Why a higher-for-longer world may favour this investing style

One of the enduring appeals of value investing is that it asks a simple question: what if the market has got this one wrong?

Rather than chasing companies already commanding premium valuations, value investors spend their time looking for businesses that have fallen out of favour, where the share price no longer reflects the strength of the underlying business. Sometimes the market is right. Occasionally, though, it isn't. And when sentiment shifts to match improving fundamentals, the rerating can be substantial.

Micron Technology is a good example.

Not long ago, Micron was largely viewed as another cyclical semiconductor company whose fortunes rose and fell with the memory chip market. Today, it's one of the world's best-performing large-cap technology companies after emerging as a key supplier of the high-bandwidth memory chips powering the rapid build-out of artificial intelligence infrastructure.

Its latest quarterly result captured how dramatic that transformation has been. The company reported record revenue, comfortably beat earnings expectations and delivered gross margins above 85%, driven by exceptionally strong demand for its AI-related memory products.

For value investors, Micron's success isn't simply a story about AI. It's an example of what the investment style is designed to capture: companies whose prospects improve long before the wider market fully recognises what's changed.

Identifying these opportunities consistently is easier said than done. That's why many value strategies take a diversified, systematic approach instead, building portfolios of companies trading at attractive valuations with the expectation that some will eventually experience the kind of rerating Micron has enjoyed.

One of the more interesting features of this cycle is that "value" no longer means avoiding technology. Micron is a reminder that valuation and innovation aren't mutually exclusive. Companies can sit at the centre of one of the world's biggest structural growth themes while still offering attractive valuations if the market underestimates how quickly fundamentals are changing.

That philosophy has underpinned the recent performance of the VanEck MSCI International Value ETF (VLUE). While Micron has been one of the strategy's standout contributors over the past year, its returns reflect something much more than the success of a single stock. The results suggest that Micron has been one contributor to a successful investment theme rather than a one-off fluke.

Table 1: VLUE performance as at 30 June 2026

|

|

1 month (%) |

3 months (%) |

YTD (%) |

1 year (%) |

3 years (% p.a.) |

5 years (% p.a.) |

Since VLUE inception date (% p.a.) |

|

VLUE |

3.45 |

28.77 |

29.58 |

52.27 |

26.04 |

18.15 |

18.56 |

|

MSCI World ex Australia Index |

3.14 |

12.61 |

5.60 |

14.95 |

17.79 |

13.38 |

15.35 |

|

Difference |

+0.31 |

+16.16 |

+23.98 |

+37.32 |

+8.25 |

+4.77 |

+3.21 |

Source: VanEck, Morningstar, Bloomberg. Results assume immediate reinvestment of all dividends and include management fees but exclude brokerage costs and taxes. Past performance is not indicative of future performance. VLUE inception date is 8 March 2021, and a copy of the factsheet is here. The MSCI World ex Australia Index (“MSCI World ex Aus”) is shown for comparison purposes as it is the widely recognised benchmark used to measure the performance of developed market large- and mid-cap companies, weighted by market capitalisation. VLUE’s index measures the performance of 250 international large- and mid-cap companies selected from the MSCI World ex Australia Index with high value scores relative to their peers at rebalance. Exclusions apply for weapons and tobacco. Consequently, VLUE’s index has fewer companies and different country and industry allocations than MSCI World ex Aus. Click here for more details.

More than that, Micron's story highlights something investors may be underestimating today. While much of the market's attention remains fixed on a relatively small group of AI leaders, the opportunity set has broadened. Companies across a range of sectors such as financials and telecommunications continue to trade at valuations that imply relatively modest expectations despite generating healthy cash flows and, in many cases, improving earnings outlooks.

If market leadership continues to widen beyond a handful of mega-cap growth stocks, the environment could become increasingly supportive for value-oriented strategies.

Table 2: VLUE’s top 10 holdings, as at 1 July 2026

|

Security Name |

Country |

Sector |

Index Weight |

|

Micron Technology, Inc. |

United States |

Information Technology |

4.93 |

|

Kioxia Holdings |

Japan |

Information Technology |

3.48 |

|

Salesforce, Inc. |

United States |

Information Technology |

2.16 |

|

Verizon Communications |

United States |

Communication Services |

2.03 |

|

QUALCOMM |

United States |

Information Technology |

1.99 |

|

Toyota Motor Corp. |

Japan |

Consumer Discretionary |

1.87 |

|

Comcast Corporation |

United States |

Communication Services |

1.58 |

|

AT&T Inc |

United States |

Communication Services |

1.57 |

|

Adobe Inc. |

United States |

Information Technology |

1.47 |

|

Hewlett Packard Enterprise Co. |

United States |

Information Technology |

1.35 |

Source: MSCI, 1 July 2026. Holdings and weightings are subject to change.

Why the environment may continue to favour value

The next question, of course, is whether the backdrop that has supported value investing over the past few years is likely to persist. While no one can forecast interest rates with certainty, several structural trends suggest inflation may remain more persistent than many investors expect.

We expect inflation to remain above the US Federal Reserve's target over the medium term. A resilient labour market continues to place upward pressure on sticky services inflation, even as energy prices have eased. If inflation proves more persistent than markets currently expect, interest rates are also likely to remain higher for longer.

