The soundtrack investors can no longer ignore

For much of the past decade, a strong US dollar and synchronised global monetary policy meant Australian investors benefited simply from owning unhedged offshore equities. That environment is becoming less one-sided. A decline in the US dollar, splintering central banks and recent commodity shocks mean offshore gains no longer translate as cleanly into local returns as they once did.

For some investors, that may increase the appeal of hedged international exposures, which aim to insulate your portfolio from changes in exchange rates so that your returns more closely reflect the performance of the companies you are invested in.

But the bigger shift is that Australian investors can no longer afford to treat currency exposure as a background issue sitting quietly beneath international portfolios.

How currency shapes returns

In an unhedged portfolio, when the Australian dollar falls, offshore returns are amplified when translated back into our local currency. When the Australian dollar rises, those same currency movements can dilute returns even when the underlying investment performs well.

As a result, exchange rate movements can materially shape long-term portfolio outcomes alongside the underlying investments themselves. And while exchange rates change constantly, currency cycles tend to persist for years rather than months, often closely tied to broader economic and interest-rate cycles.

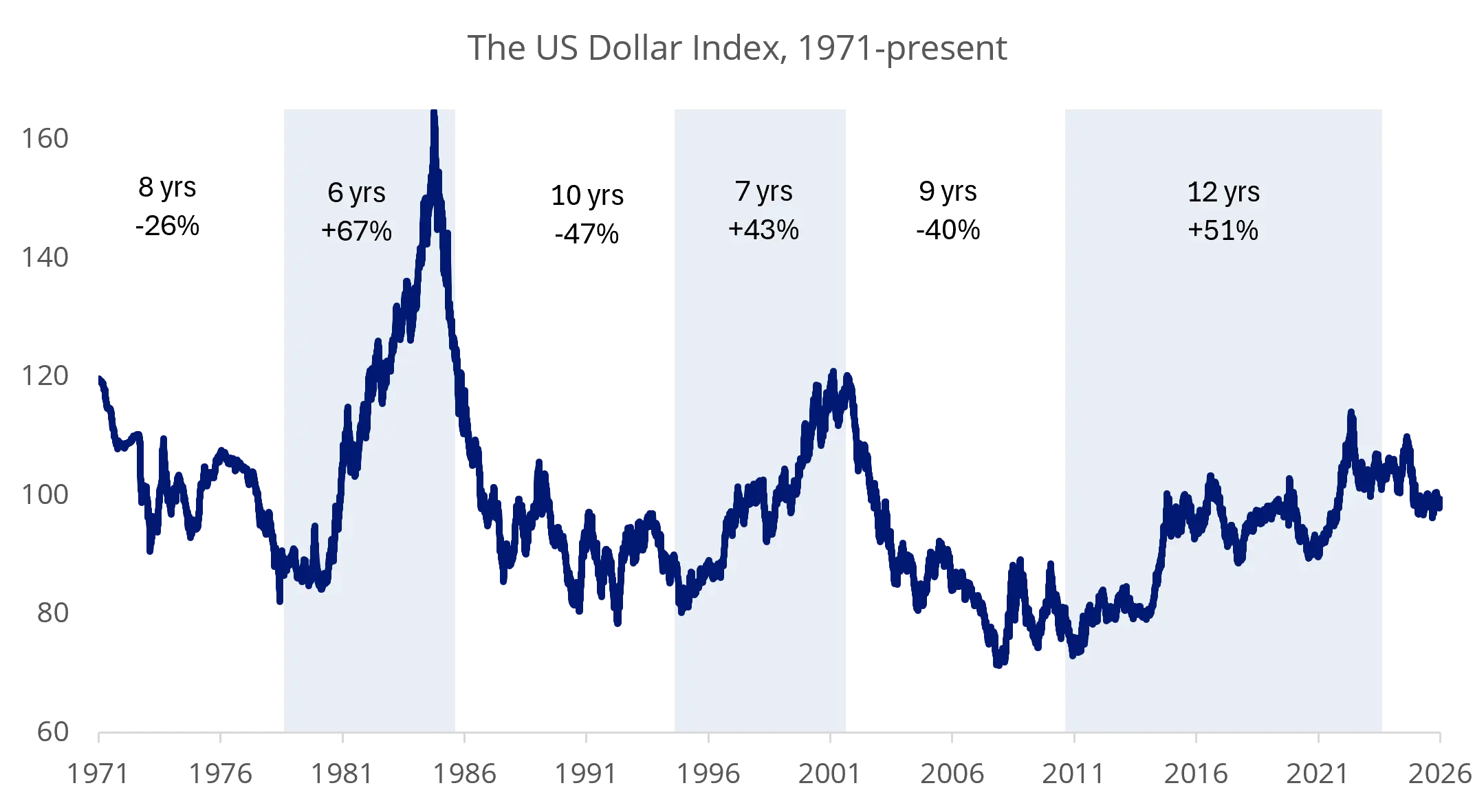

Chart 1: The world’s reserve currency moves in long-term cycles

Source: Bloomberg, as at 26 May 2026.

