The case for investing in the share market’s middle child

Large caps like BHP and Commonwealth Bank dominate headlines and exert the greatest influence on the returns of the whole Australian share market. These are the ‘big’ kids. Small caps, meanwhile, often attract attention for their higher-risk, higher-reward potential. Many of these companies are in their growth phase, still finding their feet.

Then there is the market’s middle child.

Mid-cap companies rarely command the same attention when investors are focused on a small group of market heavyweights. But with developed-market bond yields at their highest levels in more than two decades, earnings expectations for some large-cap companies are becoming harder to sustain, and with mid-caps continuing to trade at a discount to the ASX 50, investors now have reason to take a closer look.

Is a broader market emerging?

If history is any guide, markets do not tend to stay this concentrated for long. While mega-cap companies have dominated the ASX 200’s returns in recent years, history suggests periods where only a small number of stocks are driving the market tend to be the exception rather than the rule.

Similar shifts have often emerged during periods of higher interest rates and slower economic growth, when investors become more selective about where earnings growth is likely to come from. In those environments, companies able to keep growing earnings even as conditions become more difficult tend to attract greater attention from investors focused on consistency rather than simply market size.

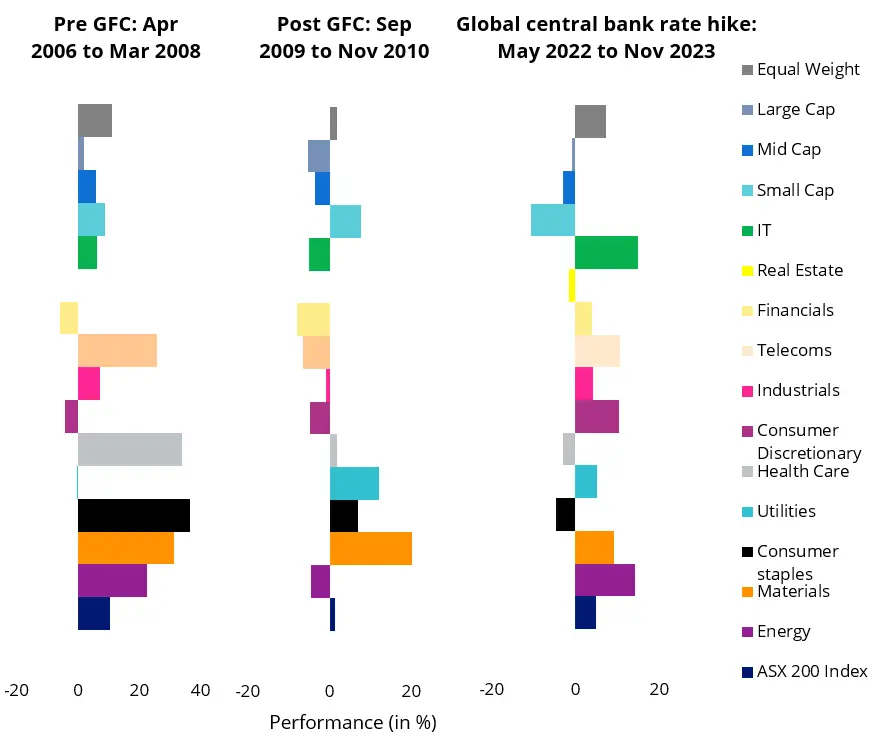

The pattern has also appeared during previous hiking cycles. While sector performance has varied, periods of rising rates have often coincided with stronger returns from materials and strategies that spread investments more evenly across the market.

Source: VanEck, Bloomberg. S&P 200 sector indices. RBA interest rate. Performance in AUD. You cannot invest in an index. Past performance is not indicative of future performance. Large Cap as S&P/ASX 20, Mid Cap as S&P/ASX Mid Cap 50, Small Cap as S&P/ASX Small Ordinaries, Equal Weight as MVIS Australia Equal Weight.