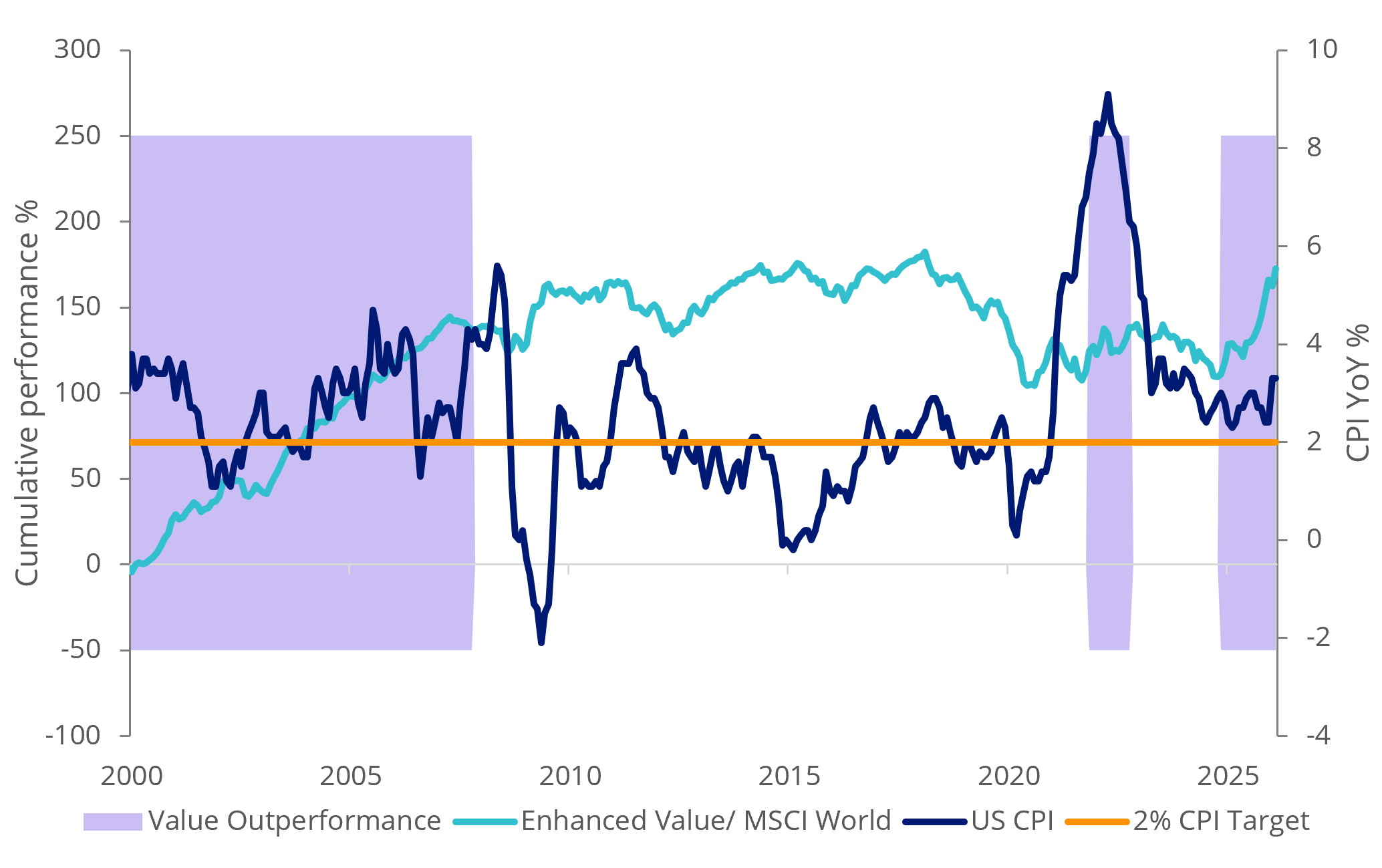

Charts 1 and 2: US inflation and long duration bond yields

Source: Bloomberg, Chart 1: 31 May 2026, Chart 2: 30 June 2026

Historically, this has been a supportive environment for value investing. Higher interest rates reduce the premium investors are willing to pay for distant future earnings, often leading markets to place greater emphasis on companies generating strong cash flows and trading on attractive valuations today.

The chart below shows this theory in action in the context of previous historical allegories: namely the era between the dot-com bubble and the Global Financial Crisis as well as the 2022 inflation surge.

Chart 3: Value’s periods of outperformance since 2000

Source: Bloomberg. 30 June 2026. Enhanced Value is MSCI World Australia Enhanced Value Top 250 Select Index. Value outperformance is Enhanced Value minus MSCI World Index Past performance is not indicative of future performance.

Bottom line

Value investing has always been cyclical. It falls out of favour when investors are willing to pay ever higher prices for future growth and tends to regain momentum when markets begin rewarding today's earnings and cash flows. If the higher-for-longer environment persists, we think the current shift may still have further to run.

For investors seeking diversified exposure to companies exhibiting attractive value characteristics, we believe the case for VLUE remains compelling.

Key risks

An investment in our international value ETF carries risks associated with: ASX trading time differences, financial markets generally, individual company management, industry sectors, foreign currency, country or sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the VanEck MSCI International Value ETF PDS and TMD for more details.

VLUE is likely to be appropriate for a consumer who is seeking capital growth, is intending to use the product as a major, core, minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

Published: 06 July 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. The product disclosure statement (PDS) and the target market determination (TMD) for all Funds are available at vaneck.com.au. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable PDS and TMD for more details on risks. Investment returns and capital are not guaranteed.