AI's unicorn test is fast approaching

Credible estimates put AI capex this year at somewhere between US$750 billion and US$1 trillion, with the trajectory pointing higher still in the years ahead.

Nvidia’s Jensen Huang estimates that each gigawatt (GW) of data-centre capacity carries a build cost of US$80–100 billion. With credible forecasts pointing to some 190GW slated between now and 2030, the implied outlay runs to the order of US$15 trillion of capex.

The hyperscalers’ free cash flow, meanwhile, is being steadily consumed. Players such as OpenAI and SpaceX, lacking sufficient alternative revenue streams, will be compelled to return repeatedly to capital markets. Within weeks of its IPO, SpaceX intends to tap debt markets for a further, and hardly trifling, US$25 billion in debt funding.

The more cynical observer might ask why SpaceX, OpenAI and Anthropic are all rushing to market at once. Layer on persistent government deficits and illiquid private markets straining for exits, and the result is a near-perfect convergence of competing demands on capital.

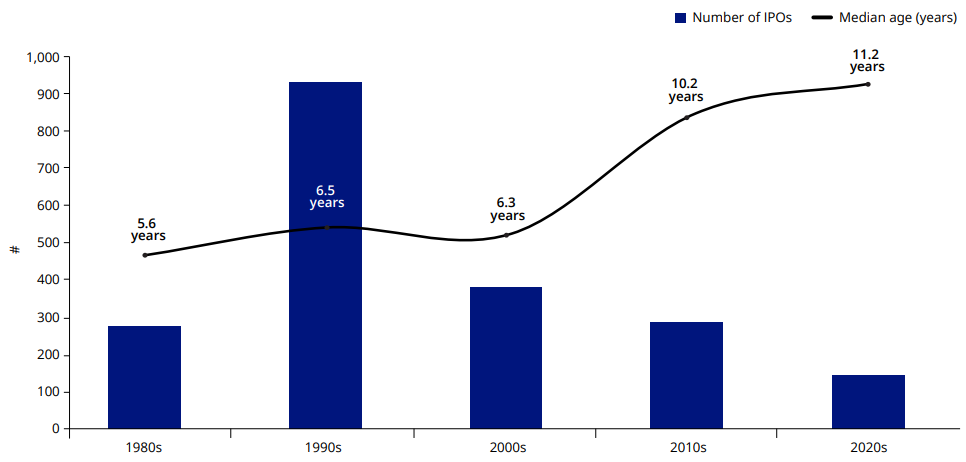

Chart 1: Companies staying private for longer - Venture Capital (VC) backed tech IPOs: Volume and median age by decade

Source: Jay R. Ritter, Director – The IPO Initiative; University of Florida. March 17, 2026.

And this is before confronting the more fundamental question of whether the sector can generate the revenue required to earn an acceptable return on that capital. Given the apparently short useful life of GPUs, depreciation alone represents a staggering figure.

Cast back to the dotcom era, when the notion of the ‘unicorn’, the billion-dollar startup, first captured the market’s imagination. How might a discerning investor have distinguished a genuine unicorn from a donkey? The test, with the benefit of hindsight, was simple enough: weigh the upfront cost of acquiring a customer against annual revenue per customer, multiplied by margin and by annual retention. A ratio above three marked a unicorn; below one, a donkey.

AI firms may now be nearing their own donkey-or-unicorn reckoning.

The return of the unicorn test

Consider the recent trajectory. Phase one was, in effect, loss-leading: entry-level models were offered free of charge and the most capable models made available by subscription at well below cost, the objective being to build adoption.

That phase succeeded. Many organisations adopted the technology wholeheartedly, actively encouraging staff to maximise usage, an entirely rational posture while the marginal cost of additional tokens, under those subscription plans, was effectively zero.

Phase two marks the providers’ shift toward an economic return: charging for usage. Given the substantial costs of inference, the appropriate price point remains genuinely uncertain. The shift also produces a pronounced uplift in reported revenue, a figure these companies are understandably keen to highlight as they frame their IPO terms.

Phase three is the more demanding test: customer retention. How will clients respond once pricing approaches, or exceeds, the providers’ own costs? The early evidence, admittedly anecdotal, is not encouraging. Some firms appear genuinely concerned by escalating AI bills; others may find the technology so embedded in their operations that the cost of reverting is itself prohibitive.

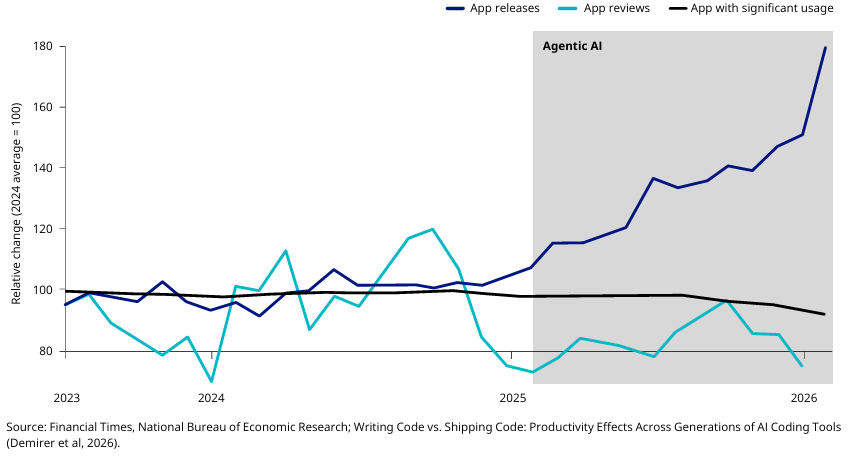

Chart 2: App releases to the moon, enthusiasm grounded

Source: Financial Times, National Bureau of Economic Research; Writing Code vs. Shipping Code: Productivity Effects Across Generations of AI Coding Tools (Demirer et al, 2026).

At the same time, a growing body of research suggests that comparatively little of the AI revolution is yet translating into measurable productivity or earnings. A notable NBER study finds that the lower barrier to application development has principally yielded a proliferation of applications for which there is little demand: output has risen, while sales and genuine enthusiasm have not.

Finally, outside the genuine frontier, Chinese models are proving an adequate and in some respects more flexible substitute, at a fraction of the cost. Firms confronting steep AI bills are, on anecdotal evidence, increasingly willing to migrate to these lower-cost alternatives.

Taken together, these dynamics suggest that the steep revenue curves now on display are likely to inflect meaningfully over the coming quarters. For some providers, completing an IPO ahead of that inflection may well prove critical.

You can read more about this subject in the latest edition of VanEck Viewpoint. Click here to download the PDF.

Published: 06 July 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.