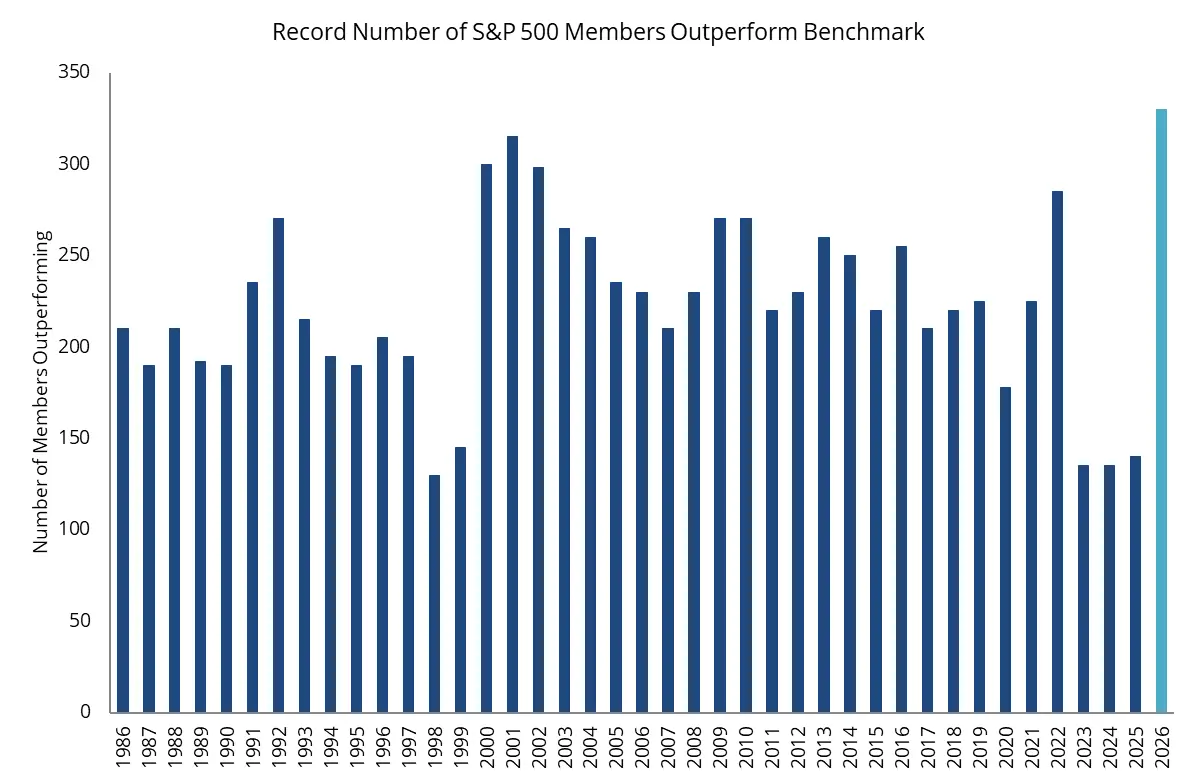

There are already signs that a shift may be emerging again. In the United States, a record share of S&P 500 companies has outperformed the index this year, reversing the unusually narrow leadership that defined much of the past two years.

Source: Bloomberg, as at 24 February 2026. As published in https://au.investing.com/analysis/record-share-of-sp-500-stocks-now-outperforming-the-index-200611961

What about Australia’s share market?

