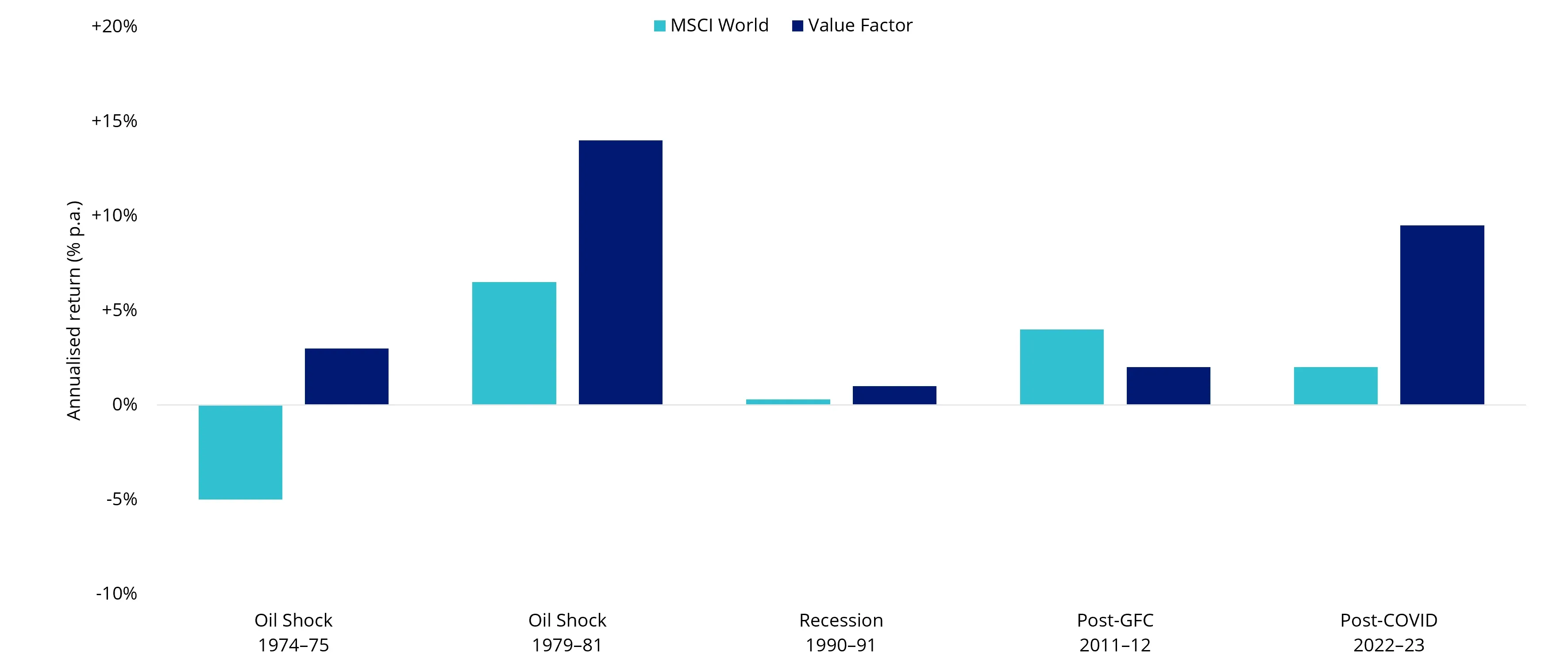

In combination, somewhat resilient growth with growing long-term risk and persistent inflation pressure paints a stagflationary picture over the coming months, which is a potentially favourable environment for value companies. Value outperformed in four of the last five stagflation periods, as shown below.

Chart 1: Performance during stagflation periods

Source: Bloomberg; Value is MSCI World Value Factor (pre-2000) and MSCI World Enhanced Value Factor (post-2000); You cannot invest in an index. Returns in US dollars. Past performance is not indicative of future performance.

2. Valuations remain compelling

Even after strong recent performance, value companies are not trading at stretched levels. Value (based on the MSCI World ex Australia Enhanced Value Top 250 Select Index) is trading at levels close to its 10-year average. From a relative value perspective, valuations are also at a multi-year low relative to broader equities1(not sure where the footnote is but this should be MSCI World ex Aus Index) indicating potential headroom on the upside.

The recent US earnings season has also confirmed that value fundamentals are meaningfully improving. The past three quarterly results have seen value companies report more net beats than the benchmark. As of 31May 2026, Q2 has been the strongest out of the past five quarters, with sell-side analysts forecasting higher year-on-year EPS growth than the broader market over the next two years.

Table 1: VLUE Performance to 31 May 2026|

|

1 month (%) |

3 months (%) |

YTD (%) |

1 year (%) |

3 years (% p.a.) |

5 years (% p.a.) |

Since VLUE inception date (% p.a.) |

|

VLUE |

15.08 |

19.69 |

25.26 |

49.60 |

26.14 |

17.69 |

18.11 |

|

MSCI World ex Australia Index |

4.53 |

6.44 |

2.38 |

14.18 |

17.78 |

13.72 |

14.92 |

|

Difference |

+10.55 |

+13.25 |

+22.88 |

+35.42 |

+8.36 |

+3.97 |

+3.19 |

Source: VanEck, Morningstar, Bloomberg. Results assume immediate reinvestment of all dividends and include management fees but exclude brokerage costs and taxes. Past performance is not indicative of future performance.

VLUE inception date is 8 March 2021, and a copy of the factsheet is here.

The MSCI World ex Australia Index (“MSCI World ex Aus”) is shown for comparison purposes as it is the widely recognised benchmark used to measure the performance of developed market large- and mid-cap companies, weighted by market capitalisation. VLUE’s index measures the performance of 250 international large- and mid-cap companies selected from the MSCI World ex Australia Index with high value scores relative to their peers at rebalance. Exclusions apply for weapons and tobacco. Consequently, VLUE’s index has fewer companies and different country and industry allocations than MSCI World ex Aus. Click here for more details.

Not all value ETFs are the same

VLUE provides exposure to around 250 companies diversified across countries and sectors, with high value scores based on price-to-book, price-to-forward earnings, and enterprise value-to-cash flow. These measures are assessed relative to sector peers, which helps avoid unintended sector concentration and reduces the risk of simply owning companies that look cheap for the wrong reasons.

For investors who want to manage the currency exposure in their international value allocation, ASX: HVLU is the Australian dollar hedged version of VLUE.

Key Risks

An investment in our international value ETF carries risks associated with: ASX trading time differences, financial markets generally, individual company management, industry sectors, foreign currency, country or sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the VanEck MSCI International Value ETF PDS and TMD for more details.

VLUE/HVLU is likely to be appropriate for a consumer who is seeking capital growth, is intending to use the product as a major, core, minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

1MSCI World ex Australia Index

Published: 04 June 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person$B!G(Bs financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund$B!G(Bs investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed. Past performance is not indicative of future performance.

VanEck MSCI International Value ETF is indexed to a MSCI index. VLUE is not sponsored, endorsed or promoted by MSCI, and MSCI bears no liability with respect to VLUE or the MSCI Index. The PDSs contain a more detailed description of the limited relationship MSCI has with VanEck and the Fund.