For much of the past decade, Australian investors with exposure to US assets benefited from a persistently weak Australian dollar and strong US dollar. In practice, currency acted as a tailwind for unhedged international portfolios.

But since 2024, the Australian dollar has shown signs of entering a more sustained recovery against the US dollar. Strong offshore equity performance no longer translates as cleanly into local returns. In some cases, gains generated by the underlying investment have been partially offset by a strengthening Australian dollar.

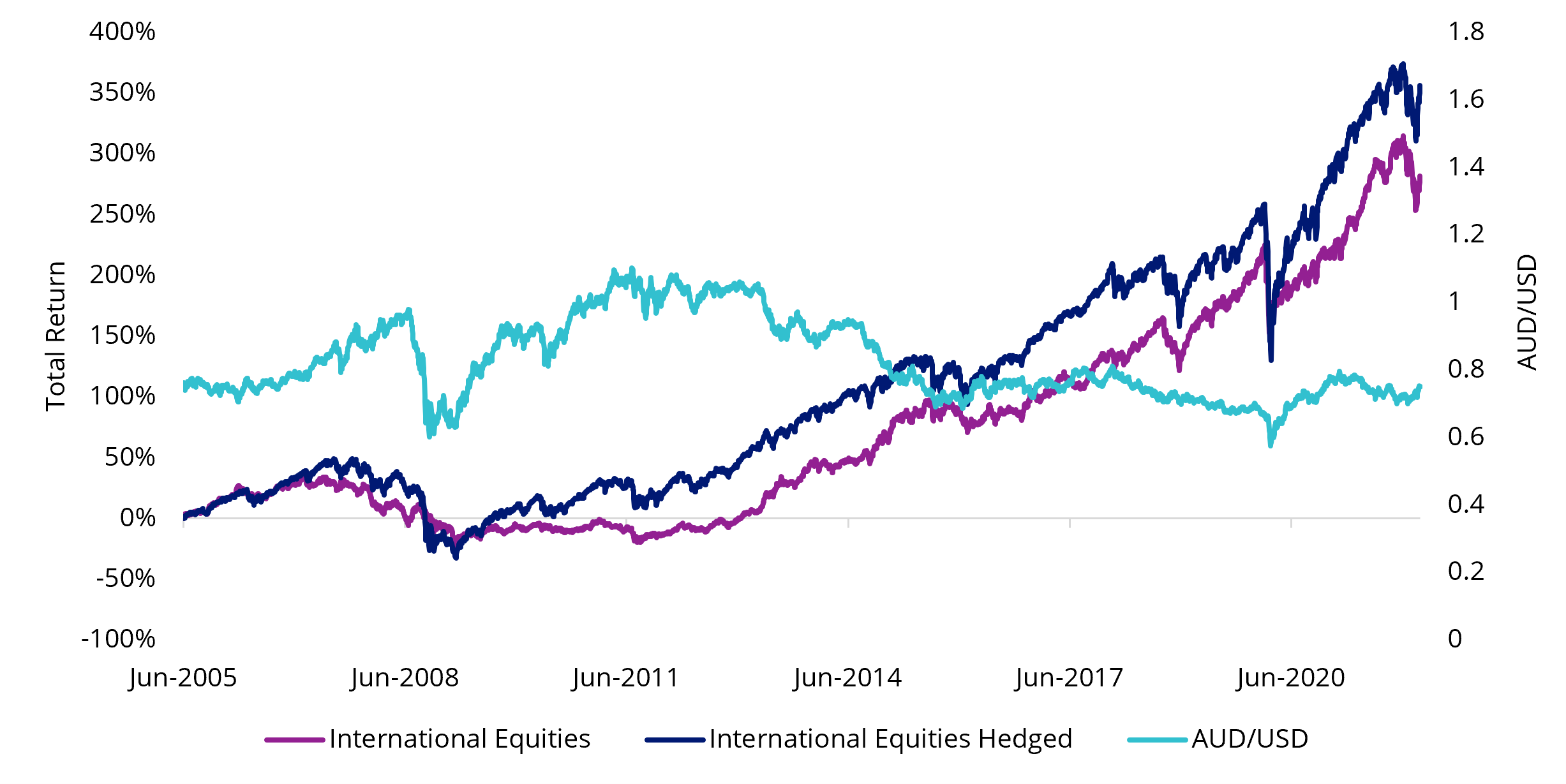

Chart 2: Australian dollar and hedged and unhedged international equities returns

Source: Bloomberg, 1 June 2005 to 26 May 2026. International Equities is MSCI World ex Australia Index. International Equities Hedged is MSCI World Ex Australia 100% Hedged to AUD Index. You cannot invest in an index. Past performance is not indicative of future performance.