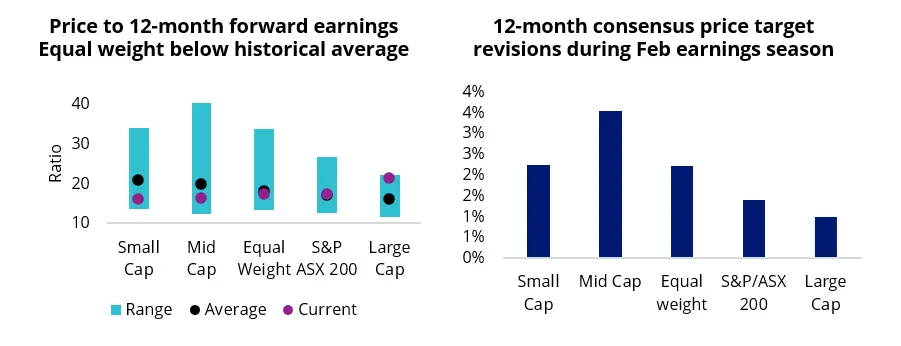

Signs of that shift are already beginning to emerge in Australia. While large caps have outperformed since February reporting season, smaller companies delivered some of the market’s strongest earnings surprises and most positive analyst target revisions. That suggests investors and analysts alike are beginning to see more room for earnings growth and share price improvement.

Source: Bloomberg. 1 April 2014 to 30 April 2026 (PE ratio), 31 December 2025 to 31 March 2026 (Price target) due to data availability. Large Cap as S&P/ASX 20, Mid Cap as S&P/ASX Mid Cap 50, Small Cap as S&P/ASX Small Ordinaries, Equal Weight as MVIS Australia Equal Weight. The ASX index series is shown for comparison purposes as it is the widely recognised benchmark series used to measure the performance of the Australian equities market. It weights companies by market capitalisation. Past performance is not indicative of future results. You cannot invest in an index. Results assume immediate reinvestment of all dividends.

Importantly, much of this is occurring while valuations outside the largest companies continue to trade at a discount to the S&P/ASX 50 despite the improvement in earnings forecasts.

That backdrop matters because increasingly concentrated markets can create risks of their own. Large caps continue to account for a large share of Australian equity market performance, even as rising inflationary pressures, elevated bond yields and geopolitical uncertainty threaten to make earnings expectations harder to sustain.

This could leave the market’s overlooked middle increasingly relevant. Mid-cap companies often combine the resilience associated with larger businesses with the flexibility to adapt and grow as conditions change. For investors, exposure beyond the market’s biggest names may also help reduce reliance on a small number of companies to drive the largest returns.

Positioning for a broader market

For investors, the implication may be straightforward: periods of narrow market leadership do not tend to last indefinitely. If market returns continue to broaden beyond the largest companies, diversification by holding companies in different sectors and of different market capitalisation sizes may become increasingly important.

That is where equal-weight and mid-cap exposures may become increasingly relevant. Strategies that spread investments more evenly across the market, such as the VanEck Australian Equal Weight ETF (ASX: MVW) have historically proven more resilient during previous hiking cycles, while mid-caps can provide exposure to a broader range of earnings drivers beyond the market’s largest companies.

For investors looking to access that part of the market, the VanEck S&P/ASX MidCap ETF (MVE) offers exposure to 50 established ASX-listed mid-cap companies across sectors, including industrials, healthcare, technology, resources and consumer businesses. As Australia’s only dedicated mid-caps ETF, MVE tracks the S&P/ASX MidCap 50 Index, providing investors with a diversified exposure to a segment of the market that has historically sat between the defensiveness of large caps and the growth potential of smaller companies.

If market leadership continues to broaden beyond the index heavyweights, the share market’s overlooked middle child may no longer be so easy to ignore.

Read more in the VanEck Portfolio Compass: Australian Equities Outlook 2026 here.

Key risks

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

An investment in MVW or MVE carries risks associated with financial markets generally, individual company management, industry sectors, stock and sector concentration, fund operations and tracking an index. See the PDS and TMD for details.

MVW is likely to be appropriate for a consumer who is seeking capital growth and a regular income distribution, is intending to use the product as a core, minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

MVE is likely to be appropriate for a consumer who is seeking capital growth and a regular income distribution, is intending to use the product as a minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

Published: 25 May 2026

Important information

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.