This is where currency hedging can become a consideration. Rather than leaving portfolio returns fully exposed to foreign exchange markets, hedging strategies seek to reduce the impact of currency movements on investment outcomes. Typically, this is achieved through forward currency contracts that reduce the impact of exchange rate fluctuations between the Australian dollar and foreign currencies.

Australian dollar-hedged ETFs embed these tools within the ETF itself, meaning investors do not need to manage currency hedging themselves. For many international equity investors, the ability to hedge is important.

According to the 2023 ASX Australian Investor Study, one in five Australian investors now hold ETFs, up from 15% in 2020. International equity ETFs have consistently attracted some of the strongest inflows across the Australian ETF market in recent years. As more Australians invest internationally, currency exposure is increasingly becoming part of the investment experience itself.

A brave new world

A rising US market and falling Australian dollar meant offshore equity returns often received a second tailwind once translated back into local currency. Many Australian investors benefited from owning US equities and US dollars alike.

That backdrop is shifting.

In 2025, emerging market equities recorded their strongest outperformance against developed markets in years, and emerging market bonds have shown similar strength. Central banks are no longer moving in lockstep. As the US dollar has weakened, the burden of US dollar-denominated debt on emerging economies has eased and commodity exporters have benefited. This is a dynamic that has historically accompanied a broader rotation away from US asset dominance.

For Australian investors, the most immediate consequence is the Australian dollar itself. After years of persistent weakness, it has begun to recover against the US dollar. If it continues to do so, the case for treating currency as an afterthought grows harder to make.

A more deliberate approach

Strong offshore equity returns no longer translate as cleanly into Australian dollar terms as they did in the previous cycle. That does not make hedging the automatic answer. Over the long run, currency risks tend to even out, and investors should be wary of making permanent portfolio changes in response to cyclical moves.

The more useful starting point is a view on the Australian dollar itself. Investors who expect it to rise have reason to hedge; those who expect it to fall may be better served remaining unhedged. Either way, currency deserves a deliberate decision rather than a default.

That decision turns on several considerations such as the investor’s time horizon, where the Australian dollar sits relative to its historical range and the diversification role that unhedged international exposure has traditionally played in a portfolio.

Some investors may choose to remain entirely unhedged. Others may prefer splitting hedged and unhedged exposures evenly. Others may decide the current environment warrants a greater allocation to hedged international assets.

From a broad asset allocation perspective, we think that the long-term difference between a hedged exposure and an unhedged exposure will be little. Currency markets are volatile and even professionals find it difficult to forecast consistently.

As of writing, the Australian dollar is trading closer to its long-run average against the US dollar (around 70 cents), while interest rate expectations, commodity prices and geopolitical developments are continuing to pull individual currencies in different directions.

For investors who wish to hedge, the VanEck MSCI International Quality (AUD Hedged) ETF (ASX: QHAL) and VanEck MSCI International Value (AUD Hedged) ETF (ASX: HVLU) allow investors to access international equities while reducing the impact of foreign exchange.

When the soundtrack changes, so does the story

The score in Interstellar does not ask the audience’s permission to matter. At some point, it just does. Currency exposure in international investing may have reached that moment.

The question is no longer whether currency movements will shape returns. It is whether investors are prepared to think more deliberately about the role those movements may play within their portfolios.

Key Risks

An investment in the ETFs carries risks associated with: ASX trading time differences, financial markets generally, individual company management, industry sectors, foreign currency, currency hedging, country or sector concentration, political, regulatory and tax risks, fund operations, liquidity and tracking an index. See the relevant PDS and TMD for more details.

QHAL and HVLU are likely to be appropriate for a consumer who is seeking capital growth, is intending to use the product as a major, core, minor or satellite allocation within a portfolio, has an investment timeframe of at least 5 years, and has a high risk/return profile.

Published: 28 May 2026

Any views expressed are opinions of the author at the time of writing and is not a recommendation to act.

VanEck Investments Limited (ACN 146 596 116 AFSL 416755) (VanEck) is the issuer and responsible entity of all VanEck exchange traded funds (Funds) trading on the ASX. This information is general in nature and not personal advice, it does not take into account any person’s financial objectives, situation or needs. You should consider whether or not an investment in any Fund is appropriate for you. Investments in a Fund involve risks associated with financial markets. These risks vary depending on a Fund’s investment objective. Refer to the applicable product disclosure statement (PDS) and target market determination (TMD) available at vaneck.com.au for more details. Investment returns and capital are not guaranteed.